Warning signs from Argentine Peso?

After months of stability, the currency is weakening again.

Published by Alba Di Rosa. .

Exchange rate Emerging markets Argentine peso Economic policy Central banks IMF Exchange ratesThe Argentine Peso, a historically weak currency, has been one of the main victims of the emerging-market capital flight that occurred last year. Excluding the extreme case of the Venezuelan Bolivar, which suffered a depreciation against the dollar amounting to more than one million percentage points in 2018, Argentine Peso was the hardest hit, losing almost 100% of its value against the greenback.

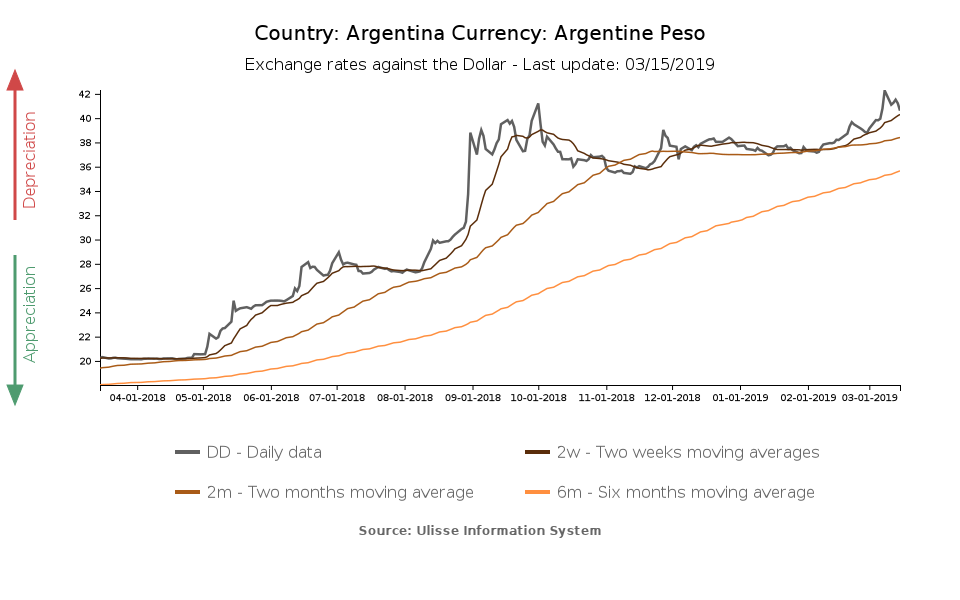

After the height of the crisis in August, when the Peso lost 40% of its value against the dollar, in October the currency took the path of stabilization. As you can see in the chart below, since February the Peso entered a new phase of weakening, which led the currency to lose more than 9% of its value against the dollar.

The impact of monetary and fiscal policy

Loans granted by the International Monetary Fund in the framework of the Stand-By Arrangement signed in June had a major impact on currency stabilization, together with the progressive

implementation of the agreed reforms. Up until now, the IMF has provided Argentina with more than 28 billion dollars in 3 tranches.

As regards reforms, on the monetary policy side the Banco Central de la Republica Argentina (BCRA) has adopted a more restrictive stance, which aims to support the currency and keep

inflation under control. One of its tools is the issuance of LELIQ, securities denominated in pesos.

On the fiscal policy side, the budget for 2019 has been approved in November: it included public spending cuts previously agreed with the Fund to obtain the loan.

This has certainly been an unpopular move for President Macri, but at least it helped restore some market confidence in Argentina.

February 2019: a new phase of weakening

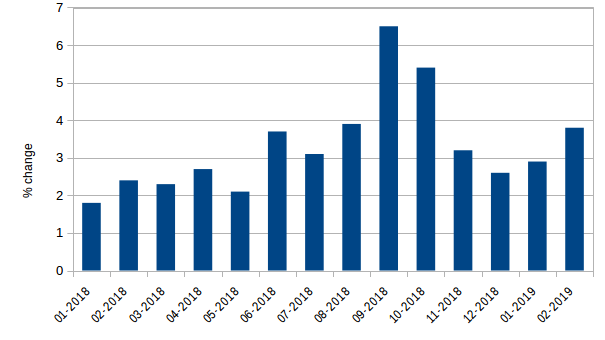

The root of this renewed weakness on the exchange rate front is the difficulty on the part of monetary policy authorities to significantly reduce inflation. After some weak progress in the last months of 2018, in the first two months of this year inflation accelerated again, as you can see in the graph below. In February, prices increased by 3.8% compared to the previous month.

Argentina, monthly inflation rate

(January 2018-February 2019)

Source: StudiaBo elaborations on Banco Central de la Republica Argentina data.

The immediate response of the central bank was a rise in monetary policy reference rate, now back above 60%. However, such a restrictive approach puts the economy at risk: Argentina’s GDP has already suffered a 4.2% contraction in Q2-2018 (year-on-year) and 3.5% decrease in Q3. This approach jeopardizes the re-election of President Macri, as well, since October presidential elections are approaching.

Risk elements

In addition to inflation, the new Peso crisis also seems to reflect widespread concerns about the possibility of a slowdown in global growth,

and the consequent increase in risk aversion.

A further cause for concern has emerged in recent weeks, i.e. the high amount of LELIQ debt issued by the central bank: more than a trillion pesos in mid-March

(more than 20 billion dollars). Given the current high interest rates, this stabilization tool could turn out to be a source of instability in the medium term,

exacerbating Argentina’s critical situation.

You may be interested in:

IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsPer il 2026 il Fondo ha rivisto lievemente al ribasso le stime di crescita del PIL mondiale, ora previsto al +3% [ Read all ]

January 2026: the latest data on global trade in goods

Published by Marzia Moccia. .

Slowdown Exchange rate Conjuncture Dollar Euro Foreign markets Uncertainty Global economic trendsThe availability in the ExportPlanning Information System of global trade data for January makes it possible to update the short-term outlook on the most recent dynamics of world trade in goods, wit}... [ Read all ]

B-READY 2025: the World Bank’s new compass for economic development

Published by Veronica Campostrini. .

Macroeconomic analysis Foreign markets Economic policy Central banks Foreign market analysisWith the publication of the Business Ready 2025 report, the World Bank introduces the new B-READY (Business Ready) index, intended to permanently replace the previous Doing Business, which was suspend}... [ Read all ]