Exchange Rates: August Wrap-up

Euro and dollar reverse their balance of power; among EM currencies, eyes on Turkey and Argentina

Published by Alba Di Rosa. .

Exchange rate Dollar Euro Swiss franc Turkish lira Uncertainty Japanese yen Argentine peso Economic policy Central banks Exchange rates

Log in to use the pretty print function and embed function.

Aren't you signed up yet?

signup!

The ones we are leaving behind, will certainly be months to remember. As far as our weekly exchange rates analysis is concerned, some topics to keep in mind are as follows: the changed balance of power for the EUR/USD exchange rate and the cyclical risks affecting emerging markets' currencies, especially in the face of external shocks.

EUR/USD

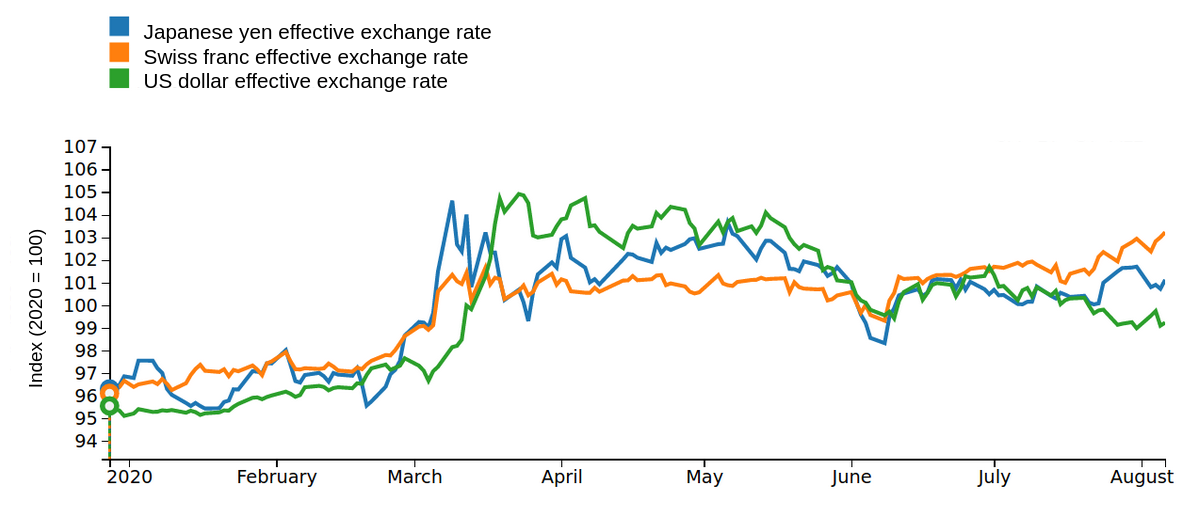

As we have reported over the past few months, in the early stages of the pandemic the dollar played a key role in meeting the sudden increased demand for liquidity, as an immediate market reaction to the health emergency. The rise in demand for dollars as a safe-haven currency led to a 7.7% surge in March in terms of effective exchange rate.

The gradual normalisation of the emergency, the strongly expansionary measures taken by the central banks of the major countries and the support interventions at the level of fiscal policy have progressively allayed makets' fears, and the consequent race towards a safe harbour. Approximately from the second half of May the dollar has started its descent, back to more contained levels.

Safe-haven currencies: Effective exchange rates

As can be seen from the chart above, the dollar appreciated more than the other safe-haven currencies at the peak of the crisis, and then reversed this trend more markedly: at present, the greenback is at lower levels than the Japanese yen and Swiss franc, considering their effective exchange rates (index: 2020 = 100).

As the determinants underlying the dollar's significant strengthening have faded, analysts expect this trend of relative weakness to continue in the coming months, also in light of the uncertainty posed by the upcoming presidential elections in November.

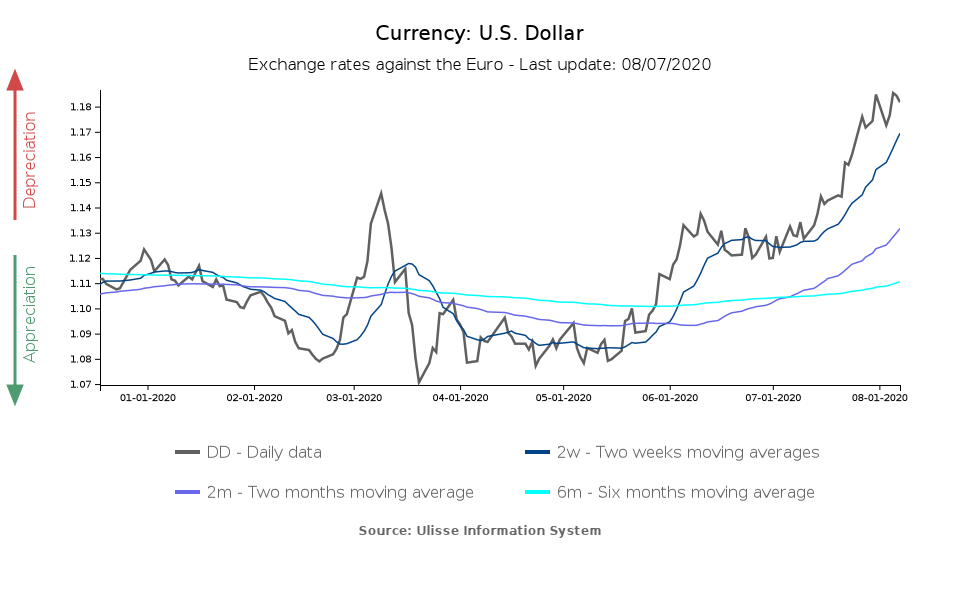

On the other side of the ocean, the summer of the single currency seems to be marked by a significant strengthening, thanks in particular to the agreement reached on the Recovery Fund: the EU's cohesive response to the health emergency has in fact reassured financial markets on the possibility of an economic recovery of the bloc, acting as a boost for the euro.

In the last week the euro-dollar exchange rate remained stable, falling briefly to 1.17 USD per EUR, before returning to 1.18 (the highest levels in the last two years).

EM currencies

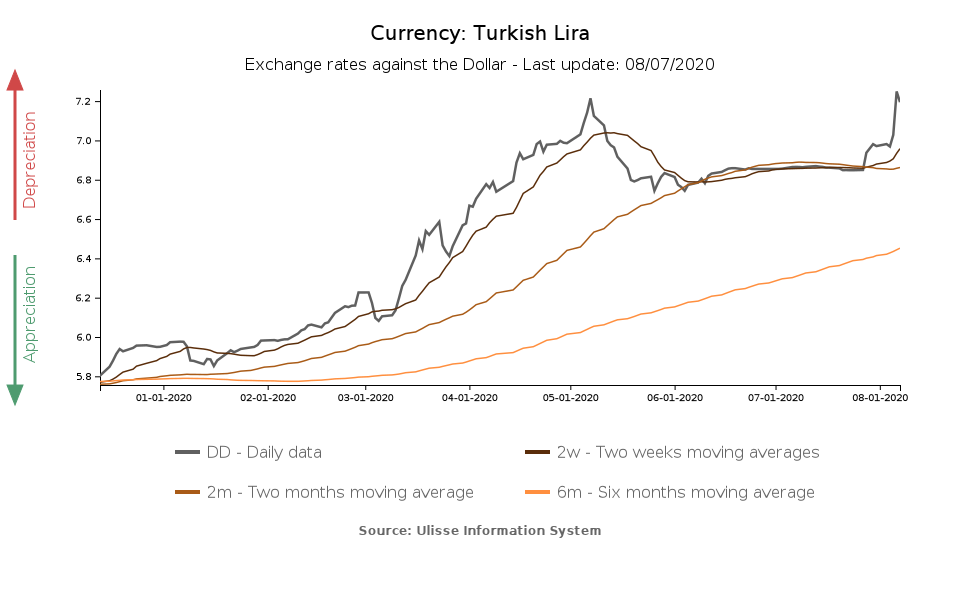

After the blow of the Covid crisis, emerging countries' currencies showed a general recovery: the MSCI EM Currency index shows a recovery roughly from mid-May to the end of July, while there has been relative stability in recent days. However, the situation differs from country to country. At present, among the most critical cases we can find two currencies with a troubled history back on the scene: Turkish lira and Argentine peso.

Compared to the scenario described last week for the lira, the situation has currently worsened. In the last few days, its exchange rate against the dollar showed a vertical drop, from 6.97 TRY per USD last week to 7.25 yesterday, to than fall back to 7.19 today. We could be on the eve of a new stormy August for the lira, as happened two years ago.

In addition to the risk factors described last week, a further sign of a malfunctioning of the Turkish currency market emerged in the last few days: on Tuesday, overnight rates on Turkish lira currency swaps in the London market broke the 1000% threshold, in what appears to be an expensive attempt by Turkish monetary authorities to discourage investors from betting against the lira. This signals an extremely precarious situation in a dysfunctional currency market.

As far as Argentina is concerned, the currency signals a serious economic emergency: since the beginning of the year, the peso has lost more than 20 percentage points against the dollar.

At the end of May, the country officially went into default, and began negotiating an agreement with its creditors for debt restructuring. An agreement between the Argentine government and its creditors has allegedly been reached on August 4: bonds held by creditors would be replaced by new bonds, for which creditors would be repaid about 55 cents for each dollar invested.