Amid tariffs and uncertainty, the downsizing of US imports continues

Published by Alba Di Rosa. .

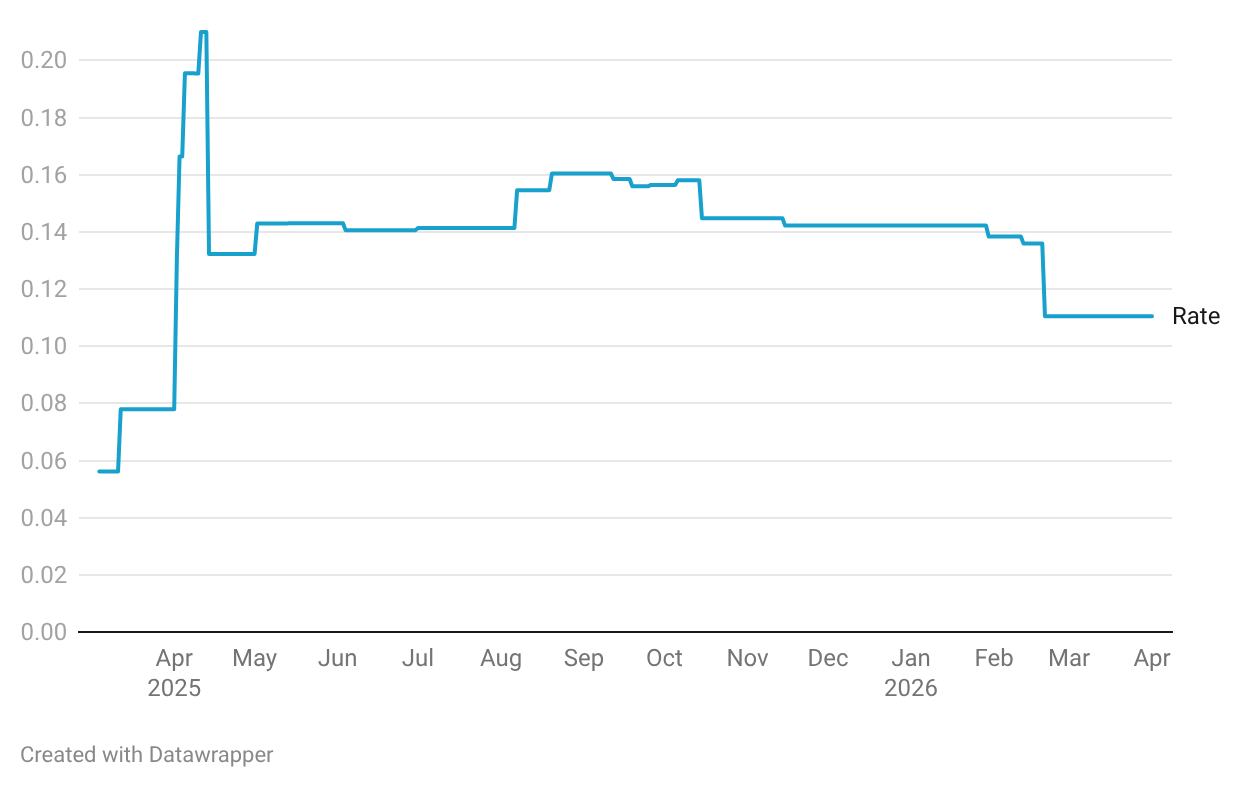

Dollar United States of America Trade balance Export Trade war Import Foreign market analysisUS trade policy decisions took center stage in global attention and debate in 2025, amid a return to levels of protectionism that had long since faded from historical memory: according to the Tax Foundation, in 2025 the average effective US tariff rate stood at 7.7% – the highest levels since 1947.

Nevertheless, the effectiveness of US protectionism appears to be limited, for the time being: according to a study by the Federal Reserve Bank of New York, nearly 90% of the economic burden of tariffs collected in 2025 actually fell on US businesses and consumers – rather than on foreign exporters – thus highlighting the substantial ineffectiveness of the defensive approach of Trump’s trade policy. The figures regarding the US trade balance in goods in 2025 also confirm substantial stability: last year, it remained in deficit by over $1.3 trillion, in line with 2024 levels.

After a 2025 marked by negotiations aimed at securing more favorable trade agreements for American exporters, 2026 began with new twists and turns, which continued to fuel uncertainty in the realm of international trade. As documented in this article, on February 20, the US Supreme Court ruled that the so-called “reciprocal” tariffs introduced by the Trump administration in the context of “Liberation Day” – adopted under the International Emergency Economic Powers Act – were invalid.

Trump’s response was immediate: relying on a different legal basis – Section 122 of the Trade Act – the administration introduced a new 10% general tariff on the same day, in addition to MFN (Most Favored Nation) conditions, effective February 24. The new general tariffs are, however, temporary in nature, with a maximum duration of 150 days, extendable only with the prior consent of Congress; by summer, it will therefore be necessary to review the current tariff framework, interrupting the current scenario of apparent calm – at least on the trade front.

Overall import-weighted effective tariff rate

in the United States, by calendar day

Source: elaborations on The Budget Lab at Yale data

Foreign Trade Figures

In an international landscape that remains multifaceted and complex, what signals are emerging from US trade in goods? The US Census Bureau recently released the latest data, updated as of February 2026, and now available on the ExportPlanning platform.

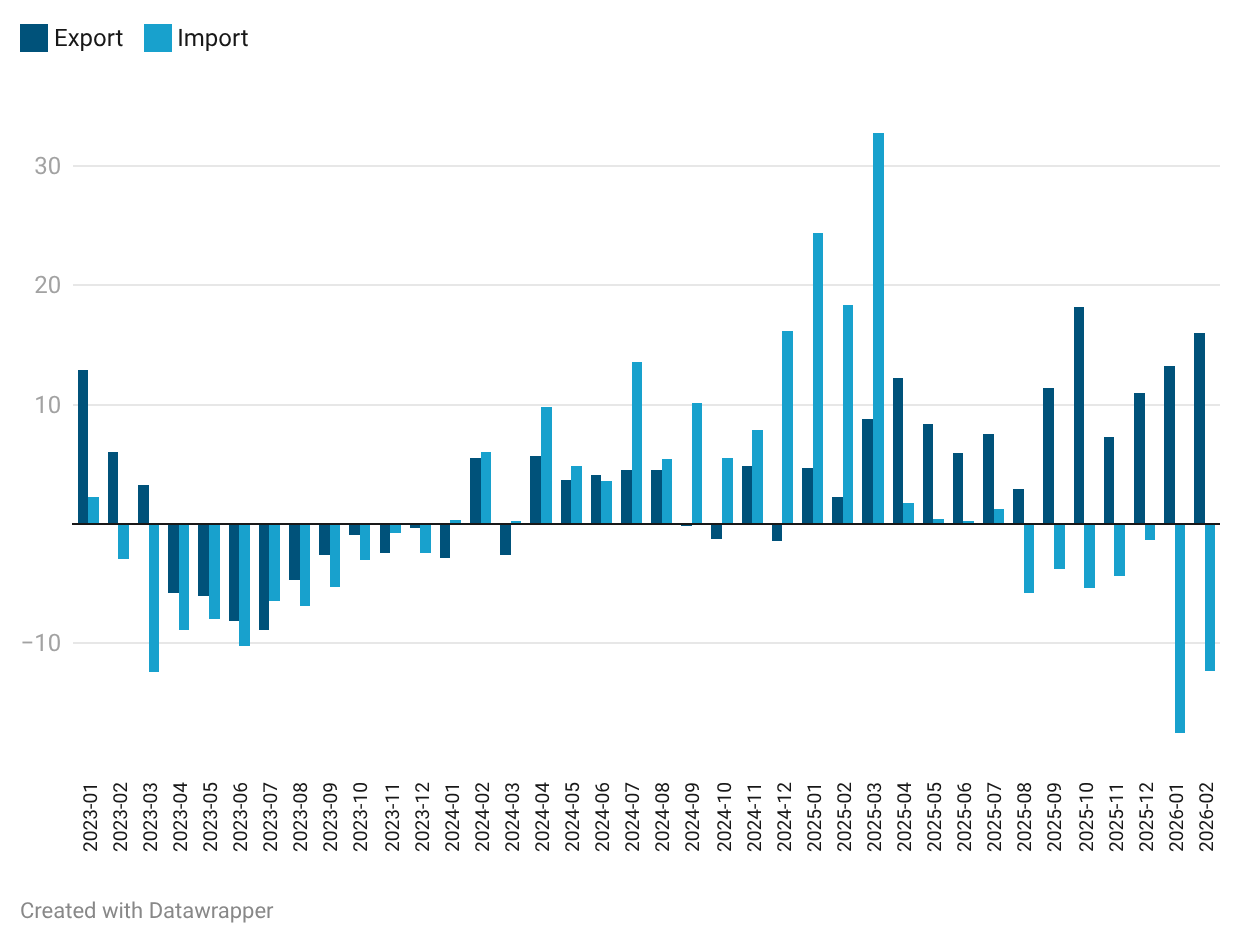

US Trade (monthly data)

% change compared to the same month of the previous year, in USD

Source: ExportPlanning elaborations on US Census Bureau data

As you can see from the chart, the growth rates of US imports peaked in the early months of 2025, driven by the front-loading effect, before slowing down in the following months. Between April and July 2025, growth rates showed a sharp deceleration, offsetting the significant inventory effect of the previous months, before turning negative starting in August. On average for 2025, US exports grew by +8.4% (measured in current dollar terms), compared to a more modest increase (+4.4%) for imports.

The latest data released by the US Census Bureau, covering the first two months of 2026, show that the decline in US imports has accelerated significantly compared to previous months: specifically, US imports fell by 17.6% year-over-year in January and by 12.4% in February. In contrast, exports have progressively accelerated their growth rate since last December, reaching a year-over-year increase of 16% in current dollars in February.

It should be noted that the year-over-year growth rates for US imports in the first two months of 2026 are derived from a comparison with the exceptionally high levels recorded in the same period of 2025 – making a decline virtually inevitable. Nevertheless, the month-over-month change (i.e., compared to the previous period) in imports for January-February 2026 also remains negative: specifically, -7.2% in January and -3.5% in February; exports, on the other hand, remain positive: +3.6% month-over-month in January and +4.7% in February.

Our Preliminary Estimates for Q1-2026

Based on historical data released by the US Census Bureau, we have used econometric models to produce preliminary estimates regarding the performance of US trade at the end of the first quarter of 2026. On average for the first three months of the current year, we estimate a 9.6% growth for US exports in current dollars; this increase is slightly weaker than the +12.2% recorded in the previous quarter. The trend in imports, on the other hand, appears to have bottomed out, showing a decline of over 11% compared to the same period in 2025.

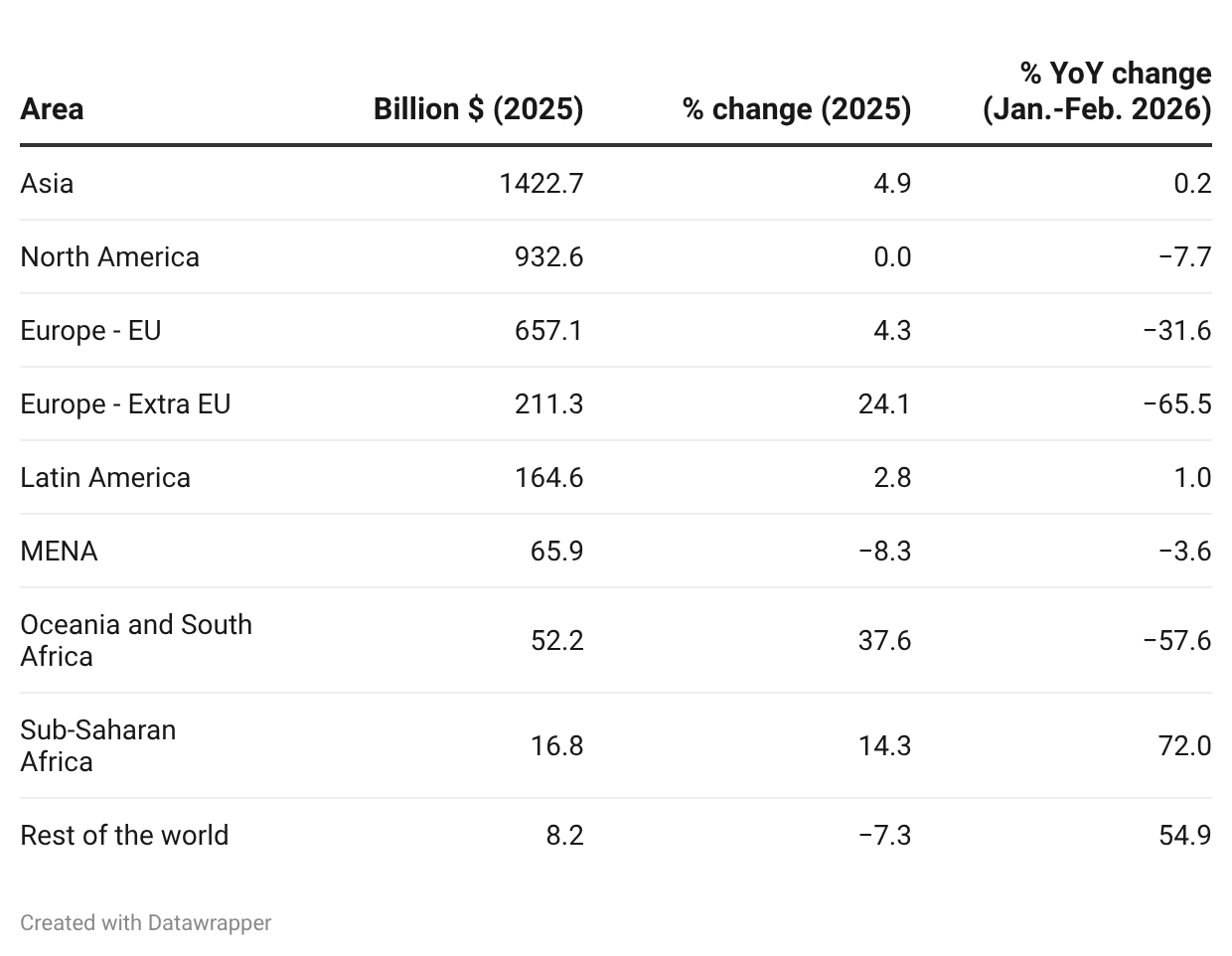

US Imports: Performance by Region and Product Category

Let’s now take a closer look at the performance of US imports in the first two months of 2026, broken down by region and product category.

US Imports: 2025 and the First Two Months of 2026

Source: ExportPlanning elaborations on US Census Bureau data

As shown in the table, US imports, broken down by area, continued to grow in the first two months of 2026 – in line with the performance observed in 2025 – for shipments originating from Asia, Latin America, and Sub-Saharan Africa. However, we are talking about a modest increase for Asia (+0.2%) and Latin America (+1%) in the first two months of 2026, following the stronger growth observed in 2025; imports from Sub-Saharan Africa, on the other hand, are accelerating, although they remain at comparatively very modest levels.

In contrast, US imports from the Middle East and North Africa (MENA) region continued to decline in the first two months of 2026; the contraction was at a slower pace than that observed in 2025. In contrast to last year’s growth, imports from the European region have seen a significant decline, both from EU (-31.6% year-over-year) and non-EU countries (-65.5%). This result is linked to the extraordinary flows that, conversely, were recorded last year, in terms of:

- exceptional imports of precious metal products (primarily gold for investment and industrial purposes) from Australia and, above all, Switzerland;

- a sharp increase in imports of pharmaceuticals from Switzerland, Germany, and Ireland;

- exceptional inflows of basic pharmaceutical products from Ireland.

In terms of product categories, the sharp decline in US imports during the first two months of 2026 appears to be fairly widespread. Among the few sectors bucking the trend, ICT and service equipment, as well as Electronic components stand out; there was also a modest increase in imports of Electrical engineering products. The US market thus confirms a trend that is now widespread globally, in which Artificial Intelligence and electronics are driving trade growth, while other sectors are undergoing a phase of reorganization, primarily linked to tensions and challenges generated by the trade war.

ExportPlanning provides on-demand supplies of monthly trade data,

tailored to the products and markets of interest.

You may be interested in:

January 2026: the latest data on global trade in goods

Published by Marzia Moccia. .

Slowdown Exchange rate Conjuncture Dollar Euro Foreign markets Uncertainty Global economic trendsThe availability in the ExportPlanning Information System of global trade data for January makes it possible to update the short-term outlook on the most recent dynamics of world trade in goods, wit}... [ Read all ]

Healthcare Industry: Robust Growth in international trade confirmed in 2025

Published by Marcello Antonioni. .

Health products Conjuncture Export Global economic trendsWorld exports of the healthcare industry have been growing strongly, across almost all sectors, but with differences between competing countries [ Read all ]

Electrical Engineering: one of the fastest-growing industrie in international trade 2025

Published by Marcello Antonioni. .

Electronics Conjuncture Export Global economic trendsWorld exports of Electrical Engineering are growing robustly, across almost all sectors, but with differences between competitor countries [ Read all ]