US Exports Trends: Q1-2021 Figures

Although US exports of several industries are close to pre-pandemic levels, the upsurge of the virus is still penalizing Fashion and Automotive industries

Pubblicato da Gloria Zambelli. .

United States of America Trade balance Importexport Fashion Automotive Global Economic TrendsThe recent release by US Census Bureau of the US foreign trade statistics in the first quarter 2021 (see Exportplanning pre-estimates) allow us to estimate the performance of US exports in the several industrial sectors, taking stock of American foreign sales recovery path. According to our estimates, the United States opened the first quarter of the year with exports and imports flowing respectively at 380 and 606 US billion.

In the graph below is reported the evolution of US balance of trade from 2019-Q1 to 2021-Q1, in order to get a picture of the recovery dynamics over the quarters, comparing latest results to pre-pandemic values.

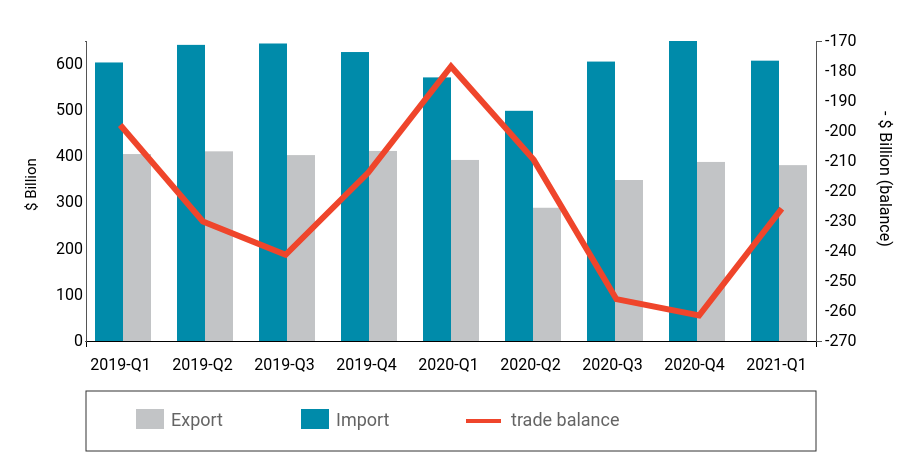

US Trade Balance (Q1-2019 to Q1-2021)

After the deterioration of deficit recorded during the third and fourth quarter 2020, the US trade balance increased in Q1-2021 to $ -225 billion, opening positively this 2021.

However, this rebound is due not to an increase in US exports, whose flows seem to have stabilized below 390 USD billion, but to a cut in US imports which fell to $ -42.5 billion compared to the values of the previous quarter.

Indeed, despite the spread of vaccines, the recrudescence of the virus has led several countries to apply new containment measures during the firsts months of 2021, waiting to achieve herd immunity.

Comparing the pre-estimates results of Q1-2021 with import and export flows of Q1-2019 clearly emerges that US imports have reached values close to pre-pandemic values (-0,64%) and,with weaker performance, so have US exports (-6%).

However, US imports and exports still reflect the changes due both to the ongoing impact of the COVID-19 pandemic and the path to economic recovery from the harsh declines of 2020. Over the past few months in several articles1, we documented how the performance heterogeneity of industries reflects the reshaping that the outbreak of health crisis has imposed on the international consumer preferences. In this context, it might be useful to analyze the results from a sectoral perspective, to check if this dynamic is also present in the first quarter of 2021.

In the following graph the different industries are placed according to the year-over-year rate of change in exports in 2020 (on X-axis) and rate of change recorded in Q1-2021 compared to the first quarter 2019 (on Y-axis). While, the size of each ball is proportional to 2019 exports value. In this way, it is possible to highlight the industries that show the greatest delays in the recovery path.

United States exports by industries

Overall, in spite of the presence of some outlier industrial sectors which are positioned at the extremes of the map, the graph shows a certain homogeneity in the recovery of US industries exports. Almost all industries showed a significant resilience compared to the 2020 results, placing them nearby or above the yellow bisector, which separated the declining from the accelerating industries. Moreover, most sectors are positioned in the middle of the chart, with the change in export flows in Q1-2021 compared to the same period of 2019 contained between -12% and +12%. In contrast, at the extremes of the map are located the US industries whose export flows in the first quarter 2021 are better (top-right area) or worse (bottom-left area) than the same period of 2019.

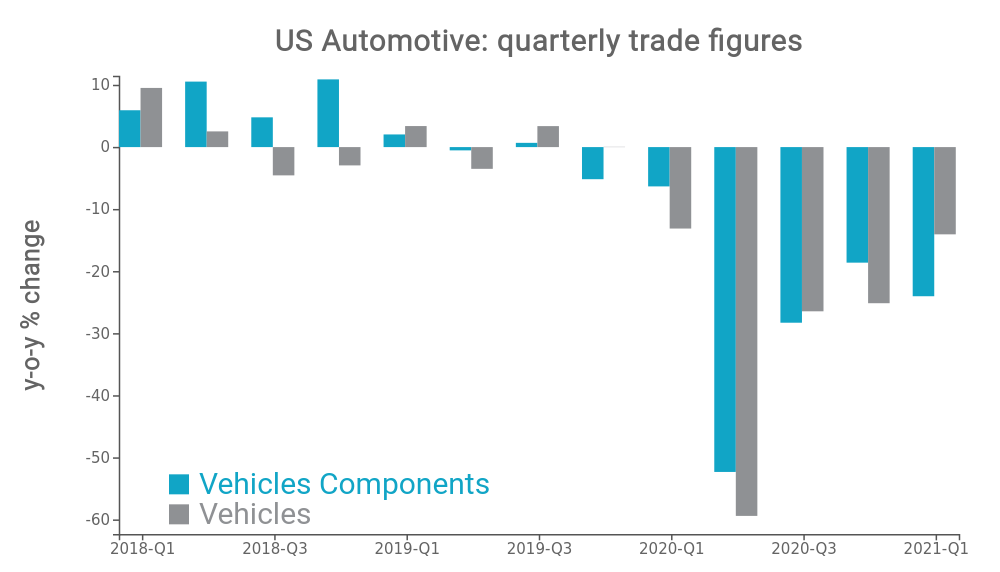

Particularly positive is the performance of US Machinery (F4) , which opened 2021 with an almost 40% growth rate compared to the value of 2019-Q1, proving to be the best dynamics sector during the opening quarter. In contrast, in line with what was reported in a previous article, the most significant downturns are visible in textile-fashion and automotive sectors, which continue to be the most affected by the current economic situation.

Automotive and Fashion industries

Vehicles, Vehicles components and Fashion goods exports diminished respectively by -25%, -29% and -28% compared to 2019-Q1; the downturn in Fabrics was more contained, standing at around -13% (see chart above). In Q1-2021, the automotive sector registered a contraction in exports for the fifth consecutive quarter, recording a drop between -14% and -25% YoY (see chart below). The same applies to the US fashion industry, whose export decline began in the first quarter of 2019, recording in the first quarter 2021 a fall of -10% and -3.4% YoY (see chart below).

Conclusions

In summary, albeit empirical evidence shows that in this first quarter of 2021 several sectors have consolidated their recovery path by achieving results close to pre-pandemic values , others, namely automotive and fashion sector, are lagging far behind. The next few months will be crucial to see whether the collapse of these sectors will be permanent or we will see a new recovery phase.

1. For an in-depth discussion of this topic, see the following articles: The Recovery Path of US Exports: Sector Analysis and Performance in the Year of Covid-19, International Trade by Sectors: 2020 Figures.

Potrebbero interessarti anche:

US-China Phase One Deal: Tracking Progress H1-2021

Pubblicato da Gloria Zambelli. .

United States of America Slowdown Free trade agreements Asia Global Economic TrendsU.S. exports to China are not flourishing despite the commitment with the "Phase One" agreement [ leggi tutto ]

US Vehicles Components: an Update

Pubblicato da Gloria Zambelli. .

United States of America Importexport Electronics Automotive Global Economic TrendsEconomic recovery proceeds, although still marked by uncertainty [ leggi tutto ]

US Export Trends: Q2-2021 Figures

Pubblicato da Lorenzo Fontanelli. .

United States of America Macroeconomic analysis Importexport Global demand Global Economic TrendsExports during 2021-Q2 hit record high as they outpace pre-pandemic levels. Growing demand for American-made food and electronic parts [ leggi tutto ]