Machinery and equipment: economic analysis of world trade

In the current international scenario, the capital goods industry is being characterized by relative resilience. An in-depth look at sectoral trends

Published by Marzia Moccia. .

Slowdown Internationalisation Global demand Uncertainty Global economic trendsIn an international scenario characterized by tightening financial conditions, in the face of restrictive actions by major central banks to deal with more persistent inflation than initially assumed, a particularly interesting indicator to monitor is world trade in investment goods. The latter, in fact, can be a building block in reading what is the "sentiment" of firms around the world and their relative choices in terms of capital goods.

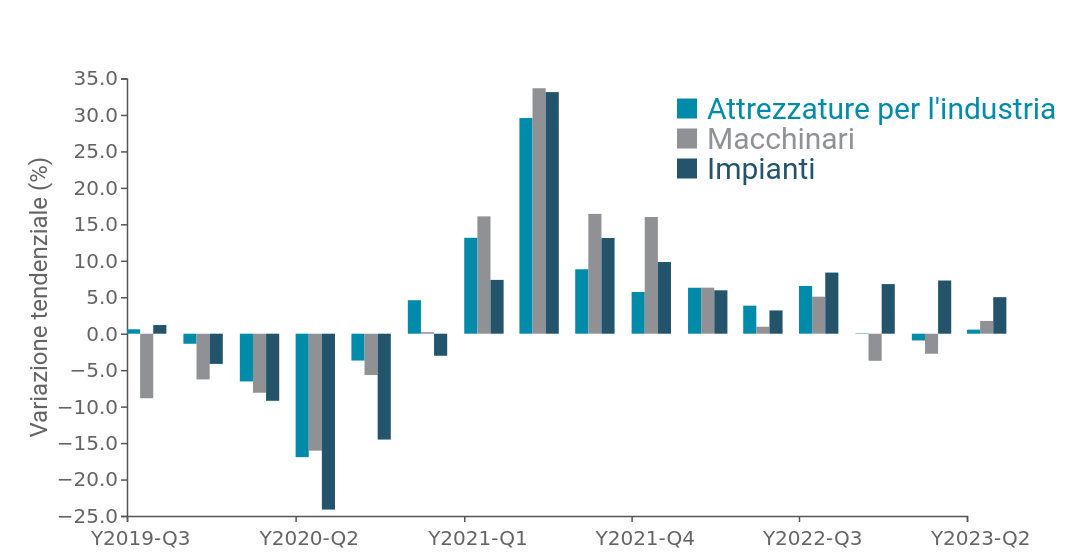

As anticipated in the article First signs of the start of a global energy transition pathway, the latest available information, covering the first half of the new year, testifies to a relative resilience of the capital goods industry, with rates of change in line with those of last year. In particular, the following graph shows the quarterly dynamics at constant prices, that is, adjusted for price and exchange rate dynamics, of the main capital goods industries, distinguishing between the Machinery, Industrial Equipment and Industrial Tools sectors.

Fig.1 – Machinery and Equipment: world demand at constant prices

(Change over the corresponding period of the previous year)

Source: ExportPlanning.

On a medium-term horizon, it seems clear that, after the penalties experienced in the pandemic year, 2021 and much of 2022 were characterized by a robust revitalization of international trade in the three segments. The new expansive cycle also made it possible to reverse a negative trend already visible during 2019, when intensified trade tensions had triggered a downsizing of trade in the segment. However, for the Machinery and Equipment sectors, the new season of increases came to a halt in late 2022, in line with worsening levels of economic activity, thus entering negative territory. The first few months of the new year, however, did not mark a worsening of the recessionary pace; indeed, data for the second quarter testify to its partial easing.

Also of particular interest is the dynamics of world demand for Plant Engineering, which appears to be characterized by holding up well, still remaining in positive territory and trending upward at constant prices.

The sectoral framework

The bubble map below places the different sectors pertaining to capital goods based on the rates of change in imports from them in 2022 (X-axis) and the first half of 2023 (Y-axis). Imports are measured at constant prices to allow for a reading of real dynamics, net of price changes.

The bisector is plotted in the map, which allows for highlighting the segments (positioned above it) that recorded accelerating rates of change in the first half of 2023 compared to last year.

Fig.2 – Machinery and Equipment: world demand at constant prices by segment

By hovering the mouse over the circle identifying an industry, a table can be displayed that summarizes the annual and six-month change data for the selected industry

Source: ExportPlanning - Datamart World Conjuncture

In particular, it appears evident that the totality of the sectors pertaining to Plant Engineering (F5) are on rates of change in line with last year's, if not higher, positioning themselves above or near the bisector.

More differentiated, however, appears the picture for the Machinery sector (F4): the economic situation still appears favorable for Food Machinery (F4.36) and Metal Machine Tools (F4.32), while Packaging Machinery (F4.38) appears to be rebounding.

Closing out the first half of the year in negative territory were Special Purpose Machinery (F4.37) and Semiconductor Machinery (F4.29), where the latter result was mainly due to the export squeeze put in place by technology-holding countries (the United States, the Netherlands and Japan) against China, the top importing country.

Also slowing down markedly appears to be Equipment for Industry (F2), with the only exception of Measuring Instruments (F2.51).

Conclusions

Foreign trade statistics for the capital goods industry (Machinery and Equipment) returns a picture of relative resilience to the current economic situation, with positive rates of change close to those of last year.

However, the capital goods industry is one in which the discrepancy existing between order intake and delivery is among the highest, affecting, therefore, the correct interpretation of results. Documented tightness may in fact reflect a lag between investment decisions and delivery of purchased goods. If this is the case, the economic data tend to document the persistence of a growth phase due to earlier investment decisions, which may be running out.

According to the latest publication of the Global Manufacturing PMI, "real-time" indicator of the outlook regarding industrial activity levels, expectations related to the production of Investment Goods has in fact experienced a deterioration over the most recent months, falling below the threshold of 50 as of February 2023.

Consistent signals also come from UCIMU data, the association of Italian machine tool, robot and automation manufacturers, documenting a marked slowdown in order intake during the first part of 2023.

You may be interested in:

Export 2026-2029: ExportPlanning updates its forecast scenario

Published by Marzia Moccia. .

Conjuncture Export markets Uncertainty IMF Global economic trendsFor exporting companies, the ability to promptly interpret the evolution of international markets is now a key competitive factor. In a global context characterized by rapid changes and growing unce}... [ Read all ]

World Trade Trends: International Trade Results in Q2 2026 (Preliminary Estimates)

Published by Marcello Antonioni. .

Home items Fashion Food&Beverage Metal industry Intermediate goods Electronics Chemicals Industrial equipment Conjuncture Automotive Global demand Industries Global economic trendsStrengthening dynamics, driven by AI applications, and the green and digital transitions [ Read all ]

IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsPer il 2026 il Fondo ha rivisto lievemente al ribasso le stime di crescita del PIL mondiale, ora previsto al +3% [ Read all ]