How to identify the product sectors with the highest potential in a market: the Mercosur agreement and the case of Brazil

Published by Veronica Campostrini. .

Planning Free trade agreements Internationalisation Made in Italy Foreign market analysisAfter more than twenty years of negotiations, marked by periods of stalemate and subsequent reopenings, on December 6, 2024 the European Union and the Mercosur countries reached a political agreement to conclude the EU–Mercosur Partnership Agreement (EMPA), one of the most comprehensive trade agreements ever negotiated by the EU.

On September 3, 2025 the European Commission submitted the official proposals for the signing and conclusion of the agreement to the Council, formally launching the institutional process. The European Parliament subsequently suspended the approval procedure, opening a political debate particularly focused on environmental safeguards and the protection of sensitive agricultural sectors. In recent days, however, the European Union has decided to proceed with a provisional adoption of the agreement, pending full ratification.

The agreement involves a market of over 780 million consumers and fits into the European strategy of geographical diversification of trade partners, within an international context marked by growing geopolitical tensions and a renewed wave of protectionist industrial policies.

Within Mercosur, Brazil represents the economic center of gravity of the area: accounting for more than 70% of the bloc’s GDP, it is the ninth-largest economy in the world in nominal terms and the main destination market for European exports to Latin America.

The framework of the trade agreement

The EMPA introduces a gradual liberalization of trade between the parties, with a particularly significant impact on European industrial goods. In particular, the agreement provides for:

- the gradual elimination of tariffs on 90% of imports of European industrial goods within a 10-year horizon;

- the liberalization of 93% of agricultural tariff lines, according to differentiated timelines;

- the reciprocal opening of public procurement markets;

- measures aimed at reducing non-tariff barriers and increasing regulatory convergence;

- the strengthening of protections in the field of intellectual property and geographical indications.

For Brazil, characterized by an average level of manufacturing tariffs above 10% and significantly higher rates in consumer goods and automotive sectors, the progressive reduction of tariffs represents a structural change in market access conditions. Looking ahead, the agreement will reshape the competitive landscape in favor of European exporters, reducing one of the main price disadvantages that has existed so far.

Opportunity frontiers for Italy

Brazil represents a strategically important market for three main reasons:

- its significant demographic size (over 210 million inhabitants);

- its complex industrial structure, with a structural need for technological upgrading;

- its role as a production and logistics hub for the entire Latin American region.

In 2025 trade between Italy and Brazil exceeded €10 billion, with Italian exports specialized in capital goods, machinery, pharmaceuticals and industrial components.

In this context, sectoral analysis plays a decisive role: identifying the sectors with the greatest potential is not merely a descriptive exercise, but an operational tool for directing commercial strategies and investment decisions in a targeted way, in view of the progressive liberalization envisaged by the agreement.

Identifying high-potential sectors: the method

To replicate the approach applied to the India case in the previous article “How to identify the product sectors with the highest potential in a market: the case of India”, the identification of priority sectors is carried out through the construction of a sectoral opportunity matrix, based on three key indicators:

- the current level of Italian exports to Brazil;

- the change in Italy’s market share over the past three years;

- the expected dynamics of Brazilian demand over the next four years.

The indicators are normalized on a 0–100 scale in order to ensure comparability across sectors with different structural characteristics. The weighted combination of the three factors generates a synthetic potential score, which makes it possible to rank sectors according to their development prospects.

The analysis is complemented by integrating the tariff framework: both the currently applied tariff level and the one expected under the scenario of progressive tariff reductions envisaged by the EMPA.

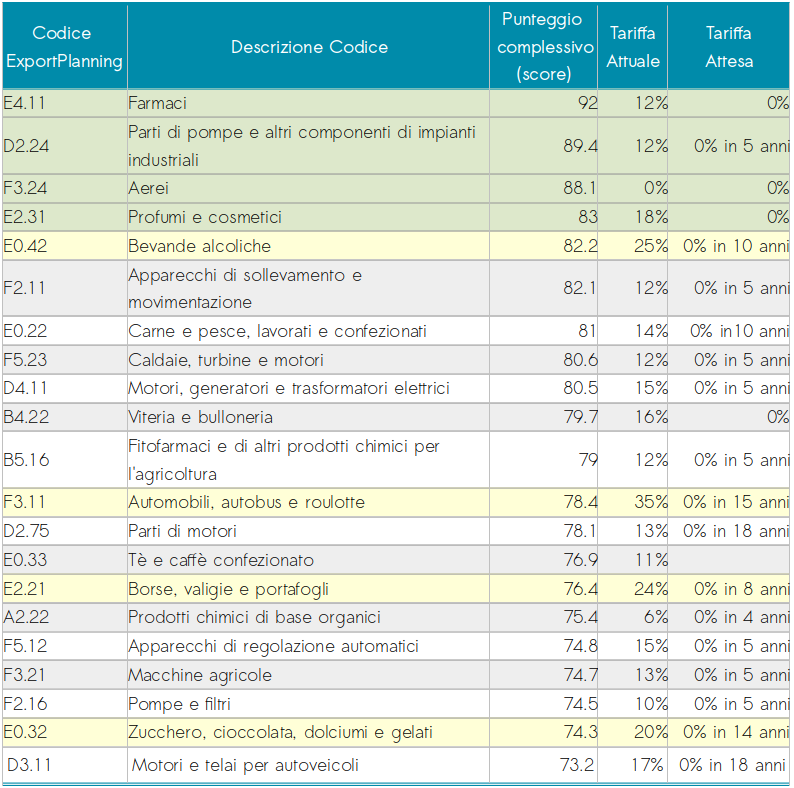

Tab.1 - Potential score and tariff framework*

Source: ExportPlanning

Among the sectors with high growth potential in the Brazilian market are, first of all, those industries in which the Italian production system has already consolidated a significant competitive position in recent years. In particular, this category includes health-related goods, with pharmaceuticals at the top of the ranking, as well as the group of chemical intermediates and agricultural products, which includes basic organic chemicals and crop protection products.

Alongside the health-chemicals supply chain, the industrial machinery and capital goods sector stands out strongly, occupying numerous positions at the top of the ranking: pump parts and industrial plant components, lifting and handling equipment, boilers and turbines, electric motors and transformers, automatic control instruments and pumps. This is fully consistent with Brazil’s production structure, a large manufacturing economy and industrial hub for Latin America characterized by a structural need for technological upgrading.

Another relevant area is represented by the automotive supply chain, which includes passenger cars, engine parts, and engines/chassis for motor vehicles. In this case, in addition to the high score, the still-existing tariff structure is particularly significant — with duties reaching very high levels for finished vehicles — highlighting a historically protected market that is nonetheless strategic for global value chains.

Alongside already competitive sectors, particular importance should be attributed to those segments for which trade liberalization may represent a real turning point, thanks to the reduction of currently high tariff barriers. This group includes several emblematic Made in Italy products, such as alcoholic beverages, the confectionery and packaged food sector, as well as the fashion-and-personal goods system (handbags, luggage, perfumes and cosmetics), all characterized by average duties ranging between 18% and 25%.

In these sectors, growth potential is partly underestimated by the model, as current market access conditions have so far limited the full expression of Italian competitiveness. The progressive reduction of tariffs could therefore significantly amplify development prospects, especially in premium segments and in the country’s main urban areas.

Are you interested in receiving a selection of the most relevant foreign trade news of the week? Subscribe for free to the World Business Newsletter!

A Brazil with a dual trajectory

The integrated reading of the potential score and the tariff framework provides a nuanced picture of the Brazilian market: on the one hand, an industrial market already mature and receptive to Italian intermediate and capital goods, where the agreement consolidates growth trajectories that are already underway; on the other hand, a consumer market that is still relatively protected, but with wide margins for expansion should liberalization be fully implemented.

For Italian companies, the challenge is not only to capture existing demand, but also to position themselves in a timely manner in view of the new competitive scenario. If definitively ratified, the EU–Mercosur agreement could represent a strategic turning point in redefining Italy’s presence in Latin America.

Within this framework, sectoral analysis becomes an essential tool for transforming a trade agreement into a concrete competitive advantage.

You may be interested in:

Decision-Making Under Uncertainty: The Strategic Value of External Data

Published by Marzia Moccia. .

Planning Internationalisation International marketing Internationalisation toolsA company’s performance largely depends on the quality of the decisions it makes, and the quality of decisions depends on the information available. Effective decisions allow the company to move for}... [ Read all ]

From Sales Attempts to Strategic Planning: The Role of Geopolitics in Shaping Firms’ Internationalization Decisions

Published by Marzia Moccia. .

Planning Conjuncture Foreign markets Uncertainty International marketing International marketingRecent developments have made it increasingly clear that the international environment is characterized by a growing and persistent level of uncertainty and geopolitical instability, directly affecti}... [ Read all ]

Market Diversification Objective: The EU–Mercosur Trade Agreement

Published by Marzia Moccia. .

Free trade agreements Europe Latin America Market AccessibilityAfter more than twenty years of negotiations, suspensions, reopenings, and periods of intense political tension, on December 6, 2024, the European Union and Mercosur reached a historic agreement aimed}... [ Read all ]