Thai Baht: Pulling the Brake

Worries over economic competitiveness and Coronavirus effect impact on the currency.

Published by Alba Di Rosa. .

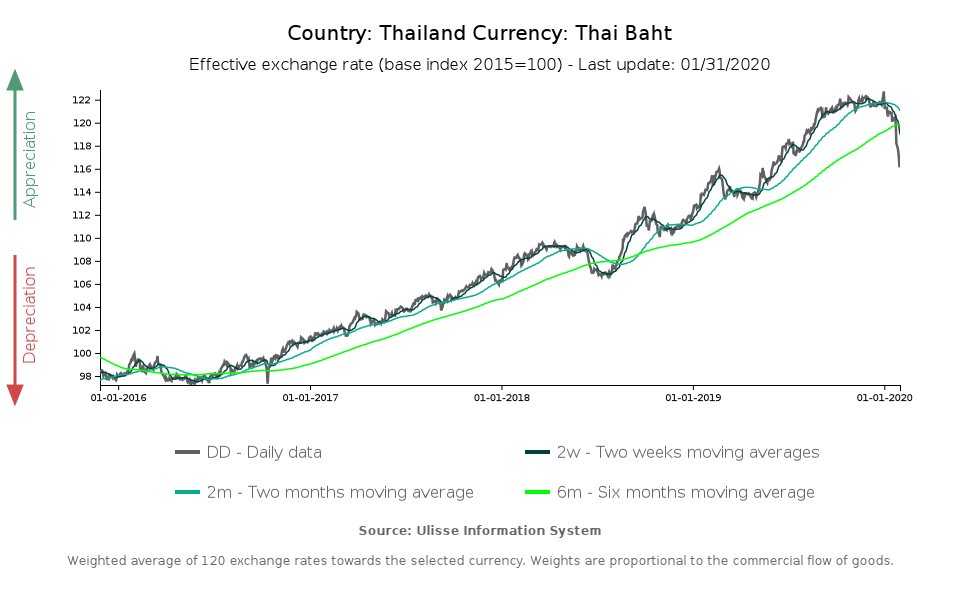

Exchange rate Asia Emerging markets Trade balance Uncertainty Exchange rate risk Central banks Exchange ratesAmong this week's financial headlines, one of the most relevant involves the great turnabout of the Thai baht. After a continuous appreciation since early 2016 - which led the currency to strengthen by 23% over 4 years in terms of effective exchange rate (EER) - the baht has experienced a significant depreciation since the beginning of January: -5.3% (EER), as can be seen from the graph below.

The factors that help explain this dynamics can be traced back to domestic and international elements.

Thai central bank: stemming the strong baht to safeguard economic competitiveness

As written in previous articles, the appreciation trend shown by the baht is supported by several factors:

- A positive current account balance, in which a buoyant tourism industry plays a key role

- The high amount of foreign currency reserves ($214bn in November, according to ExportPlanning data) held by the Bank of Thailand (BoT), that have increase investors’ trust in the baht, to the point where it has gained credit as a new safe haven

At the beginning of last year, we crowned the baht as 2018 best performer in Southeast Asia (3.6% appreciation in terms of EER). In 2019 the currency confirmed this role, gaining 7.3 percentage points.

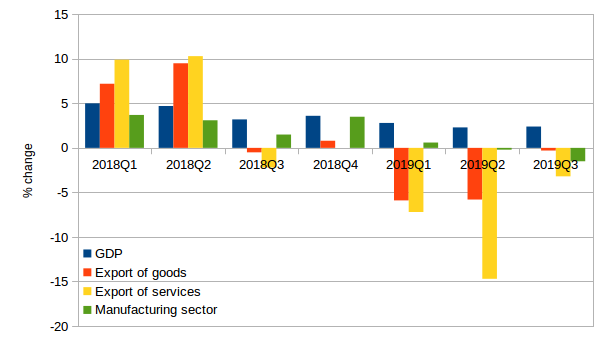

However, as is well known, a very strong currency penalizes a country's economic competitiveness. In recent months, Thai institutions have started to perceive this issue as an urgent matter, also in the face of an economic situation marked by slowdown (in terms of GDP) and contraction (in terms of exports) during 2019.

Thailand: main economic indicators,

y-o-y % change (2018Q1-2019Q3)

Source: StudiaBo elaborations on NESDC data.

In November, the Bank of Thailand introduced measures aimed at stemming the strength of the baht: reference interest rate cut, from 1.5% to 1.25%, and relaxation of regulations to facilitate capital outflows.

In the Monetary Policy Report released in early January, the BoT reiterated its concern about the strength of the baht and stated that other measures would also be introduced, if necessary. The Finance Minister also expressed his willingness to cooperate with the BoT, in terms of fiscal policy, in managing the strength of the baht.

The Coronavirus effect

In addition to the action of Thai policy-makers, another element that, in the last week, has significantly contributed to the weakening of the baht is the Coronavirus emergency. A climate of panic has in fact been spreading in financial markets in relation to the Chinese epidemic.

For Thailand in particular, the epidemic is perceived as a risk factor as it threatens the tourism industry, a key resource for the national economy. At least in the first part of 2020, Thailand is likely to witness a marked reduction in the number of international tourist arrivals and, first of all, of Chinese tourists, due to the travel restriction to and from China.

One quarter of Thai tourism revenues come from Chinese tourists (source: ING), and China also represents the main export market for Thailand. A demand slowdown, due to the state of sanitary emergency, could therefore undermine the strength of Thai current account surplus.

However, Thailand is not the only one feeling the hit of the current negative climate on financial markets. Major stock exchanges around the world have been recording losses in the last week, while the Vix Index ("the fear index"), reached a peak on January 27.

On currency markets, safe-haven currencies show a general appreciation trend, proving an increase in risk aversion.

Oil prices felt the blow as well, falling out of fear of the economic consequences of the epidemic, which could affect global demand for raw materials.

You may be interested in:

IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsPer il 2026 il Fondo ha rivisto lievemente al ribasso le stime di crescita del PIL mondiale, ora previsto al +3% [ Read all ]

US Trade Deficit Put to the Test by Tariffs: Evidence from First-Half 2026 Data

Published by Marzia Moccia. .

Slowdown Conjuncture United States of America Uncertainty Trade war Foreign market analysisAmid uncertainty that has now become the new normal, international geopolitical tensions, and the reshaping of the rules governing global trade, the United States undoubtedly remains a key focus of }... [ Read all ]

Global Economic Outlook: International Trade Results for April 2026

Published by Marzia Moccia. .

Conjuncture Industries Uncertainty Global economic trendsThe data for April 2026 document the continuation of an expansionary phase in international trade, albeit with significant differences at the product level. [ Read all ]