New release of exchange rate risk indicator

Background on four country clusters

Published by Giulio Corazza. .

Exchange rate Dollar Euro Exchange rate risk Internationalisation toolsOne of the main risk factors to consider when undertaking an internationalization process is exchange rate fluctuations.

The exchange rate risk takes on different aspects depending on the time period over which it is assessed. In the short term it represents the risk associated with a lower collection amount associated with trade receivables expressed in a foreign currency. In the medium-long term it represents the risk that the purchasing power of potential customers present on the foreign market undergoes a significant reduction, so much so as to modify their propensity to purchase the goods offered by the company.

The first short-term exchange rate risk can be easily managed by hedging the risk associated with receivables expressed in foreign currency. The management of the second medium-long term risk is more complex, it is the responsibility of the company, and requires a continuous adaptation of the supply conditions of the good/service by the company in order to take into account the changes on the foreign market induced by the changes in the exchange rate. This management has, of course, a cost, the ex-ante evaluation of which is proportional to the medium/long-term exchange rate risk.

The exchange rate risk indicator developed by ExporPlanning measures only the medium-long term risk. It is composed of three pillars:

- Exchange rate equilibrium in terms of purchasing power parity (PPP), based on past and future trends in the country's relative inflation.

- Current currency resource availability, generated by the country's trade in goods and services with the rest of the world.

- Credibility of the country and currency, derived from the quality of the country's institutions, its monetary and currency policy.

For more information on the subject please refer to the previous methodological article: Export risks: focus exchange rate risk

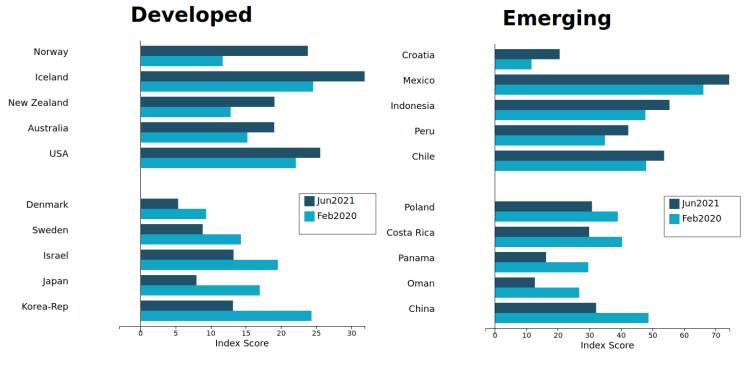

ExportPlanning's medium- to long-term exchange rate risk index ranges from 0 to 100 and measures the depreciation risk associated with the currencies of 152 countries around the world. This new version of Export Planning exchange rate risk, incorporates the gradual stabilization of financial markets following the pandemic crisis. In light of the profound changes that have affected the economic fundamentals of all countries around the world in the wake of the pandemic crisis, a comparison with the previous publication (February 2020) may be useful to see which countries have seen their risk increase and which have seen it decrease significantly. The following charts show this comparison for four country clusters: developed, emerging, frontiers, and least developed.

Exchange rate risk: focus on developed and emerging countries

Currencies that are part of the first cluster of developed countries have generally seen an improvement in medium- to long-term exchange rate risk. However, there is no shortage of instances where these have become riskier:

for example, the United States and Austrialia, despite having an extremely low synthetic risk index of around 20 points, have both experienced a slight increase in riskiness. This worsening is partly due to an increase in inflation forecasts, and for the United States, to a decrease in its current reserves, generated by trade in goods and services with the rest of the world.

of goods and services with the rest of the world.

In contrast, countries that have seen an improvement include Denmark and several Western European countries in general. For Denmark, this is due to a decrease in inflation expectations, relative to the average inflation of the world economy.

Turning to the emerging countries, those that have seen a deterioration include Mexico, Indonesia, Chile and Peru. For these countries, the main reason is the decrease in the credibility of the countries due to the weakness shown

institutions in the management of the current epidemiological emergency.

Mexico also sees a substantial decrease in its reserves generated by the current balance.

On the other hand, a clear improvement characterizes China. This is due in part to a decrease in expected relative inflation and in part to an increase in credibility.

and partly due to an increase in the credibility of the country and its currency. In fact, China shows an improving trend in the

quality index of institutions. In addition, the country's monetary and currency policy has resulted in a significant appreciation of the Yuan's effective exchange rate since the end of 2019, reinforcing markets' expectations of its

its stability.

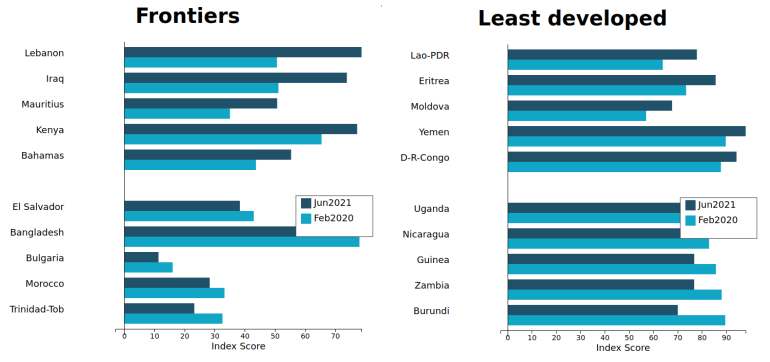

Exchange rate risk: focus on frontier and least developed countries

In contrast, the frontiers and least developed countries clusters saw a general worsening in the index.

As can be seen from the charts, these economies often have much higher exchange rate risk than the more developed countries. Even with tentative signs of improvement in some cases, they still remain high risk countries.

You may be interested in:

Amid tariffs and uncertainty, the downsizing of US imports continues

Published by Alba Di Rosa. .

Dollar United States of America Trade balance Export Trade war Import Foreign market analysisThe US Census Bureau recently released the latest foreign trade data, updated as of February 2026, and now available on the ExportPlanning platform [ Read all ]

January 2026: the latest data on global trade in goods

Published by Marzia Moccia. .

Slowdown Exchange rate Conjuncture Dollar Euro Foreign markets Uncertainty Global economic trendsThe availability in the ExportPlanning Information System of global trade data for January makes it possible to update the short-term outlook on the most recent dynamics of world trade in goods, wit}... [ Read all ]

Trump 2.0: How Effective Is U.S. Tariff Policy?

Published by Marzia Moccia. .

Dollar United States of America International marketingPrime evidenze in relazione agli obiettivi economici dichiarati [ Read all ]