World Trade in Manufactures: Better than Expected?

The profile by industry of international trade: 2022 figures

Published by Marzia Moccia. .

Slowdown Conjuncture Global demand Industries Uncertainty Global economic trendsAn international climate profoundly marked by the uncertainty of the Russian-Ukrainian conflict, increases in commodity prices, especially energy prices, and the resulting inflationary pressures, with a downward outlook for the world economic outlook, had led major international forecasters to estimate world trade volume growth in the range of 3-3.5 percent in 2022. However, the update of the World Conjuncture ExportPlanning database with the 2022 pre-estimate returns a slightly bullish picture compared to that forecast, showing a relative resilience of goods trade to the economic picture just described.

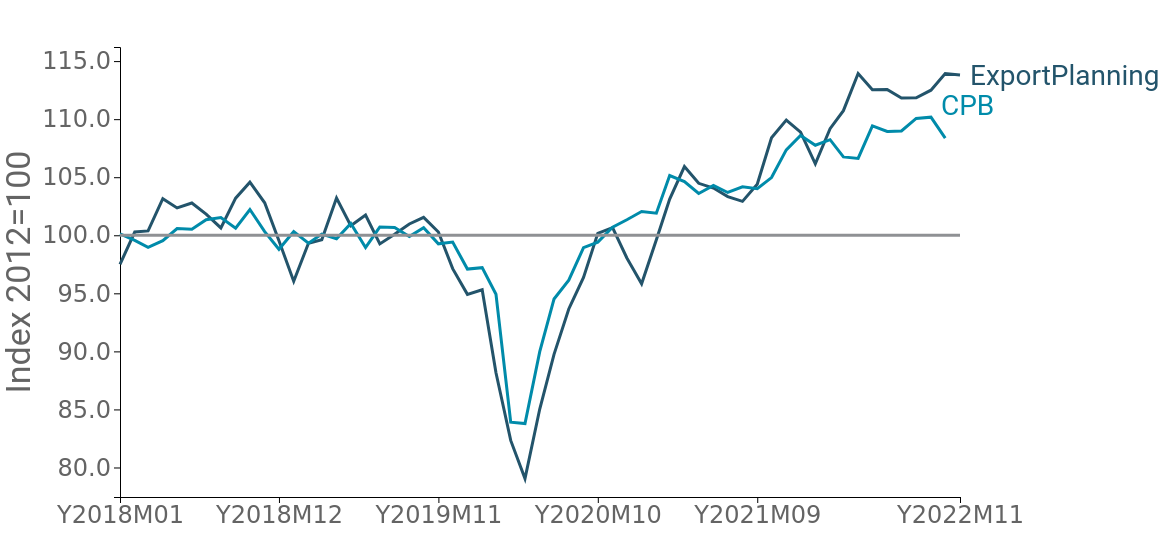

The graph below shows the monthly series of world trade in manufactured goods in quantity, comparing data collected and systematized by ExportPlanning with that of the Central Planning Bureau, an institute that in turn collects and processes information on international trade in goods.

Fig.1 - World trade in quantity

(CPB data vs. ExportPlanning data, three-term moving average)

Source: ExportPlanning - World Trade Datamart

It is evident from both series how world trade, after showing a vigorous and significant recovery during 2021, has gradually given way to a more moderate pace of trade expansion since the second part of 2022. Compared with a growth of 8.6 percent in quantity in the first half of 2022, the second half of the year in fact showed a more tentative increase of close to 6 percent. Overall, then, the ExportPlanning pre-stimate testifies to a 7 percent increase in world trade in manufactured goods in quantity over last year. A result that, while testifying to a slowdown in the expansionary phase of international trade, appears noteworthy and more positive than initially assumed.

The industry profile of international trade

In order to map the changes that are affecting the main industries that make up the world trade in manufactured goods, the graph below places on the x-axis the 2021 change over 2019 and on the y-axis the 2022 change over 2021.

Through this representation, it is possible, on the one hand, to highlight the industries in greater resilience/slowdown, relating them to the overall picture of recovery to pre-crisis levels.

Fig.2 – International trade at constant prices by industry

By hovering the mouse over the circle that identifies an industry, a table can be displayed that summarizes data on the average annual change in the selected industry

Source: ExportPlanning - World Trade Datamart

The graphical representation paints a rather differentiated picture in terms of the performance of the different industries driving world trade in manufactured goods, both for the consumer and capital goods cluster and for the more upstream intermediate goods chains related to them.

Fashion system: strong increase in 2022 with recovery to pre-pandemic levels

For several sectors of the Fashion System, world demand - measured in constant prices - grew at double-digit rates in 2022. The Footwear, Leather Goods and Outerwear segments are the ones with the strongest increases, but positive results were also reported for Lingerie and Jewellery, Watches and Costume Jewellery. For most of these industries, the 2022 performance finally allowed them to recover their pre-pandemic values, closing the gap with the corresponding 2019 levels1. Growth 'normalisation' phenomena, on the other hand, characterised the dynamics of global demand for Sporting Goods, Bicycles and Musical Instruments, which grew at a particularly fast pace in 2020-2021 in the face of lockdown-induced changes in consumption.

'Normalisation' of demand for the Home System

Widespread negative dynamics, on the other hand, characterised the 2022 global demand for Home System products, after a two-year period 2020-2021 characterised by significant increases. Performance with a 'minus' sign was reported for world demand for Household Appliances, Lighting, Home Textiles and Consumer Electronics. Also moderately negative was the performance of world trade in Furniture and Furnishing Elements (-1.8%), after a two-year period with average annual growth of more than 5%. In all of these cases, however, world demand measured at constant prices is at levels well above pre-pandemic levels, reflecting how the slowdown in 2022 is to be interpreted as a physiological "normalisation" of the pace of development of demand, from the gradual downsizing of the focus on the enhancement of domestic spaces, strongly supported by the lockdown, as well as the possible impact of high energy prices in highly energy-intensive production sectors.

Agribusiness and Health Demand do not lose ground

2022 also confirms the high dynamism of global demand for healthcare (E4), albeit (naturally) at a more moderate pace than the pandemic two-year period 2020-2021. All the main segments end 2022 in positive territory, with the exception of disposable medical devices (-3%), reflecting an improving health picture. In addition, the growth performance of the Agro-food sector was consolidated, with global sales of pasta and rice marking the best result for the period (+9.7% in quantity); overall, the recovery in demand for products destined for the HO.RE.CA. channel became more robust.

Heterogeneous Dynamics for Intermediate and Capital Goods

A rather differentiated picture also for intermediate goods, reflecting the state of health of the related downstream supply chains. This is the case for the wood supply chain (B3), which shows the most significant declines, reflecting the normalisation of demand for the Home System described above, and for chemical intermediates (B5), given the plurality of destination sectors. While chemicals for the pharmaceutical and industrial industries remained largely in positive territory, world trade in quantities of Fertilisers, Paints and Varnishes and Dyes closed the year in decline.

For the capital goods cluster, a picture of substantial resilience emerges: the pace of expansion of demand for ICT Tools (F1) and the related supply chain (D1) continues, albeit at more moderate rates, just as trade in Industrial Equipment (F2) and Industrial Process Machines (F4) is not losing ground. The recovery of the automotive industry (F3 and D3) is also consolidating, although the picture of recovery to pre-crisis levels still looks very mixed: while the agricultural machinery and commercial vehicles segments are above 2019 values, world trade in motor vehicles (with the exception of the hybrid and electric chain), and heavy vehicles such as aircraft, trains and boats is not closing the gap yet.

The more positive closing of the year for world trade than initially assumed, with the relative resilience of investments, is therefore good news, although uncertainty, inflationary pressures and tighter monetary policies still represent current challenges in the global economic framework. In an ever-changing scenario, the 'real time' monitoring of economic information becomes increasingly relevant for exporters to optimise strategies and investments.

You may be interested in:

World Trade Trends: International Trade Results in Q2 2026 (Preliminary Estimates)

Published by Marcello Antonioni. .

Home items Fashion Food&Beverage Metal industry Intermediate goods Electronics Chemicals Industrial equipment Conjuncture Automotive Global demand Industries Global economic trendsStrengthening dynamics, driven by AI applications, and the green and digital transitions [ Read all ]

IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsPer il 2026 il Fondo ha rivisto lievemente al ribasso le stime di crescita del PIL mondiale, ora previsto al +3% [ Read all ]

US Trade Deficit Put to the Test by Tariffs: Evidence from First-Half 2026 Data

Published by Marzia Moccia. .

Slowdown Conjuncture United States of America Uncertainty Trade war Foreign market analysisAmid uncertainty that has now become the new normal, international geopolitical tensions, and the reshaping of the rules governing global trade, the United States undoubtedly remains a key focus of }... [ Read all ]