The Automotive Slowdown

Technological disruption and weak economic conditions weigh on the car market; better resilience for the commercial vehicles segment.

Published by Alba Di Rosa. .

Asia Europe Automotive Slowdown Uncertainty Conjuncture United States of America Global demand AutomotiveLatest data confirm what has been known for months: the automotive industry is experiencing a phase of slowdown, not only in Europe but worldwide. As document in previous articles, the factors behind the slowdown can be summarized as follows:

- The structural transformations the car market is going through: from the gradual abandonment of diesel following the Dieselgate scandal and the introduction of more stringent regulations on emissions, to the slow shift towards electric cars;

- A weak global economic outlook which, together with trade war tensions, fuels uncertainty and discourages corporate investments, as well as household consumption.

The availability of complete data on production and sales in 2018 for more than 100 countries (see the Automotive database in the Analytics section of the platform) makes it possible to analyze the current phase of slowdown and evaluate the performance of the automotive industry in 2018 compared to the previous year.

Car industry: widespread slowdown

2018 data suggest that the car sector has been experiencing more difficulties compared to the commercial vehicles segment.

- Production

Globally, car production declined by almost 3% in 2018 (in terms of units).

Although the ranking of top producers has remained unchanged - featuring China, Japan, Germany, India, South Korea and the United States - major car manufacturers registered a decrease in the number of cars produced in 2018, compared to 2017. With the exception of India (+2.6 %) and Japan (almost zero growth), figures range from the disappointing -9.3% variation recorded for Germany to a smaller 2% contraction in South Korea; production decreased by 7.8% in the USA and by 5.1% in China.

On the contrary, Russia, Romania, Portugal and India showed the most relevant positive variations in the number of cars produced.

- Sales

Sales trends are similar to those described about production: car sales fell in 2018, as well, with a negative variation close to -3%.

The podium of the major markets has remained unchanged compared to 2017 (China, USA, Japan, Germany, India and Great Britain); nonetheless, car sales registered a collapse in all major markets - with the exception of India (+ 5.1%) and Japan (+ 0.11%).

The greatest contraction occurred in the USA (-12.8%), followed by Great Britain (-6.8%); smaller contractions in China (-4.1%) and Germany (-0.16%).

Major increases in terms of sales were recorded for Brazil (+ 13%), India (+ 5%), Russia (+ 11%), Spain (+ 7%), Thailand (+9.6%) and France (+ 3%).

- Foreign trade

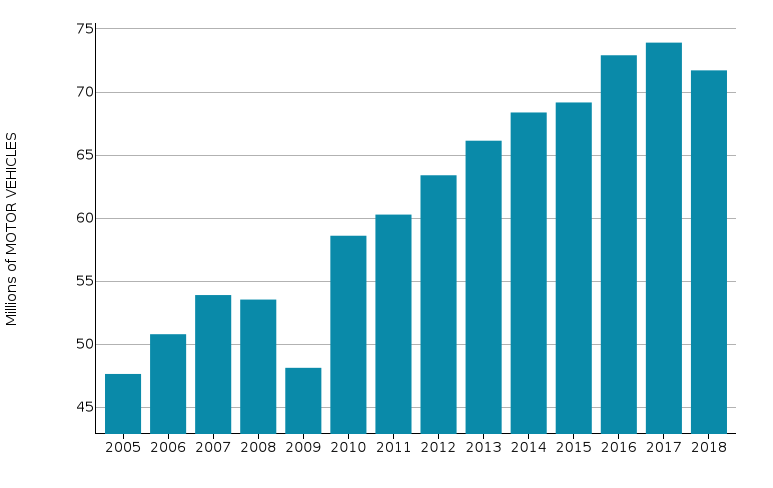

Foreign trade data further confirm the ongoing slowdown. Global demand for cars (in units) showed a slight slowdown in 2018, after reaching a peak in 2017.

Graph 1 – Global demand for cars, in units (1995-2018)

Source: ExportPlanning.

Good performance for commercial vehicles

Unlike the negative trend shown for the car sector, estimates available for the commercial vehicles segment show a dynamic growth in 2018, both in terms of production (+4.2%) and sales (+5.6%).

Major producers showed generalized growth in terms of number of vehicles: +4.4% for the US, +1.7% for China, +15.4% for Mexico and +2% for Japan.

In addition to being the major commercial vehicles producer, the United States also ranked as major market in 2018 and recorded a significant expansion of sales (+8% in terms of units); significant growth for China, Canada and India, as well. Sales also expanded in relatively smaller markets, such as Brazil (+16%) and Spain (+21%).

An overview

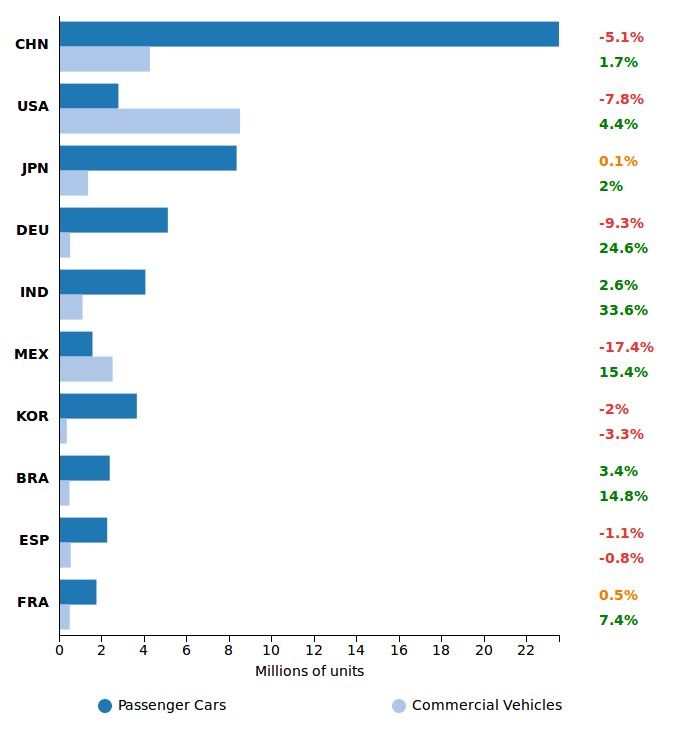

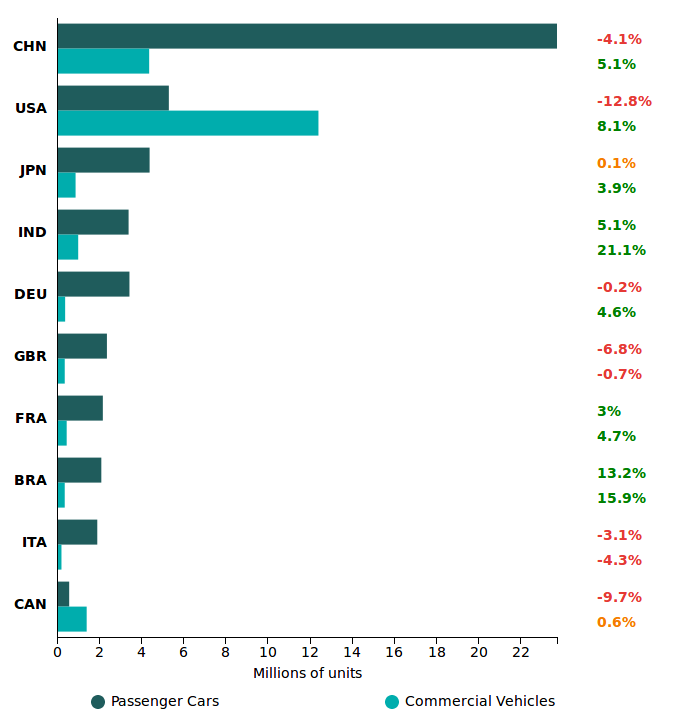

Graphs shown below summarize the dynamics described so far, as regards production (Graph 2) and sales (Graph 3), focusing on the top 10 global players. The percentage shown on the right indicates, for each country, the variation in the number of vehicles produced (Graph 2) or sold (Graph 3) in 2018 compared to 2017.

Graph 2 – Motor vehicles production (2018)

Source: StudiaBo elaborations on ExportPlanning data.

The overall production picture suggests that a positive growth trend for both cars and commercial vehicles is quite rare (see India and Brazil). Decreases in production or stagnation prevail, especially for the car sector. On the contrary, the commercial vehicles segment shows positive variations for all the top manufacturers, but South Korea and Spain.

Graph 3 – Motor vehicles sales (2018)

Source: StudiaBo elaborations on ExportPlanning data.

Quite similar scenario on the sales front. In the ranking of the 10 largest markets for motor vehicles, only two of them showed sustained growth in registrations in 2018, namely India and Brazil; smaller positive increase for France, while Italy and the UK showed a contraction in both sales of cars and commercial vehicles.

Conclusions

The analysis therefore confirms that, in the last year, the automotive industry found itself among the victims of the global economic context, characterized by uncertainty and commercial tensions that do not favor corporate investment. This has combined with the sector's own challenges, first of all sustainable mobility, and the shift in consumer needs: consumers are now starting to demand a service - mobility - instead of a product - cars.

For the automotive industry, critical challenges therefore extend over several fronts: on the one hand, the great challenge of innovation, about which companies can directly intervene; on the other hand, the unfavourable general economic context, against which companies do not have any leeway. It is therefore likely that a sustained recovery of the industry will be achieved only by overcoming both these sources of tensions.

You may be interested in:

U.S. tariffs and a weak dollar: Europe's challenges

Published by Marzia Moccia. .

United States of America Trade war Uncertainty Made in Italy Global economic trendsL’Unione Europea tra incertezza negoziale, pressioni protezionistiche e deprezzamento del dollaro [ Read all ]

US imports of goods after Liberation Day

Published by Silvia Brianese. .

United States of America Trade war Conjuncture Foreign market analysisLe importazioni statunitensi in frenata ad aprile-maggio 2025 dopo il boom del primo trimestre [ Read all ]

Food Machinery: Segments and Markets with Highest Export Potential

Published by Marcello Antonioni. .

Development stage of Imports Metal industry Industrial equipment International marketing Uncertainty Marketselection Foreign markets Export markets Foreign market analysisNew high for the world trade in the sector, thanks to numerous markets in structural Growth, spread across the main segments [ Read all ]