World Trade Figures in Q1 2022: Performance by Industry

General slowdown in the pace of growth, which nevertheless remains generally positive

Published by Marcello Antonioni. .

Slowdown Conjuncture Global demand Industries Uncertainty Global economic trendsIn the first quarter of 2022, world trade confirmed the signs of a slowdown already highlighted at the end of 2021. In particular, in the first three months of the year, world trade in goods, while confirming an upward trend in constant prices, showed a further deceleration in the pace of development, falling from +9.9 per cent trend in Q4 2021 to +4.9 per cent Y-o-Y trend in the most recent quarter.

The slowdown compared to the average pace of 2021 appears to be generalised to (almost) all industries

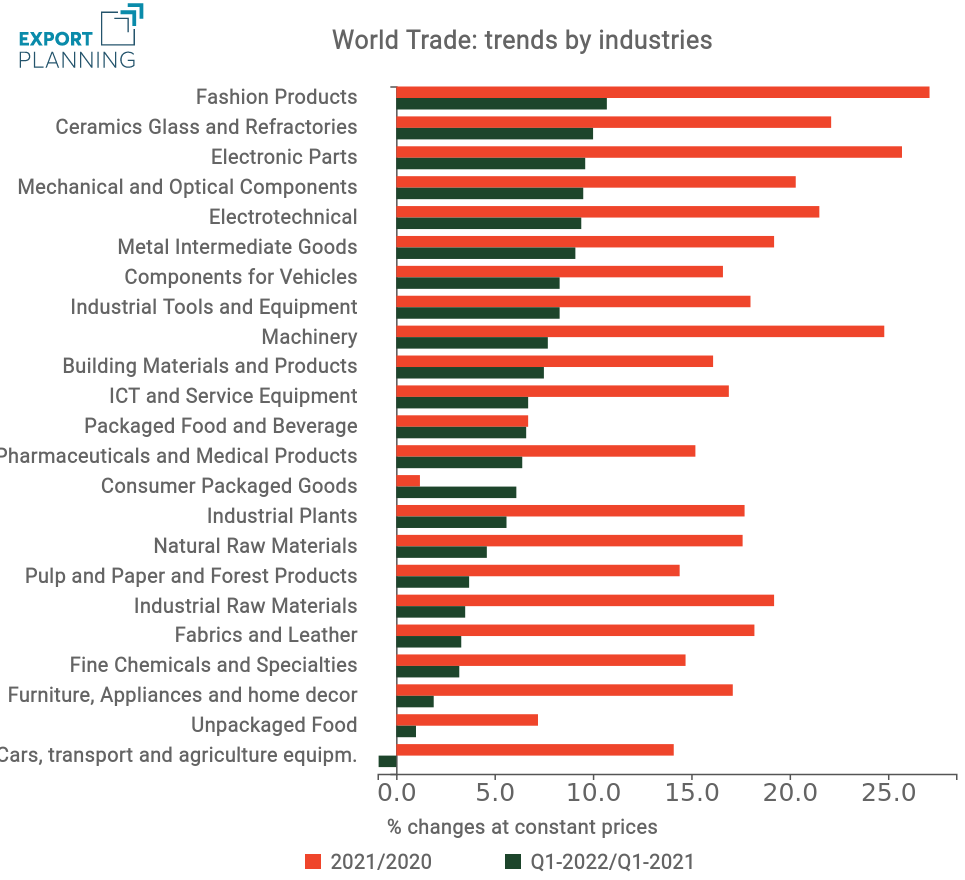

Considering the average performance in 2021 (when world trade grew by 19 per cent in constant prices), the slowdown is particularly significant. Moreover, the slowdown appears to be rather generalised across industries.

Source: ExportPlanning-World Trade Datamart

Against an average slowdown of more than 14 percentage points (calculated as the difference between the pace of growth in 2021 and that of the first quarter of 2022), particularly significant slowdowns were seen in the industries of Machinery (with a negative differential of more than 17 percentage points), Fashion products, which, although showing the most favourable growth performance in the first three months of 2022 (+10. 7% at constant prices), suffer a negative differential of more than 16 percentage points compared to the average 2021, Electronic Parts (which lose 16 percentage points in the most recent growth rates compared to the average 2021) and Furniture, Appliances and home decor, which - with a negative differential of more than 15 percentage points - lose positions in the ranking of the fastest growing industries. Last but not least, it is worth highlighting the case of Cars, transport and Agricultural Equipment, which - with a trend performance that became slightly negative in the first quarter of the year - falls to last place in terms of trend performance in the first quarter of the year and slows down by around 15 percentage points compared to the 2021 average.

On the other hand, there are a number of industries that do not see any significant slowdown, but rather in some cases accelerate. This is the case, for example, of Consumer Packaged Goods, which - after a 2021 that had recorded weak growth in world trade at constant prices - in the first quarter of the year increased its growth rate by 5 points (rising to +6.1% at constant prices). Also worth mentioning is the case of the Packaged Food and Beverages industry, which in the first quarter of the year (+6.6%) essentially maintained the same trend rates of world trade that had characterised 2021.

Intermediate cases, with actual slowdowns in world trade compared to the 2021 average but not particularly pronounced (within 10 percentage points), are Components for Vehicles (with growth in the first quarter of the year halved compared to the 2021 average), Pharmaceuticals and Medical Products (down from +15.2 per cent in 2021 to +6.4 per cent in the first quarter of 2022) and Industrial Tools and Equipment (with growth halving from 18 per cent in 2021 to +6.4 per cent in the first quarter of 2022).

Conclusions

Although further slowing down compared to previous quarters, the first three months of 2022 showed world trade still growing at constant prices. All the industries analysed (with the sole - albeit limited - exception of transport and agricultural equipment) all recorded a "plus" sign in the trends for the first quarter of the year, demonstrating that, to date, world trade has not been in recession.

However, there is no doubt that the recent rate of growth has slowed down compared to last year, which was also a special year - marked by a technical "rebound" in the second quarter of the year (a recovery from the Great Lockdown of Q2 2020). Moreover, it should of course be stressed that this is a period that has not yet been significantly impacted, on the one hand, by the beginning of the Russian-Ukrainian conflict and, on the other, by the extensive lockdowns imposed by the Chinese authorities on Shanghai to counter the resurgence of the pandemic.

Therefore it will be important to observe the evolution of world trade in this second quarter of the year in order to understand whether the foreign channel can continue - despite elements of uncertainty in the most recent period - to make a positive contribution to the development of world economies.

In the meantime, it is strategic for exporting companies to be able to measure the performance of the various markets in which they operate and assess their own performances against that of the various competitors present in these markets1.

1) For this purpose, see ExportPlanning's Market Barometer tool, which allows, for a given product/sector/industry and market, to monitor the quarterly sales evolution of the different (country) competitors on the market.

You may be interested in:

Footwear: how are the manufacturing Countries performing in the first half of 2026?

Published by Mauro Badanelli. .

Conjuncture Industries Foreign markets International marketingAfter analyzing the dynamics of global trade in footwear machinery in a previous article, attention now shifts to the finished product, in order to examine the most recent performance of the main foot}... [ Read all ]

Export 2026-2029: ExportPlanning updates its forecast scenario

Published by Marzia Moccia. .

Conjuncture Export markets Uncertainty IMF Global economic trendsFor exporting companies, the ability to promptly interpret the evolution of international markets is now a key competitive factor. In a global context characterized by rapid changes and growing unce}... [ Read all ]

Footwear Machinery: the map of Growing and Slowing markets in Q2 2026

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Foreign markets International marketingFor exporting companies, the international context is changing increasingly rapidly. Relying on consolidated year-end data often means arriving too late. Having indicators updated to the second quarte}... [ Read all ]