Current scenario of European exports in the first quarter of 2024

The EU's exports show the first signs of recovery, but still remain in negative territory

Published by Simone Zambelli. .

Europe Conjuncture Global economic trendsThe availability of ExportPlanning pre-estimates for the 1st quarter 2024 of the foreign trade data of EU countries - accessible through the EU countries datamart- allows us to outline the European economic situation in the first months of 2024.

As is known, 2023 was a difficult year for international trade, due to a combination of factors that contributed to creating an uncertain and challenging economic and trade environment for businesses and governments around the world. 2024 therefore promises to be a year full of hope for a significant recovery.

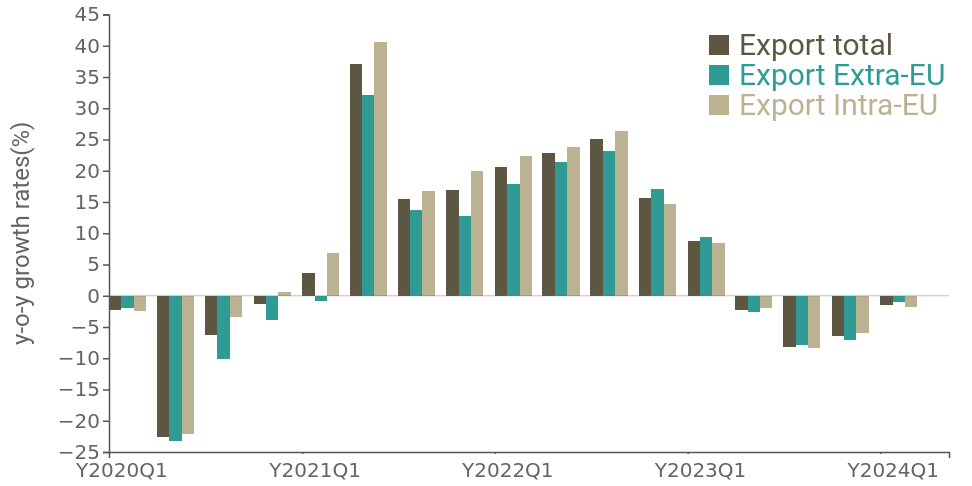

The following graph shows the trend changes in the Union's exports in euro, dividing them between intra-EU and extra-EU flows.

In the graph shown it is clear that 2023 was a downward year, culminating in the third quarter, in which total EU exports recorded a -8% trend in euro values. The fourth quarter is also strongly negative (-6%), while from the first months of 2024 it seems that the trend is reversing, with EU exports which, although in negative territory, settle at - 1.4% trend in euro values.

Despite the positive signals, Europe is still in difficulty compared to its main global competitors. The analysis of the PMI (Purchasing Manager Index) tells us that, while China and the United States have already exceeded the critical threshold of 50 (which discriminates between recession and expansion) since January, the EU is unable to exceed 46: this suggests that the recovery is still slow for the Old Continent.

Focus on Countries

In recent months the dynamics of EU exports have been characterized by strong heterogeneity.

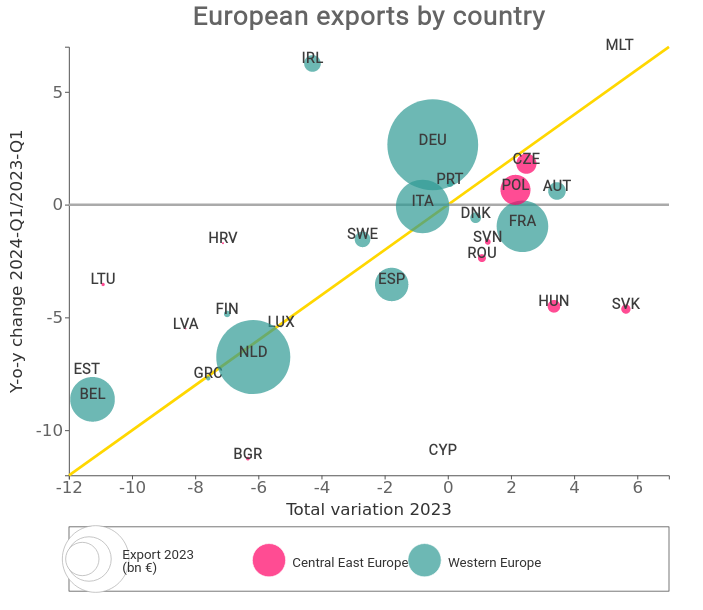

The following map positions countries based on the annual rate of change of 2023 (X-axis) and the rate of change of the first quarter of 2024 on the corresponding quarter of 2023 (Y-axis); the size of each ball is proportional to the value of exports in 2023.

During 2023, it is above all the countries of Central and Eastern Europe that have held up the most (with the exception of the Baltic Republics and Bulgaria and Croatia), while for Western Europe only France, Denmark and Austria recorded changes at the end of the year positive in euro values, however less than 3%. Italy closes 2023 with -0.7%, similar to Germany with -0.5%.

In the first quarter of 2024 there are many countries improving compared to the 2023 average, i.e. those that are positioned above the bisector; however, there are still few countries that have positive trend changes. Among the main EU exporters we note Italy (+0.5% in euro values), Germany (+2.4%), the Czech Republic (+1.4%), Poland (+0.8%) and Austria (+ 0.8%).

Focus on Industries

Let us now shift our attention to the manufacturing specialization industry level.

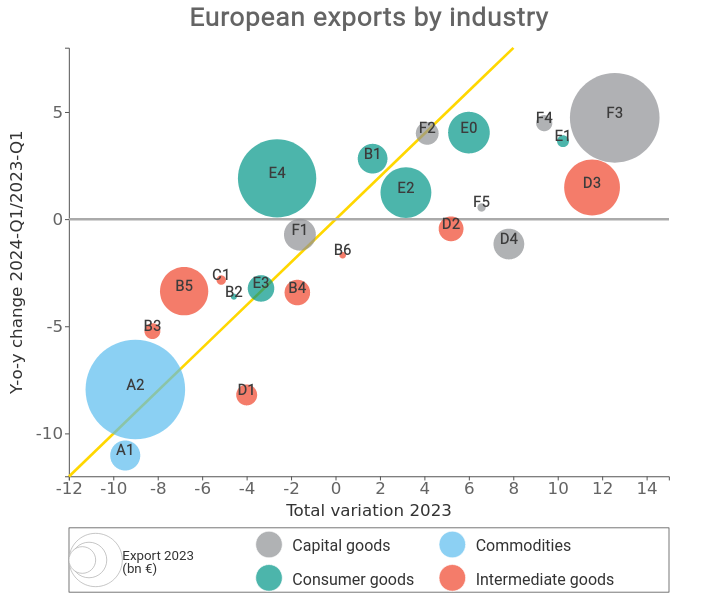

In the following graph, the different industries are positioned on the basis of the annual rate of change recorded in 2023 (X axis) and that of the first quarter of 2024 compared to the first quarter of 2023. Furthermore, the size of the balls is proportional to EU exports in 2023.

At a sectoral level we can see that it is above all consumer goods that have recorded the greatest increases (albeit limited) in the first quarter of this year: +4.4% for packaged food and beverage (E0) and +1.8% for unpackaged food (B1); fashion products (E2) recorded a +1.7%, while health products and tools (E4) recorded a +1.9%; the only exception is the still negative performance of the household products (E3).

Investment goods also showed resilience in 2023 and are growing trend in the first quarter of 2024, led by automotive (F3) with +15.6 % trend, which also drags up the sector of the related components (D3).

On the other hand, intermediate goods and, even more downwards, natural and industrial raw materials recorded mostly negative changes (A1 and A2), also due to the general drop in the prices of the main commodities that has been underway for several months.

Conclusions

2023 represented a period of significant challenges for international trade, characterized by a number of factors, including trade and geopolitical tensions and economic instability.

In the first quarter of 2024, promising signs of a possible recovery emerged, helping to create a more favorable climate for global trade.

Although Europe still appears to be slightly behind its main global competitors, these good signs offer hope for a recovery during the year.

You may be interested in:

Footwear: how are the manufacturing Countries performing in the first half of 2026?

Published by Mauro Badanelli. .

Conjuncture Industries Foreign markets International marketingAfter analyzing the dynamics of global trade in footwear machinery in a previous article, attention now shifts to the finished product, in order to examine the most recent performance of the main foot}... [ Read all ]

Export 2026-2029: ExportPlanning updates its forecast scenario

Published by Marzia Moccia. .

Conjuncture Export markets Uncertainty IMF Global economic trendsFor exporting companies, the ability to promptly interpret the evolution of international markets is now a key competitive factor. In a global context characterized by rapid changes and growing unce}... [ Read all ]

Footwear Machinery: the map of Growing and Slowing markets in Q2 2026

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Foreign markets International marketingFor exporting companies, the international context is changing increasingly rapidly. Relying on consolidated year-end data often means arriving too late. Having indicators updated to the second quarte}... [ Read all ]