The textile-apparel supply-chain after the pandemic crisis

An analysis of world trade in 2020-2021 and outlook 2022

Published by Marcello Antonioni. .

Covid-19 Fashion Internationalisation Great Lockdown Industrial equipment Consumption pattern International marketing

Log in to use the pretty print function and embed function.

Aren't you signed up yet?

signup!

2020: the year of falling world demand, but also of 'fly-to-quality'

The pandemic crisis that erupted at the beginning of 2020 hit the textile-clothing industry hard - due to the Great Lockdown it necessarily entailed. The drastic drop in world demand for textile-clothing products is well known (-40% trend in the second quarter of the year, -17.1% at year-end at constant prices).

What is less well documented, however, is the strong qualitative shift that has occurred throughout the supply chain.

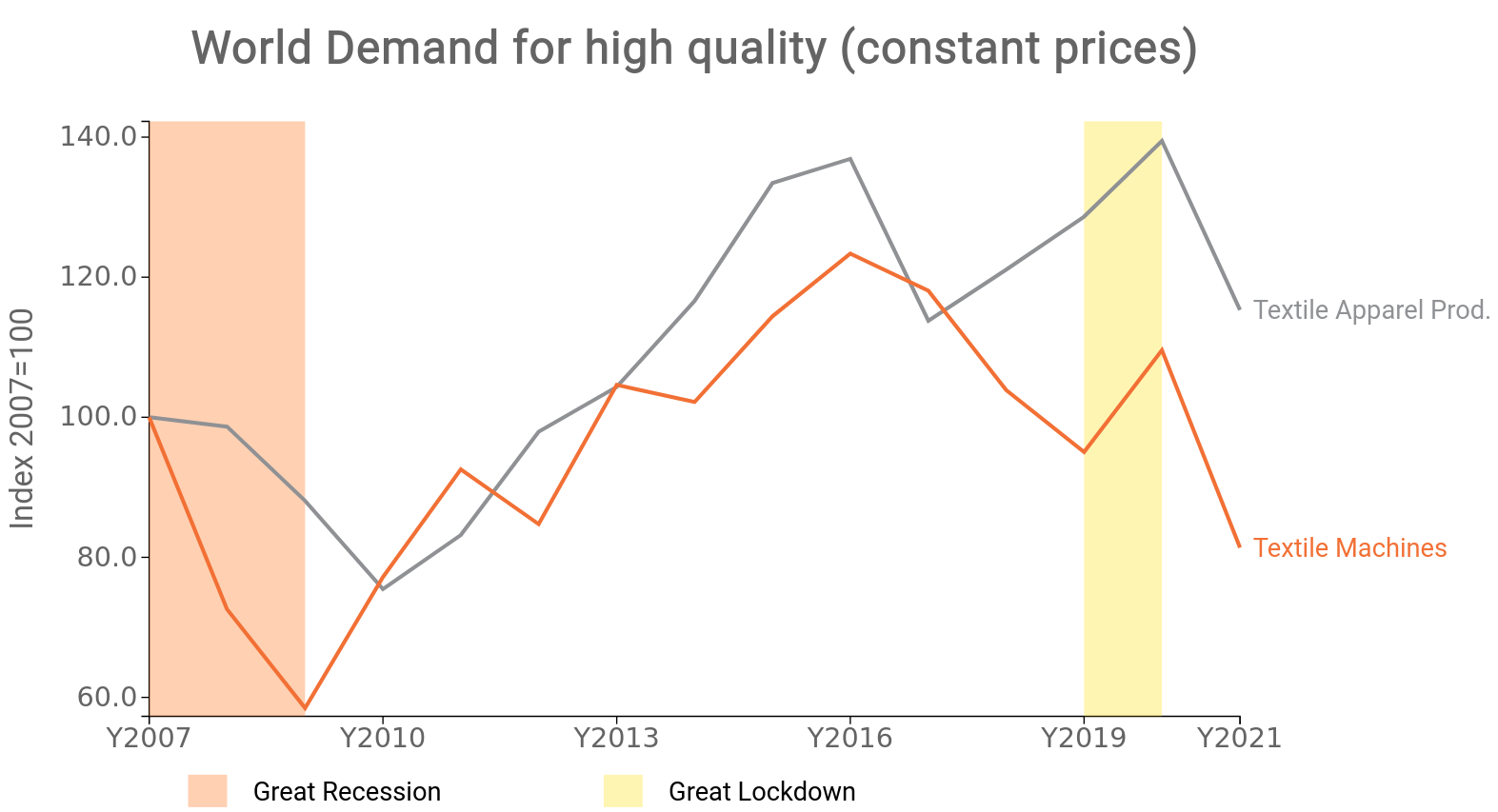

In 2020 there was a strong improvement in quality

of world trade across the textile-apparel supply chain

The fall in world demand for textile-apparel products that occurred in the second quarter of 2020 and the subsequent strong uncertainty as to when and how it will recover seem to have prompted operators in the supply chain - in order to escape the much-increased competitive pressures - to focus significantly on quality differentiation strategies. The result was that, on average for 2020, world demand for textile/clothing products by price/quality bands - measured by the ExportPlanning Information System - recorded, against a fall in flows in the medium-low price/quality bands, a significant growth (+8.4% in values at constant prices) of flows relative to the highest price/quality bands.

A similar phenomenon occurred upstream in the textile-apparel supply-chain, as a result of a demand for technology that seems to have favoured purchases of higher quality machines. In 2020, world demand for high- and medium-high price textile machinery grew by more than EUR 1.4 billion, while that for the other ranges fell by a total of EUR 3.5 billion1.

In other words, companies have indeed reduced their investments in machinery in 2020, but by reducing the medium-low priced ones (mainly intended to increase production capacity) and not the higher priced ones (mainly intended to improve competitiveness).

To summarise, therefore, the outbreak of the pandemic made companies in the textile-clothing chain fear prolonged falls in demand, not a reduction in the degree of competitiveness in the various markets, but on the contrary an accentuation of it. The consequence was to block projects aimed at increasing production capacity while safeguarding those aimed at improving the company's competitiveness.

This phenomenon is even more relevant especially in relation to what happened in correspondence with the previous great crisis (Great Recession) in 2008-2009, where sales in the high price brackets were hit hardest along the supply chain.

Source: ExportPlanning-Annual Datamart

The year 2021: the year of the strong (and partly unexpected) 'rebound', but concentrated on the medium and low segments

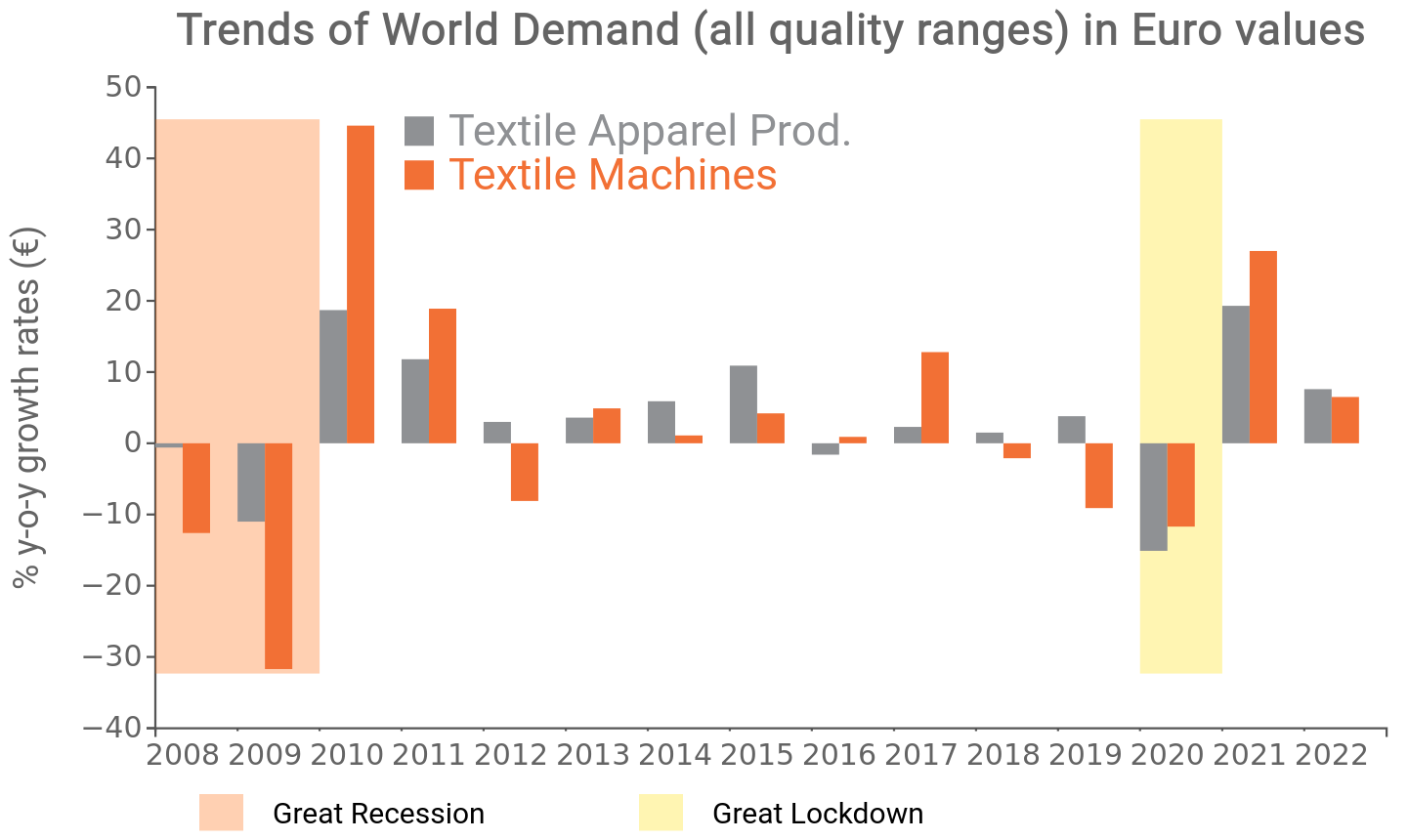

The year 2021, on the other hand, was characterised by a sudden (and partly unexpected) recovery in world demand for textile-clothing industry products: after a first quarter that was still 'disrupted' and apart from the predictable technical rebound in the second quarter of the year (+56.5% in constant price values), the remaining part of the year saw tendential growth rates of world sector demand of around +12% in constant price values.

The end of the year - recently certified by the annual ExportPlanning data - saw an increase over 2020 of +21.4 per cent in constant price values, on overall levels almost 10 per cent higher than pre-pandemic levels.

Even upstream of the supply-chain, in the textile machinery sector, the recovery experienced in the average of 2021 was significant (+28.4 per cent compared to 2020 in constant price values), making it possible to almost completely recover pre-pandemic levels (just 4 percentage points away in constant price measurements).

In 2021 the significant recovery of world trade in the textile-apparel industry was concentrated on the lower price segments

In contrast to what happened in 2020, in the average of 2021, world trade data disaggregated by price/quality bands show a strong re-acceleration of flows in the lower-middle bands both upstream and downstream of the textile-clothing chain. In the downstream products, last year world trade grew in the lower bands by more than 24 percentage points compared to 2020 in constant price values, while flows in the higher quality bands recorded a significant retreat.

Similarly, in the textile machinery sector, world flows in the medium-low ranges recovered very strongly in 2021 (+68 per cent in constant prices, after -41 per cent in the previous year), while those in the higher price ranges contracted (-25.7 per cent).

In this second case, therefore, companies in the textile-clothing chain aimed to quickly regain efficiency on the production side and to invest again in capacity expansions.

The year 2022: the inflation bogeyman on consumption and the outlook for world trade

The 2022 scenario appears to be full of unknowns for the textile-clothing supply chain. As documented in the recent article "War and Pandemic slow but don't stop World Trade", the economic damage caused by the Russian-Ukrainian conflict will contribute to a significant slowdown in global growth in 2022 and an increase in inflation, which will tend to penalise textile-clothing consumption.

It should be stressed, however, that cyclical information indicates that the ongoing deceleration is certainly significant, but far from translating into a break in the recovery cycle of world trade that started in the second half of 2020.

Moreover, the depreciation of the euro against the dollar, expected in the course of 2022 in the order of almost 5 percentage points, will support global purchasing power in euros. In euro-denominated values, world demand for textile and apparel industry products is expected to grow by +7.6 per cent (which, however, falls to +2.9 per cent in dollar-denominated values).

With regard to world demand for textile machinery, the forecast for 2022 is +6.5 per cent in euro-denominated values, falling to +1.8 per cent in dollar-denominated values.

Source: ExportPlanning-Forecast Datamart

In essence, after the strong rebound in world trade in 2021, the effects of the war in Ukraine and difficulties in global logistics will lead to a marked slowdown in global trade in the textile-apparel supply chain.

Against this backdrop, it will be interesting to see which competitive strategies the companies in the supply chain will tend to favour in the dichotomy between qualitative differentiation and volume strategies in 2020-2021.

1) With regard to the textile machinery sector, only China increased its exports in 2020, but this growth only affected the high price brackets, while the flows in the medium-low brackets fell. Similarly, in 2020, the other main competitors, while they saw their exports in the low to medium price brackets plummet, saw exports in the higher quality brackets hold up.

Also on the market front, in 2020, the main markets in the sector (Turkey, Bangladesh, China, Vietnam, India) recorded growth in high-end imports, against significant declines in the other ranges.