Woodworking machinery: global trade slows down

Published by Mauro Badanelli. .

Internationalisation Industrial equipment Conjuncture Foreign markets International marketingThe production of technologies for woodworking represents a strategic sector of Made in Italy, closely linked to the furniture and furnishings supply chain. In this context, Italy stands out internationally for the breadth and specialization of its offering: from machines for the primary processing of raw wood to advanced systems for finishing and panel processing.

Within this supply chain, the article will focus in particular on stationary machines for woodworking1.

Stationary woodworking machines refer to fixed equipment designed for precise, repetitive and professional processing of wood materials. Unlike portable tools, these machines are permanently installed and allow for greater accuracy, safety, and productivity. They are essential equipment both in the furniture industry and in craftsmanship, as they enable high-quality results while reducing processing time.

The state of global trade in woodworking machinery

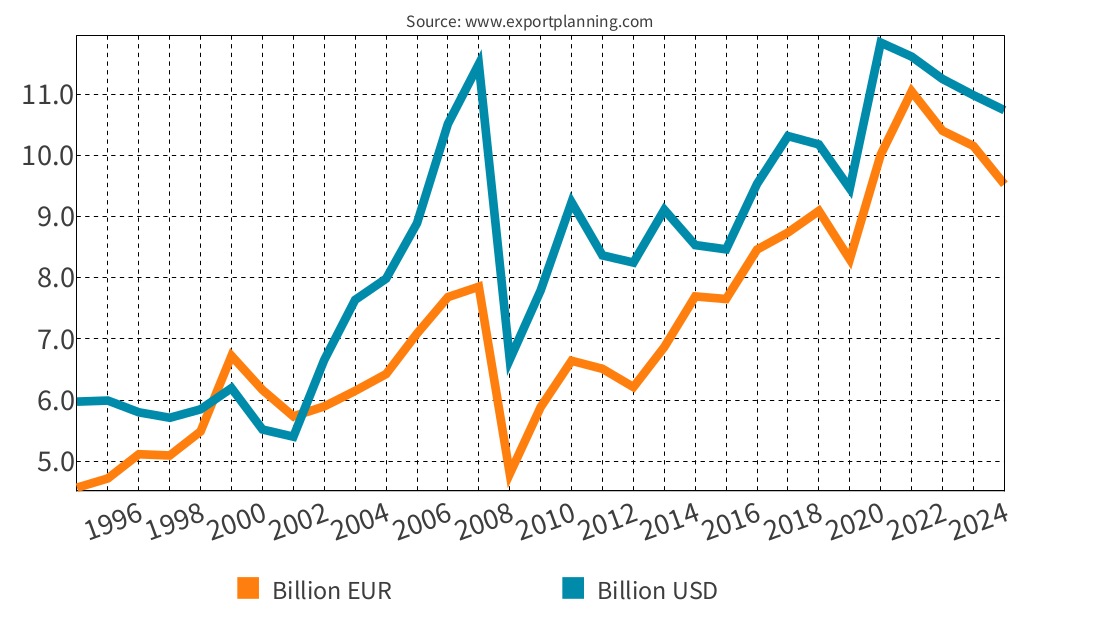

After reaching a historic peak of over 11.5 billion dollars in 2021, in 2025 the value of global trade in woodworking machinery stood at 10.7 billion dollars, corresponding to 9.5 billion euros.

Also due to the decline in interest in upgrading domestic spaces and furnishings following the boom recorded during the pandemic period, recent years have shown a relatively weak phase for global trade in the sector, confirming a downturn in trade already begun in 2023.

Over the period 2009–2025, the average annual growth rate was rather limited (+1.1% in euros).

Fig.1 – Woodworking machines - Global trade by value

The main markets for woodworking machinery

Analysis of international trade flows helps outline the geography of production in the wood-furniture supply chain. The United States remains, also in 2025, the main market for manufacturers of wood machinery. The value of imports reached 1,554 million euros, accounting for a 16.5% share of global imports.

Demand for foreign machinery from other major markets is significantly lower. In 2025, the second-largest global market, Germany, imported machinery worth 622 million euros, equal to a 6.6% share of global imports in the sector. This is followed by Vietnam, Canada and France, whose imports in 2025 were equal to or below 400 million euros.

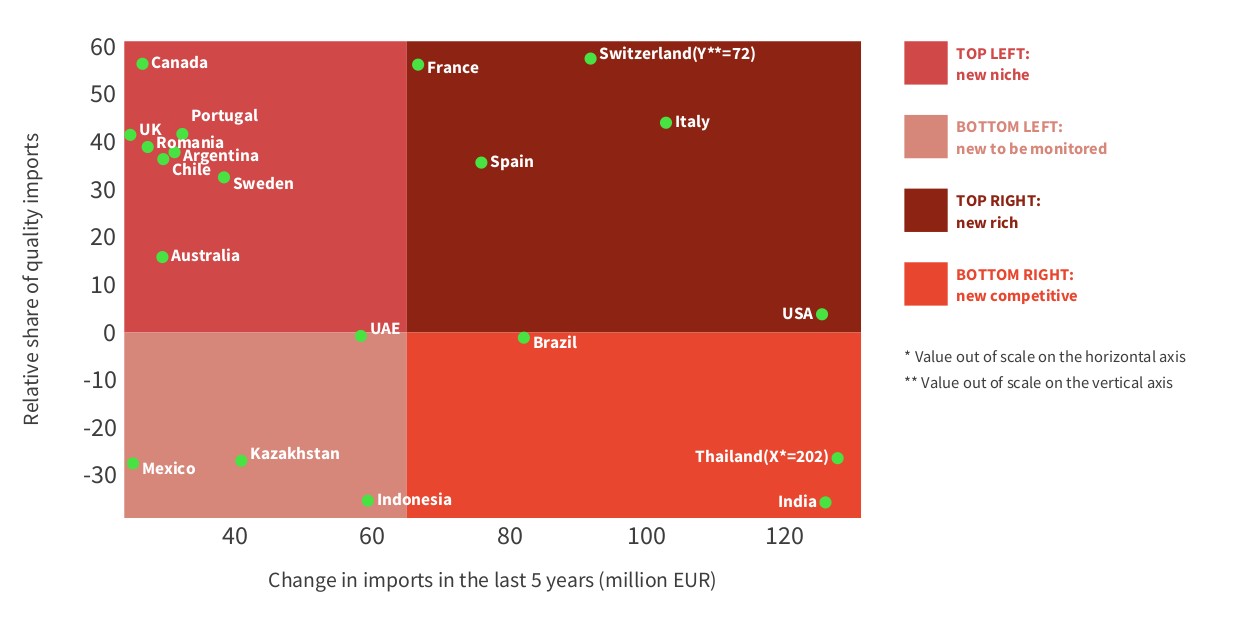

The ExportPlanning information system also enables analysis of the varying propensity of different markets to pay a premium price for the quality of imported products. It can thus be observed that, like Vietnam, other markets over the 2020–2025 period have experienced a strong increase in imports of low-end machinery (Thailand, India, Brazil and the United States). Conversely, over the same period, the increase in imports in Italy and Switzerland concerned higher price segments.

Fig. 2 - Woodworking machinery - Analysis of premium price in the most dynamic markets

(2020–2025 period)

Source: ExportPlanning elaborations - Reporting Tool

Are you interested in receiving a selection of the most relevant weekly foreign trade news? Subscribe for free to the World Business Newsletter!

The competitive landscape and Italy’s positioning

The international competitive arena sees China, Germany and Italy in the top 3 among the largest global suppliers of technology. In particular, the first two countries hold a significant market share. Chinese exports reached 2,486 million euros in 2025, equal to 24.3% of global exports. Germany, on the other hand, exported woodworking machinery worth 2,262 million euros (22.1% market share). However, export trends in the two countries have followed markedly different dynamics. In 2009, Chinese machinery accounted for only 6.8% of global trade, while Germany held a 28.6% share.

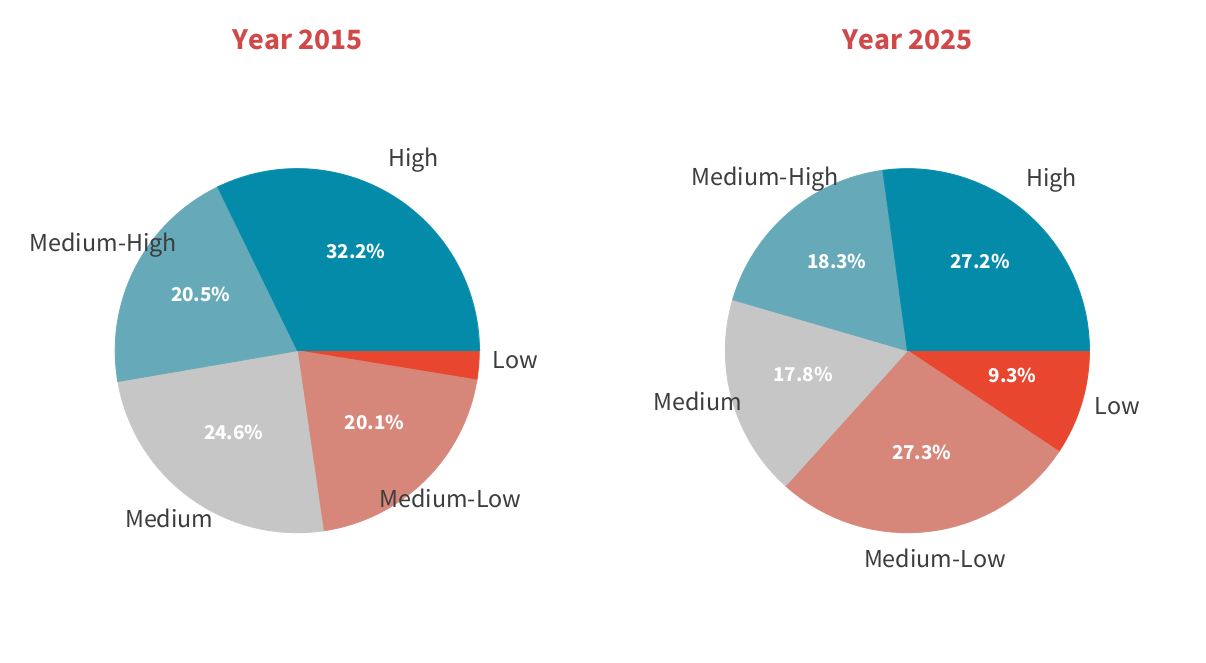

The growth of Chinese exports in the global context has also impacted the distribution of trade by price segment. Fig. 3 shows the redistribution of exports between 2009 and 2025 in favor of the medium-low and low price segments.

Fig. 3 - Woodworking machinery - Distribution of international trade by price level

Source: ExportPlanning elaborations - Reporting Tool

Within this competitive landscape, Italy ranks third, having exported 1,374 million euros in 2025, corresponding to 13.4% of global exports. Over the years, Italy has also experienced a decline in its market share, which stood at 17.5% in 2008. Italian exports in the sector are mainly directed toward the United States, with a value reaching 177 million euros in 2025, and toward EU countries (Germany, France, Poland and Spain).

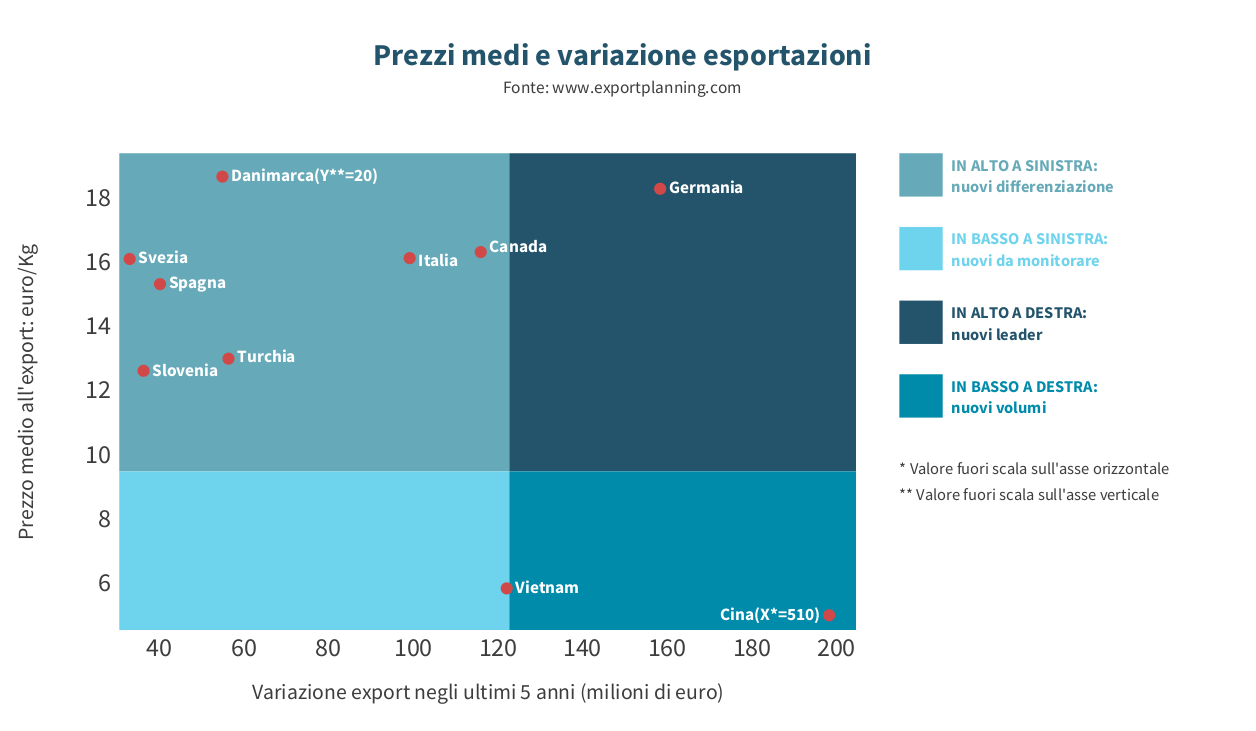

Analysis of competitive positioning in the 2020–2025 period confirms Germany’s technological leadership, with its ability to export large volumes of high-priced machinery. Canada and Italy also position themselves in a similar market segment to Germany, with significant export flows. In the low-end segment of the competitive landscape, China dominates, exporting large quantities of machinery at significantly lower prices.

Vietnam’s exports are also moving in this direction. In 2025, Vietnamese exports reached 131 million euros and, although not yet among the leading exporters, foreign sales have grown significantly in the medium term, especially since 2022, at an average annual growth rate of 34%. The main destination market for Vietnamese exports is currently the United States, where in 2025 exported machinery reached a value of 86 million euros.

This phase of export growth in the country—still a net importer of machinery for the sector—appears to be the result of a nearshoring strategy implemented by Chinese manufacturers, as observed in other sectors of capital goods machinery in response to the US-China decoupling.

Fig. 4 - Woodworking machinery - Competitive positioning of the most dynamic exporters

(2020–2025 period)

Source: ExportPlanning elaborations - Reporting Tool

Trends in the first quarter of 2026

Thanks to the ExportPlanning information system, it is possible to compare global trade data for the sector in the first quarter of 2026, offering an up-to-date interpretation of current dynamics.

The most recent evidence confirms the persistence of a contraction phase in global demand. After declines in recent years, the January–March period recorded a further deceleration, with a drop of 10 percentage points. EU exports and Italian exports have also decreased, with the decline appearing particularly significant for Italy. While, as shown in the table, Italian export dynamics have remained broadly aligned with those of the European Union in recent years, the first months of 2026 show an initial sign of divergence, the nature and persistence of which will need to be carefully monitored in the coming months.

Tab. 1 – Woodworking machinery - Comparative dynamics

year-on-year % changes at current prices

| 2023 | 2024 | 2025 | Q1-2026 | |

| Global demand | - 6.7% | - 3.8% | - 7.1% | - 10.7% |

|---|---|---|---|---|

| EU exports | + 2.7% | - 7.8% | - 9.9% | - 2.2% |

| Italy exports | + 2.5% | - 8.1% | - 11.9% | - 8.8% |

Source: ExportPlanning information system

Conclusions

Global trade in stationary woodworking machinery is currently in a slowdown phase. Data on global demand also confirm, for the first part of 2026, the difficulties faced by exporting companies in the sector. In several markets, price competition is becoming increasingly intense, while on the supply side China’s position as a key player continues to strengthen.

This is therefore a dynamic and constantly evolving scenario that requires careful monitoring of market conditions by manufacturers operating in international markets. A timely analysis of external data, including those provided by the ExportPlanning information system, can offer companies in the supply chain an up-to-date overview of potential markets to target and of the changing competitive landscape.

1. The Harmonized System (HS) codes considered for the analysis are the following: HS846510, HS846520, HS846591, HS846592, HS846593, HS846594, HS846595, HS846596, HS846599, HS846692, HS847930. ```

You may be interested in:

Blue jeans, shifting geographies: the challenge faced by new manufacturing Countries to China and Bangladesh

Published by Mauro Badanelli. .

Fashion Export Foreign markets International marketingBlue jeans: an iconic fashion product Blue jeans are one of the iconic products of the apparel industry, with a well-established presence in markets around the world and demand spanning generat}... [ Read all ]

Dyeing machinery: innovation and sustainability at the heart of a changing supply chain

Published by Mauro Badanelli. .

Industrial equipment Export Foreign markets International marketingDenim is one of the cornerstones of the global apparel industry. Every year, billions of garments are produced and sold worldwide, fueling demand from fast fashion brands, premium manufacturers, and}... [ Read all ]

US Trade Deficit Put to the Test by Tariffs: Evidence from First-Half 2026 Data

Published by Marzia Moccia. .

Slowdown Conjuncture United States of America Uncertainty Trade war Foreign market analysisAmid uncertainty that has now become the new normal, international geopolitical tensions, and the reshaping of the rules governing global trade, the United States undoubtedly remains a key focus of }... [ Read all ]