IMF WEO April 2026: the global economy faces new tests

Published by Alba Di Rosa. .

Macroeconomic analysis Conjuncture Uncertainty Trade war Global economic trendsOn April 14, the International Monetary Fund released the latest edition of the World Economic Outlook (WEO), a key study that compiles analyses and projections on the global economy in the short and medium term. In the document, the Fund reviewed the evolution of the global economy over the past year and attempted to outline its prospects, within the particularly uncertain context we are currently experiencing. Let's take a closer look at the report’s key messages.

The global economy in 2025: resilience in the face of challenges

As we all recall, 2025 was a year fraught with challenges on the international stage. The obstacles arising from increased trade barriers and high levels of uncertainty were significant; however, these challenges were partly offset by the benefits of investments in the technology sector, favorable financial conditions, and the support provided by fiscal and monetary policies. Overall, despite major disruptions to trade and the persistent climate of uncertainty, last year ended on a positive note in terms of global economic growth.

In the April 2026 edition of the WEO, global economic growth for last year was revised to +3.4%, which is 0.1 percentage points higher than the January estimates (and 0.2 percentage points higher than those from last October).

Global trade also remained robust in 2025, as documented on several occasions in our magazine.

This performance was driven primarily by the expansion of exports in the technology sector, which offset the slowdown in trade for other product categories.

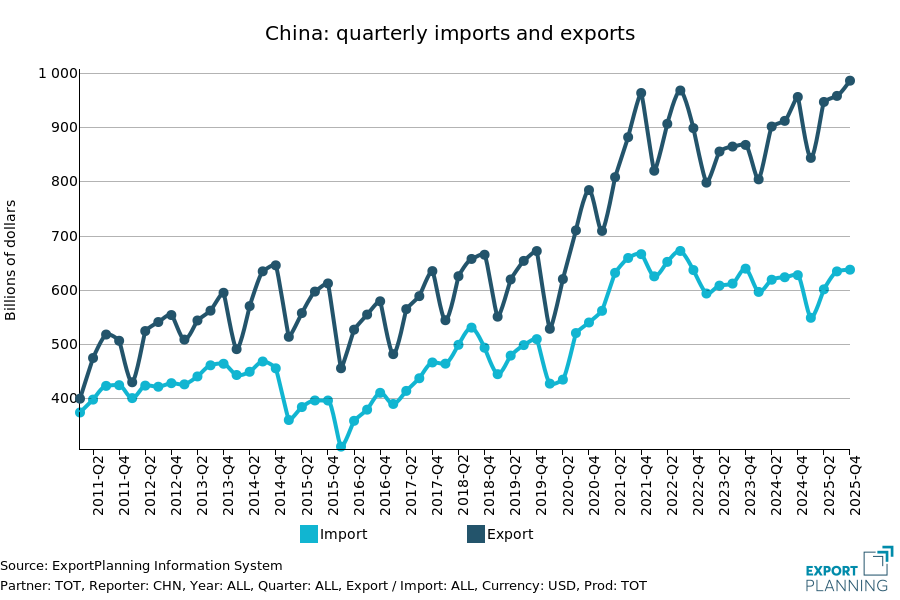

Furthermore, the reorganization of global supply chains and trade relations continued. US imports from China fell significantly (-29% in dollar terms; see the US Quarterly Trade Database); imports from Canada also declined (-6.9%). These declines were offset by increased imports from Taiwan (+72.7%), Vietnam (+41.2%), and, to a lesser extent, Mexico (+5.7%).

For their part, Chinese exports have gradually shifted from the United States toward other Asian economies and, temporarily, toward Europe, leading China to reach a new high in terms of trade surplus.

New source of tension

Despite the presence of some downside risks, prior to the outbreak of the US-Israel conflict with Iran, the Fund projected that the current moderate momentum would continue through 2026 – momentum that was then abruptly halted by the outbreak of the conflict in the Middle East, with immediate disruptions caused by the closure of the Strait of Hormuz and attacks on production facilities.

The conflict is therefore representing a clear risk factor, due to its impact on multiple fronts: primarily on commodity markets, but also on inflation expectations and financial conditions. The specter of the energy crisis thus takes center stage should hostilities continue.

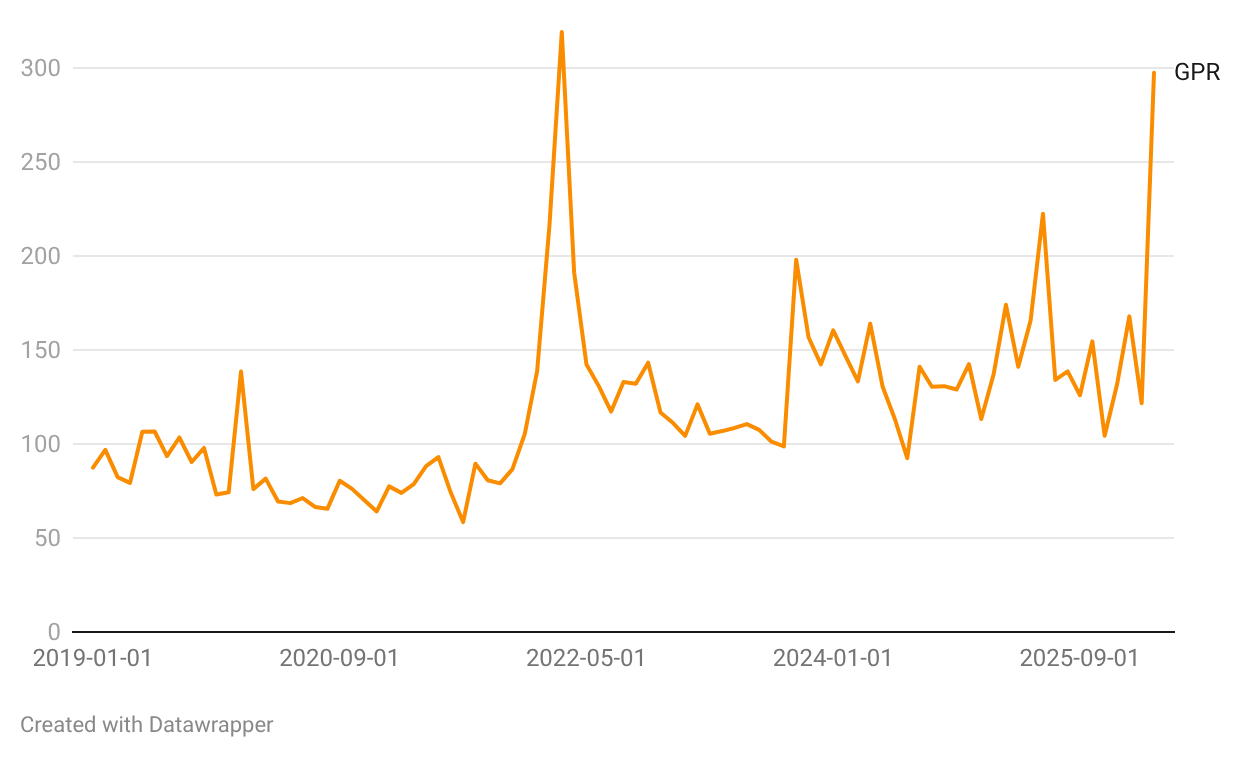

The magnitude of the current shock is measured, for example, by the Geopolitical Risk Index – an indicator developed by Dario Caldara and Matteo Iacoviello – which in March returned to levels close to those seen at the start of 2022, when the Russia-Ukraine conflict began.

Geopolitical Risk Index – up to March 2026

Source: StudiaBo elaborations on www.matteoiacoviello.com/gpr.htm data

Forecast scenario

In the context described, formulating macroeconomic forecasts is therefore particularly complex. The Fund has outlined the assumptions on which its reference forecast was formulated – namely, that the war will be of limited duration, intensity, and scope, such that the disruptions will subside by mid-2026 (in line with commodity futures prices as of March 10). The conflict is therefore expected to last a few more weeks, followed by the start of a gradual recovery, which could allow the region’s production and exports to return to normal by mid-year.

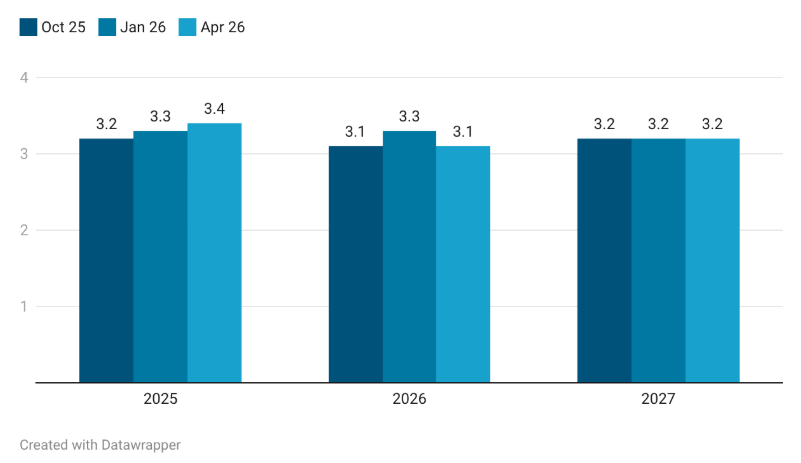

Based on these assumptions, global growth is projected to reach +3.1% in 2026 and +3.2% in 2027: we are therefore talking about a downward revision of 0.2 percentage points for 2026 and an unchanged estimate for 2027, compared to the figures released in last January’s WEO Update.

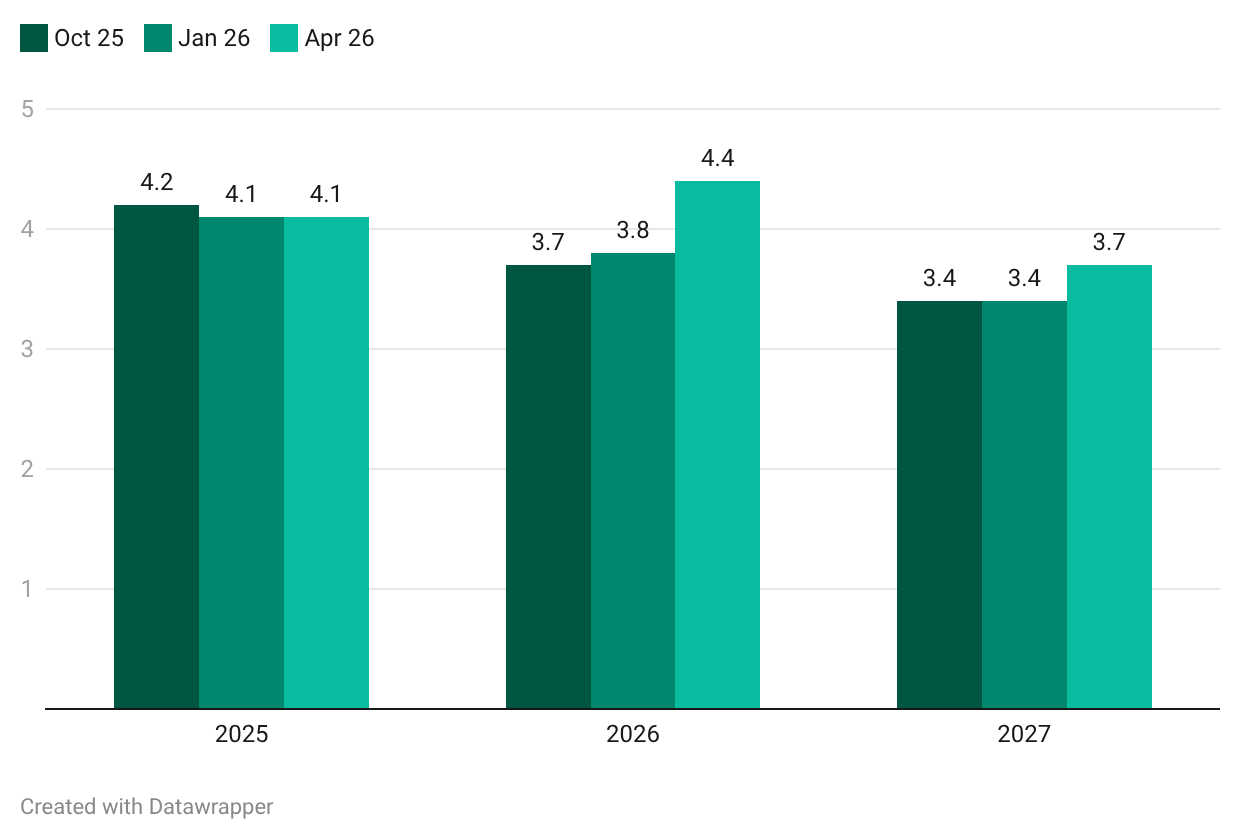

More pronounced, however, is the upward revision for global inflation, now projected at +4.4% for 2026 and +3.7% for 2027; compared to last January’s figures, this represents an increase of 0.6 percentage points for 2026 and 0.3 percentage points for 2027. This marks a clear departure from the global trend toward disinflation observed in recent years.

Global GDP outlook: a comparison of the latest WEO editions

% change

Global inflation outlook: a comparison of the latest WEO editions

% change

Source: StudiaBo elaborations on IMF data

Although the downward revisions to growth appear relatively modest at the global level, the impact on regions affected by conflict and, more broadly, on the most vulnerable economies, is much more pronounced. The downward revision of growth in emerging markets and developing economies amounts to 0.3 percentage points for 2026, compared to the figures in the January WEO, while forecasts for advanced economies remain largely unchanged.

Another point to note is the wide range of possibilities that are emerging: if, in fact, the conditions for a rapid end to the conflict highlighted by the Fund do not materialize, the outlook could deteriorate significantly. In the so-called “severe scenario” – that is, a scenario in which turbulence in energy markets persists into next year, along with a divergence in inflation expectations and a tightening of financial conditions – the global economy would risk, according to IMF estimates, entering a recession, with growth around 2% for the current and next year, and overall global inflation close to 6%.

Against this complex backdrop, the institution has therefore clearly emphasized its support for the solid principles of economic and financial cooperation and integration – principles that are all the more necessary at this historic moment to preserve global prosperity.

You may be interested in:

IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsPer il 2026 il Fondo ha rivisto lievemente al ribasso le stime di crescita del PIL mondiale, ora previsto al +3% [ Read all ]

US Trade Deficit Put to the Test by Tariffs: Evidence from First-Half 2026 Data

Published by Marzia Moccia. .

Slowdown Conjuncture United States of America Uncertainty Trade war Foreign market analysisAmid uncertainty that has now become the new normal, international geopolitical tensions, and the reshaping of the rules governing global trade, the United States undoubtedly remains a key focus of }... [ Read all ]

Plastics processing machinery: what are the main markets and how is the competitive landscape evolving?

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Industries International marketingPlastic processing machinery represents one of the most important technological pillars of modern manufacturing supply chains. Through processes such as injection moulding, extrusion, blow moulding }... [ Read all ]