The Ascent of the Yuan: a Change of Strategy?

Published by Alba Di Rosa. .

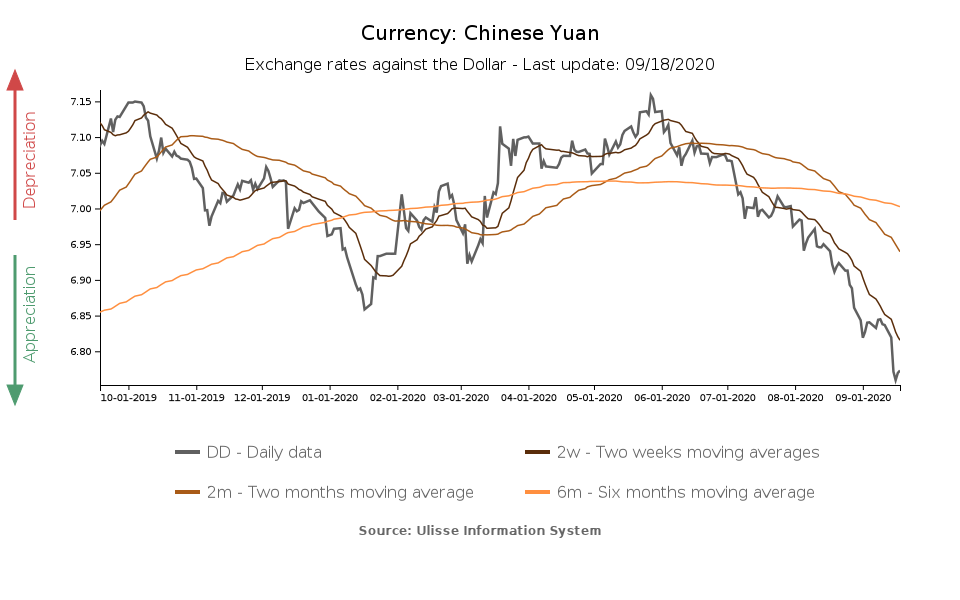

Covid-19 Exchange rate Asia Chinese yuan Central banks Exchange ratesA trend that emerged in early summer and gradually consolidated over the months is the strengthening of the Chinese currency, the yuan, as can be seen from the chart below. The exchange rate currently stands at 6.77 per dollar, for an overall strengthening in the last 3 and a half months of 5.4% against the greenback.

Before focusing on the possible determinants of this strengthening, it is useful to clarify some features of the Chinese exchange rate regime. In its latest Annual Report on Exchange Arrangements and Exchange Restrictions, the International Monetary Fund includes the Chinese exchange regime in the group of "Other managed arrangements". The exchange rate is defined as controlled in the short term, but would leave room for the influence of market forces in the long term (Sonali Das, 2019).

Some key features of the current exchange rate regime adopted in China:

- A central parity rate, calculated and announced on a daily basis by the central bank for the exchange rate of the yuan against a basket of currencies (CFETS RMB Index), including the US dollar

- A daily fluctuation band of +/- 2% within which trades can take place

- Potential interventions on FX markets by the central institution

Given these rules, the yuan exchange rate could theoretically depreciate or appreciate as much as 10% in a single week, if tolerated by the central bank.

Yuan: the latest developments

Having clarified the non-negligible weight of the People's Bank of China (PBOC) in determining the exchange rate of the yuan, let us go into more detail about the reasons behind the dynamics of the currency in recent months. This strengthening has been noted since it stands in contrast to the recent past: since the 2015 currency reform, the yuan has in fact moved from just above the threshold of 6 yuan per dollar to then exceed the threshold of 7 in 2019.

Below are some of the main factors currently at stake, which could help explain the currency dynamics.

Support signals come from the economic data front. Compared to the major world economies, the Chinese economy seems to give the most solid signs of recovery from the Covid crisis. The last projections released by the OECD signal China as the only country, among those examined, for which positive GDP growth is expected for 2020.

Data from the National Bureau of Statistics of China show increases for August in terms of industrial production (+5.6% YoY), retail sales (+0.5% YoY) and freight traffic (+4.8% YoY); all three indicators showed an acceleration compared to the previous month. On the contrary, passenger traffic is still in negative territory, with a 37.8% drop in August compared to the same period in 2019.

If this suggests that the Chinese industry has restarted, it would not seem to suggest an equally strong recovery for services linked to people's movement and free time. In fact, income and expenditure data show that per capita disposable income in H1-2020 decreased by 1.3% compared to the same period in 2019, while per capita expenditure dropped by 9.3%.

On the other hand, positive signals are coming from foreign trade: Chinese exports in July, the last available month, marked a 7.2% growth YoY, definitely up from +0.5% in June.

Among the factors supporting the yuan, the phase of deep weakness of the greenback needs to be carefully taken into account, as well. In bilateral exchange rates, the weakness of one of the two opponents will inevitably tip the balance towards the other currency.

Last but not least, these dynamics should be read from the perspective of a managed exchange rate. The strengthening of the yuan could therefore represent a phenomenon tolerated and potentially desired by the central bank.

In a framework of external trade tensions and a large internal market with growth potential, according to analysts it could be in the interest of the PBOC to move towards a new monetary policy strategy: from the objective of a competitive currency, that supports exports, to the strengthening of the internal market.

This is in line with the "Dual circulation plan", an idea announced by President Xi Jinping in May. Further details need to be disclosed yet. This would allegedly represent a new strategy for China's development in the coming years, mainly focused on "internal circulation" rather than external circulation (i.e. the internal process of production and consumption), aiming at reducing the country's external dependence.

Another reason for the PBOC's alleged tolerance to the current trend of the yuan could be the wide margins of strengthening: according to the Economist's Big Mac Index, the Chinese currency would be undervalued by 7% against the dollar, adjusted for the different GDP per capita.

You may be interested in:

IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsPer il 2026 il Fondo ha rivisto lievemente al ribasso le stime di crescita del PIL mondiale, ora previsto al +3% [ Read all ]

China keeps leading the way in the production of technical sportswear

Published by Mauro Badanelli. .

Covid-19 Internationalisation Industries Foreign market analysisLa capacità di intercettare opportunità internazionali nel B2B richiede oggi la comprensione dell'evoluzione delle geografie produttive globali [ Read all ]

January 2026: the latest data on global trade in goods

Published by Marzia Moccia. .

Slowdown Exchange rate Conjuncture Dollar Euro Foreign markets Uncertainty Global economic trendsThe availability in the ExportPlanning Information System of global trade data for January makes it possible to update the short-term outlook on the most recent dynamics of world trade in goods, wit}... [ Read all ]