EU Agri-food Exports in 2020

Opposite dynamics for exports of Agri-products for retail consumption and for the Horeca channel

Published by Marzia Moccia. .

Covid-19 Conjuncture Global economic trendsThe global health crisis and the related containment measures have exerted a significant impact on the consumer goods industry, strongly penalizing consumption categories of discretionary and/or durable consumer goods. Over the past year, the priorities of international consumers have naturally focused on satisfying essential needs, supporting the demand for health, hygiene, cleaning and food products.

Thanks to global demand, the Agri-Food sector is one of the sectors that has shown the most resilience in the current economic situation, although it cannot be considered completely free from damage. The intensity of the resilience of the various segments has in fact been differentiated according to the different channels of destination: while, on the one hand, there has been a consolidation of consumption in the domestic sector, on the other hand the closures imposed on restaurants (and bars), as well as restrictions on the mobility of people and tourist flows, have severely penalized the segment of Horeca products, as anticipated in the article HORECA products: Monthly Trade Figures.

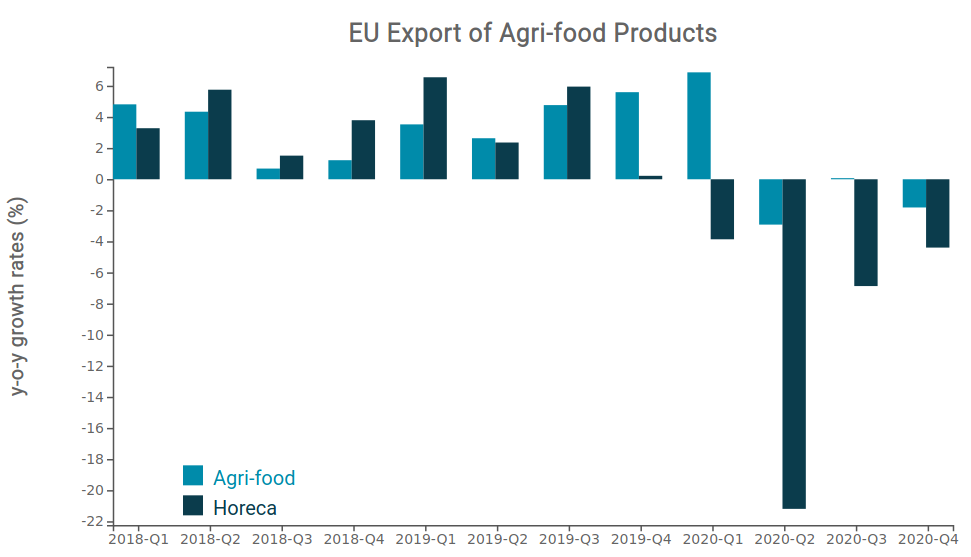

The dynamics of EU exports of agri-food products

The information on the dynamics of EU exports during the last year allows to certify previous considerations: the following graph shows the y-o-y variation in euro (compared to the corresponding quarter of the previous year) of European exports of Agri-food products, tipically for retail sale, and of Horeca products, mainly sold and distributed through the channel of bars and restaurants.

Source: ExportPlanning

From the graph above, it is clear that the performance of EU exports of Agri-food products was relatively different from that of Horeca ones for almost the whole of 2020: during the quarters following the outbreak of the health emergency, EU exports of Agri-food products in fact limited their losses to around -2%, while Horeca exports showed much more marked declines. After posting its worst result in the second quarter of the year (down 21%), European exports in this sector began to gradually recover ground, although without ever regaining their pre-crisis levels. Overall, at the end of 2020, European agri-food exports closed the year substantially stable (+0.5%) compared to last year, against a -9% contraction in exports of Horeca products.

In order to be able to investigate in detail which sectors have been more sustained or penalized by the international economic situation, the graph below shows the dynamics of the main EU agri-food export segments on the basis of the y-o-y rate of change recorded in 2020 (x-axis) and that shown in the last quarter of 2020 (y-axis); the size of each ball is proportional to the 2019 value of exports in euro.

Source: ExportPlanning

In the top right area of the chart, you can identify the products that have shown the most significant growth performance over the past year. These are typically products of the so-called "Mediterranean diet", such as Fruits and vegetables (B1.21, E0.24), fresh and packaged, Oil and condiments (B1.51, E0.12) and Packaged pasta and rice (E0.15).

In the middle of the chart you can find the sectors that have shown substantial resilience, marked by a higher EU export value than the first group. Here we can find Packaged meat and fish (E0.22), Dairy products (E0.14), Vegetables and legumes (B1.31) and Bakery products and confectionery (E0.31, E0.32).

Exports of fresh and frozen meat deserve a separate discussion: on the whole, European exports of the sector contained losses, for an overall drop of -1% in 2020. However, the significant contraction that characterized the last quarter of 2020 (-8% compared to Q4-2019) must be attributed to a normalization phenomenon following last year's sales spike due to the boom in exports to China as a result of the swine fever outbreak.

Particularly significant was the resilience of Coffee exports (E0.33), which showed a relatively stable performance compared to 2019, signaling how domestic coffee consumption replaced and offset consumption through the Horeca channel.

On the other hand, the bottom left area contains the segments that showed a decline in 2020. As anticipated, these are products primarily destined for the Horeca channel, particularly Alcoholic beverages (E0.42) and Fish products (B1.13), along with products widely used in alcohol production such as Levites and malts (B1.61). All three product categories ended 2020 in negative territory, and performance relative to Q4-2020 also reports lower export values than in the corresponding period last year.

Conclusions

As anticipated, the 2020 results of European exports certify the transfer of consumption of agri-food products within the domestic sphere, with a strong penalization of the restaurant, hotel and catering channels that affected the whole of 2020, due to the reduced levels of operation of the service sector and the strong limitations to the mobility of people, that still exist. Moreover, while on the one hand the major European export sectors, such as the meat and dairy segments, showed substantial stability compared to last year, it was above all the pasta, oil and fruit segments that showed strong growth. This result strongly supported the growth of exports from the Member States most specialized in their production, such as Italy, Spain and Greece.

You may be interested in:

Global trade in footwear machinery: China dominates, Italy leads the way in premium technology

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Foreign markets International marketingThe footwear machinery industry represents one of the pillars of manufacturing innovation in the fashion sector. In an increasingly competitive environment, characterized by global markets, growing }... [ Read all ]

World Trade Trends: International Trade Results in Q2 2026 (Preliminary Estimates)

Published by Marcello Antonioni. .

Home items Fashion Food&Beverage Metal industry Intermediate goods Electronics Chemicals Industrial equipment Conjuncture Automotive Global demand Industries Global economic trendsStrengthening dynamics, driven by AI applications, and the green and digital transitions [ Read all ]

US Trade Deficit Put to the Test by Tariffs: Evidence from First-Half 2026 Data

Published by Marzia Moccia. .

Slowdown Conjuncture United States of America Uncertainty Trade war Foreign market analysisAmid uncertainty that has now become the new normal, international geopolitical tensions, and the reshaping of the rules governing global trade, the United States undoubtedly remains a key focus of }... [ Read all ]