A Slowing global Trade: a Geographical and Sectoral profile

The weakness in world demand for goods is generalised, but its intensity varies in geographical and sectoral terms

Published by Marzia Moccia. .

Conjuncture Global economic trends

Since the last months of 2022, the global manufacturing industry has shown evidence of a substantial slowdown, which has been reflected both on the production volume front and on the dynamics of international trade in goods.

As anticipated in the article III quarter 2023: world trade conjuncture, the latest foreign trade statistics for the 3rd quarter of the year, available at the link, show the continuation of weak global demand: the latter, after ending the first quarter with a 3.6 percent fall, contracted a further 5.6 percent in the March-June period and 3.8 percent in the June-September period.

The weak international economy reflects, with some lag, the effects of tighter monetary policies put in place by major central banks to deal with more persistent inflation than initially assumed.

Although the slowdown in global demand for goods appears to be generalized to all the major economies and all the different industries that drive trade, the intensity with which it is manifesting itself nevertheless appears differentiated in geographic and sectoral terms.

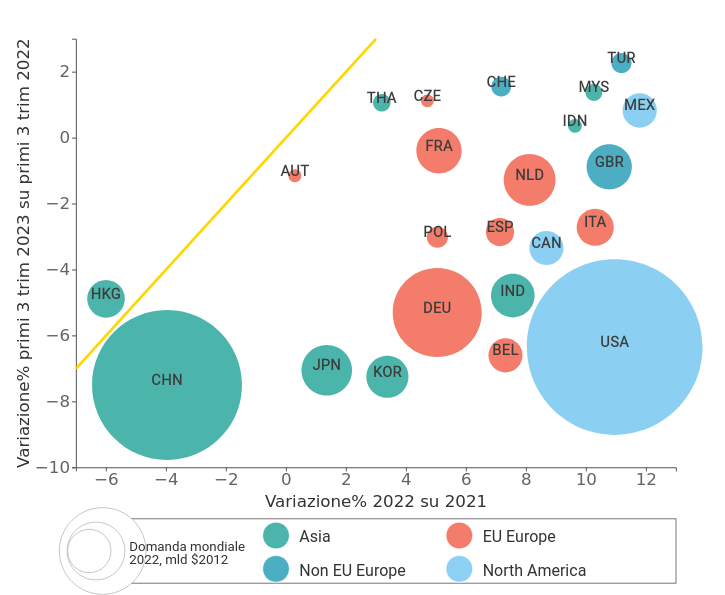

World demand for goods: the geographic profile of the slowdown

The bubble map below shows the world's major economies, positioning them on the basis of the rates of change in goods imports at constant prices recorded in 2022 (X-axis) and the first nine months of 2023 (Y-axis). Imports are measured at constant prices in order to return a reading of real dynamics, that is, net of price changes. The bisector is plotted in yellow, which allows us to highlight countries (positioned above it) that have accelerating rates of change in their merchandise imports in the first nine months of 2023 compared to the 2022 dynamics.

It is evident from the proposed map that essentially all geographies lie below the bisector, signaling how the slowdown phase is a common factor for all the world's major importers.

Fig.1 – Map of the world's largest importers at constant prices

Source: ExportPlanning

- North America: is discernible the sharp slowdown that is affecting in real terms the imports of Canada and the United States, which after dynamic growth in 2022, are in negative territory in the new year. Bucking the trend is Mexico, the only country in the area that is proving more resilient to the current economic situation, partly due to the country's increasingly significant role in the reshoring processes taking place in the North American area;

- Asia: he economies of the Asian continent appear to be "split" into two large clusters. The first falls into all those countries that are adding to already weak growth in 2022 a further reduction in imports in 2023; this cluster includes first and foremost China, followed by the markets of Japan, South Korea and Hong Kong. The second cluster, on the other hand, is headed by the resilient and still holding economies of ASEAN, such as Malaysia, Thailand and Indonesia. In the middle of the two groups we find India, also slowing down, but with smaller reductions than the first group and positive 2022 dynamics;

- Europe: slowdown also evident for all EU member countries, with Germany and Belgium experiencing the largest declines; other member states, including Italy itself, are more resilient. Broadening our gaze eastward, the performance of the Turkish market appears to be bucking the trend.

World demand for goods: the sectoral profile of the slowdown

Equally informative is the bubble map of world imports by industry, shown here.

Fig.2 – Map of world demand by industry at constant prices

By hovering the mouse over the circle identifying an industry, a table can be displayed that summarizes the annual and six-month change data for the selected industry

Source: ExportPlanning - Datamart World Conjuncture

Again, the slowdown affects almost all industries across the board, with few exceptions:

- The automotive industry, both transportation equipment (F3) and components (D3), emerges as the only sector bucking the trend, sustaining the current economic phase of world trade, after the sharp downturns and slow recovery experienced in the post-pandemic period. Driving the growth is the increasing relevance of electric and new mobility. Also attributable to these dynamics is the good resilience of Electrical Engineering (D4), with strong growth in electric motors for motor vehicles;

- Still holding up appears to be the Industrial Investment Goods (Machinery, Equipment and Tools for Industry - F5, F4 and F2) industry. However, as recounted in the article Machinery and equipment: economic analysis that of capital goods is a sector in which the discrepancy existing between order collection and delivery is among the highest, affecting, therefore, the correct interpretation of results. Documented tightness may in fact reflect a lag between investment decisions and delivery of purchased goods. If this is the case, the economic data tend to document the persistence of a growth phase due to earlier investment decisions, which may be running out;

- The downsizing in the level of economic activity is also documented by prudent purchasing policies by businesses, documented by the slowdown in imports of all intermediate goods (B);

- Among consumer goods, the home system and the fashion system accuse the largest contractions in quantity in recent months. However, if in the former case it is a strong "structural" downsizing of demand after the "boom" of the pandemic two-year period, in the latter case the effects on consumption patterns induced by rising selling prices and the reduction of economic availability, eroded by inflation, are discernible;

- Also slowing down is the electronics industry, both finished goods (F1) and components (D1), as documented in the article The sharp decline in world exports of ICT and Service Equipment. It reflects both a process of "normalization" of demand for the segment, after a two-year period of intense growth, and the gradual decoupling of the U.S. from China for the sector, in the face of partial substitution with other suppliers.

Conclusions

The relative dispersion, both geographic and sectoral, of economic dynamics suggests that exporting firms should carefully analyze the potential expressed by different foreign markets. Information is, now more than ever, an important strategic lever for directing their efforts toward the most promising markets.

You may be interested in:

US Trade Deficit Put to the Test by Tariffs: Evidence from First-Half 2026 Data

Published by Marzia Moccia. .

Slowdown Conjuncture United States of America Uncertainty Trade war Foreign market analysisAmid uncertainty that has now become the new normal, international geopolitical tensions, and the reshaping of the rules governing global trade, the United States undoubtedly remains a key focus of }... [ Read all ]

Plastics processing machinery: what are the main markets and how is the competitive landscape evolving?

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Industries International marketingPlastic processing machinery represents one of the most important technological pillars of modern manufacturing supply chains. Through processes such as injection moulding, extrusion, blow moulding }... [ Read all ]

Global Economic Outlook: International Trade Results for April 2026

Published by Marzia Moccia. .

Conjuncture Industries Uncertainty Global economic trendsThe data for April 2026 document the continuation of an expansionary phase in international trade, albeit with significant differences at the product level. [ Read all ]