I quarter 2023: the world trade conjuncture between old and new phenomena

Highly uncertain environment remains, with highly differentiated sectoral trends

Published by Marzia Moccia. .

Slowdown Conjuncture Industries Uncertainty Global economic trendsThe international scenario remains deeply marked by uncertainty: while on the one hand, the global economy is gradually recovering from the negative effects of the Russian-Ukrainian conflict and the related disruptions in the energy and food markets, as well as from the consequences of the pandemic context, with a recovery of the Chinese economy and an easing of disruptions in the supply chains, on the other hand, the situation still remains fragile. Indeed, weighing most heavily on the economic outlook is a more persistent inflation than initially assumed and the resulting massive and synchronised tightening of monetary policy by the world's major central banks, as documented in the latest World Economic Outlook release.

This international context has naturally led to a slowdown in the pace of growth of world trade, which has occurred especially since the last quarter of last year.

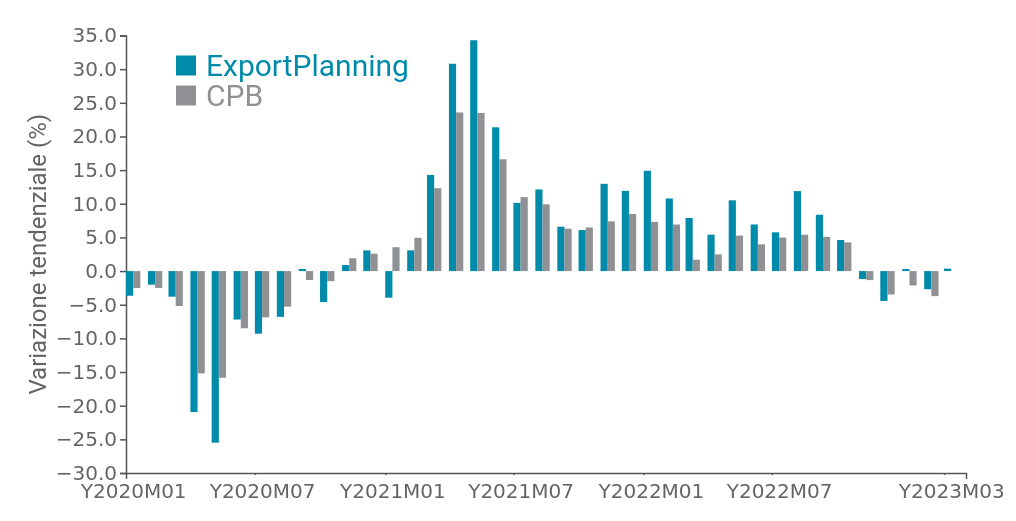

For much of 2022, in fact, world trade proved more resilient than initially assumed. This phenomenon is evident from Fig.1, which shows the series of monthly quarterly changes in world trade in manufactured goods in quantity, comparing data collected and systematised by ExportPlanning with those of the Central Planning Bureau, which in turn collects and processes information on international trade in goods.

Fig.1 - World trade in quantity

(CPB data vs. ExportPlanning data, trend change)

Fonte: Elaborazioni ExportPlanning.

Both sources make it possible to document how, after showing renewed vigour post-Covid, the dynamics of world trade in manufactured goods entered negative territory right from the last months of 2022, remaining so in the first quarter of the new year.

Overall, ExportPlanning pre-estimates show a trend change of -0.2% in the first three months of 2023 compared to the same period last year.

The slowdown of world trade by industry

At this point, it is significant to investigate how the slowdown in world trade is being reflected in the various industries that drive international trade in goods.

The graph below positions on the x-axis the change 2022 over 2021 and on the y-axis the change first quarter 2023 over the same period 2022. Through this representation, it is possible to highlight the most resilient/slowest industries.

Fig.2 - International trade at constant prices by industry

Positioning the mouse over the circle identifying an industry displays a table summarising the data on the average annual variation of the selected industry

Source: ExportPlanning - International Trade Datamart

The proposed graphical representation clearly shows that the most significant slowdowns are mainly affecting world trade in goods upstream of the supply chain: international trade in commodities (A1 and A2), and almost all intermediate goods, with the sole exception of components for transport equipment (D3), are clearly decelerating. It is possible that, in anticipation of lower prices, downstream companies and traders are reducing their purchases, using the stocks accumulated during 2021 and the first part of 2022.

The picture for capital goods, on the other hand, is more differentiated: first of all, the recovery of Transport Equipment (F3, as also shown by the dynamics of D3 components), which had closed 2022 still at levels lower - in quantity - than pre-Covid levels, continues.

In addition, trade in Plant Engineering (F5) and Industrial Equipment (F2) was also in positive territory, indicating a possible resilience of long-term investment decisions by companies, despite a downward outlook, in the face of intensifying international financial risks; on the other hand, demand for Machinery (F4) was down.

Particularly significant appears to be the continuation of the pace of growth in world trade in Electrical Engineering (D4), driven by the results of the "Motors, Generators and Electrical Transformers" segment, which brings the industry to values that are far higher - in quantity - than those before the pandemic crisis, and is an indirect proxy for the energy transition phenomenon.

In contrast, the reduction in trade in ICT Tools (F1) is mainly attributable to a normalisation phenomenon, in contrast to the marked growth that has affected the sector in recent years.

The picture for the consumer goods cluster appears largely positive: foodstuffs, both fresh (B1) and packaged (E0) slow down but do not decline, as does the health goods chain (E4). The most significant exception is represented by the Household System (E3) and the related supply chain (B3 and C1), which after the marked growth achieved in the pandemic period, now seems to be penalised by the shift in consumption preferences, oriented more towards mobility and social occasions outside home.

Conclusions

In a particularly complex international conjuncture, the world trade data thus make it possible to document the progressive consolidation of particular types of phenomena, from upstream to downstream of the supply chain: first of all, the reorganisation of world consumption preferences appears to be solid, with a return of attention to mobility and social occasions away from home. Moreover, companies' purchasing decisions appear to be more prudent, especially in terms of purchasing intermediate goods and machinery, but long-term investments seem to be holding up. Transversally, the phenomenon of energy transition is becoming increasingly important, with consequent anti-cyclical trends.

You may be interested in:

Footwear: how are the manufacturing Countries performing in the first half of 2026?

Published by Mauro Badanelli. .

Conjuncture Industries Foreign markets International marketingAfter analyzing the dynamics of global trade in footwear machinery in a previous article, attention now shifts to the finished product, in order to examine the most recent performance of the main foot}... [ Read all ]

Export 2026-2029: ExportPlanning updates its forecast scenario

Published by Marzia Moccia. .

Conjuncture Export markets Uncertainty IMF Global economic trendsFor exporting companies, the ability to promptly interpret the evolution of international markets is now a key competitive factor. In a global context characterized by rapid changes and growing unce}... [ Read all ]

Footwear Machinery: the map of Growing and Slowing markets in Q2 2026

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Foreign markets International marketingFor exporting companies, the international context is changing increasingly rapidly. Relying on consolidated year-end data often means arriving too late. Having indicators updated to the second quarte}... [ Read all ]