Monetary policy stance: Norway bucking the trend

Europe’s main oil exporter is heading towards normalization.

Published by Alba Di Rosa. .

Exchange rate Europe Uncertainty Exchange rate risk Oil Central banks Exchange ratesYesterday Norges Bank, the Norwegian central bank, released useful information about its monetary policy stance in the coming months. Although the reference interest rate is currently unchanged at 1%, a hike in June is highly likely. The bank is therefore following a different path compared to major central banks, such as the Fed, the ECB and the Bank of Japan.

- The FED slowed monetary policy normalization: after raising fed funds rates 4 times in 2018, reaching the 2.25-2.5% target range, the bank is now in wait-and-see mode.

- The ECB is still keeping rates at around 0. Even if the QE ended in 2018, the bank is currently reinvesting principal payments from maturing securities purchased under the asset purchase programme. This will go on “as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation”.

- The BoJ is keeping rates at zero and plans to "persistently continue with powerful monetary easing".

Even neighboring Sweden remains in negative territory. On the contrary, Norges Bank raised rates in September 2018 for the first time in 7 years, and raised them further in March. According to on the information released yesterday, the next increase is expected to take place in June.

It is therefore clear that a gradual normalization is underway, given the good conditions of the economy. Yesterday Olsen, president of the central bank of Sweden, stated that “capacity utilisation in the Norwegian economy is slightly above a normal level”, while “underlying inflation is a little higher than the 2 percent inflation target”.

Oil and economic recovery

According to Olsen, the current good health of the Norwegian economy is the result of a solid growth that has taken place since the autumn of 2016, supported by a positive outlook for the global economy, low interest rates and oil prices on the rise after the 2014 fall. As a matter of fact, Norway is a major oil exporter (the biggest exporter in Europe, the eleventh world’s largest exporter); therefore, economic and currency dynamics are closely linked to its price.

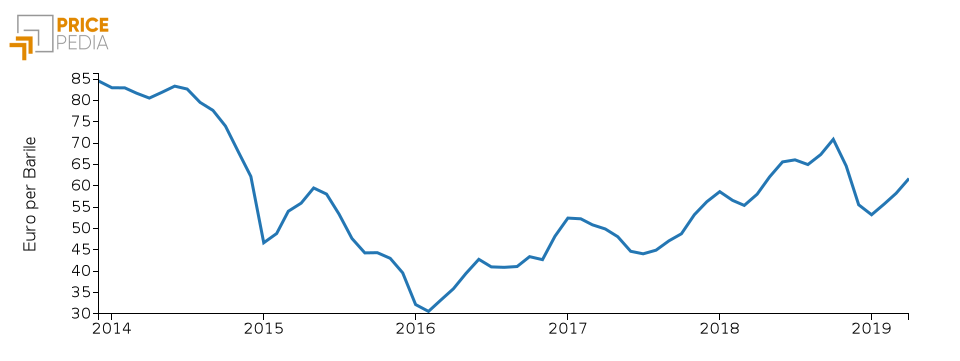

As you can see from the chart below, the price of oil collapsed in 2014 and then recovered in 2016. Between 2016 and the present, the price has almost doubled.

Monthly price: Crude oil, €/barrel

Source: PricePedia.

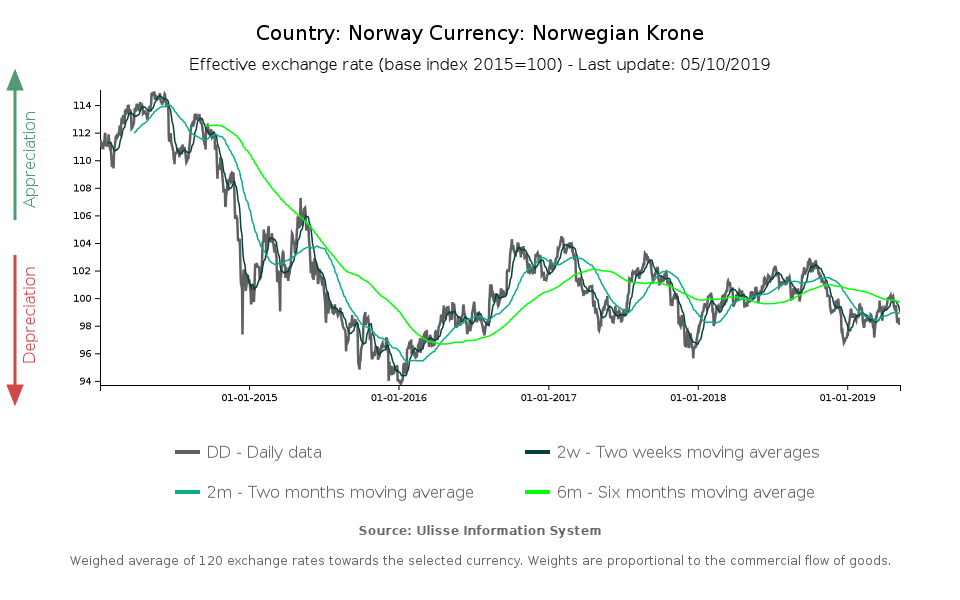

Similarly, Norwegian Krone effective exchange rate collapsed in 2014, recovered in 2016 and then stabilized in 2017 around a significantly lower level, compared to the average recorded in the first decade of the 2000s.

The Krone has therefore been quite weak since 2014, despite a recovery in oil prices. The president of the Norwegian central bank pointed out that a weak currency has been supporting exports, but at the same time it has caused an increase in the prices of imported goods, fueling inflation.

Looking at the most recent dynamics, the weakening of the Krone started in October 2018 has coincided with a new reduction in oil prices, together with the climate of generalized uncertainty on financial markets.

The outlook of the risks to the Norwegian economy is therefore relatively limited from the national point of view; on the contrary, looking abroad, trade war and political tensions that marked the global scenario in recent months cannot be overlooked, since they impact financial markets sentiment and global demand.

You may be interested in:

IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsPer il 2026 il Fondo ha rivisto lievemente al ribasso le stime di crescita del PIL mondiale, ora previsto al +3% [ Read all ]

US Trade Deficit Put to the Test by Tariffs: Evidence from First-Half 2026 Data

Published by Marzia Moccia. .

Slowdown Conjuncture United States of America Uncertainty Trade war Foreign market analysisAmid uncertainty that has now become the new normal, international geopolitical tensions, and the reshaping of the rules governing global trade, the United States undoubtedly remains a key focus of }... [ Read all ]

Global Economic Outlook: International Trade Results for April 2026

Published by Marzia Moccia. .

Conjuncture Industries Uncertainty Global economic trendsThe data for April 2026 document the continuation of an expansionary phase in international trade, albeit with significant differences at the product level. [ Read all ]