Plastics processing machinery: what are the main markets and how is the competitive landscape evolving?

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Industries International marketingPlastic processing machinery represents one of the most important technological pillars of modern manufacturing supply chains. Through processes such as injection moulding, extrusion, blow moulding and thermoforming, these machines enable the production of a wide range of products serving strategic sectors of the global economy. From automotive components to food packaging, from medical devices to construction materials, as well as electronics and consumer goods, the quality, efficiency and technological sophistication of the machinery employed directly influence the performance of the final products. Moreover, the growing demand for lighter, more sustainable and higher-performance materials is accelerating the technological evolution of the industry, driving investments in automation, process digitalisation and the use of recycled and bio-based materials.

In this context, international trade in plastic processing machinery1 represents a significant indicator of the ability of industrial systems to innovate and respond to the evolving dynamics of global demand.

Global trade in plastic processing machinery

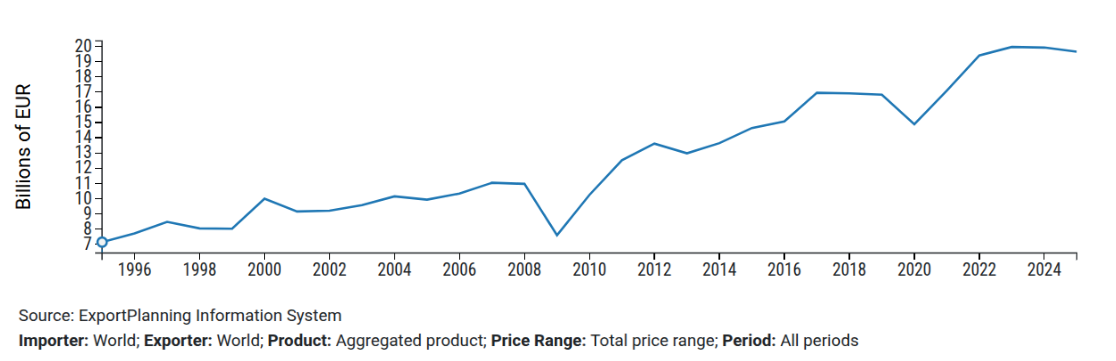

According to data available in the ExportPlanning Information System, international trade in plastic processing machinery reached 19.6 bln € in 2025, down by 1.4% at current prices compared with 2024.

Nevertheless, over the 2009–2025 period, international trade recorded an average annual growth rate of +3.5%, mainly driven by the strong expansion experienced during 2021–2022.

Fig. 1 – Global trade in plastic processing machinery

(current prices)

Source: ExportPlanning

Market conditions in the first quarter of 2026 did not show any significant change compared with the negative trend observed throughout 2025. Global trade declined by more than six percentage points compared with the same period of 2025. The overall performance was mainly affected by the contraction in Asian exports during the first months of the year. By contrast, the European Union recorded positive year-on-year growth, while Italy experienced a decline of more than ten percentage points.

Table 1 – Plastic processing machinery: comparative performance

Year-on-year percentage changes at current prices

| 2023 | 2024 | 2025 | Q1 2026 | |

| Global demand | +2.9% | -0.2% | -1.4% | -6.4% |

|---|---|---|---|---|

| EU exports | +8.5% | -5.4% | -6.3% | +1.6% |

| Italian exports | +14.2% | +2.4% | -5.5% | -11.6% |

| Asian exports | -0.2% | +7.9% | +1.8% | -10.1% |

| Chinese exports | +1.2% | +21.1% | +6.4% | -6.8% |

Source: ExportPlanning Information System

Would you like to receive a selection of the most relevant international trade news every week? Subscribe to the World Business Newsletter free of charge!

Main markets

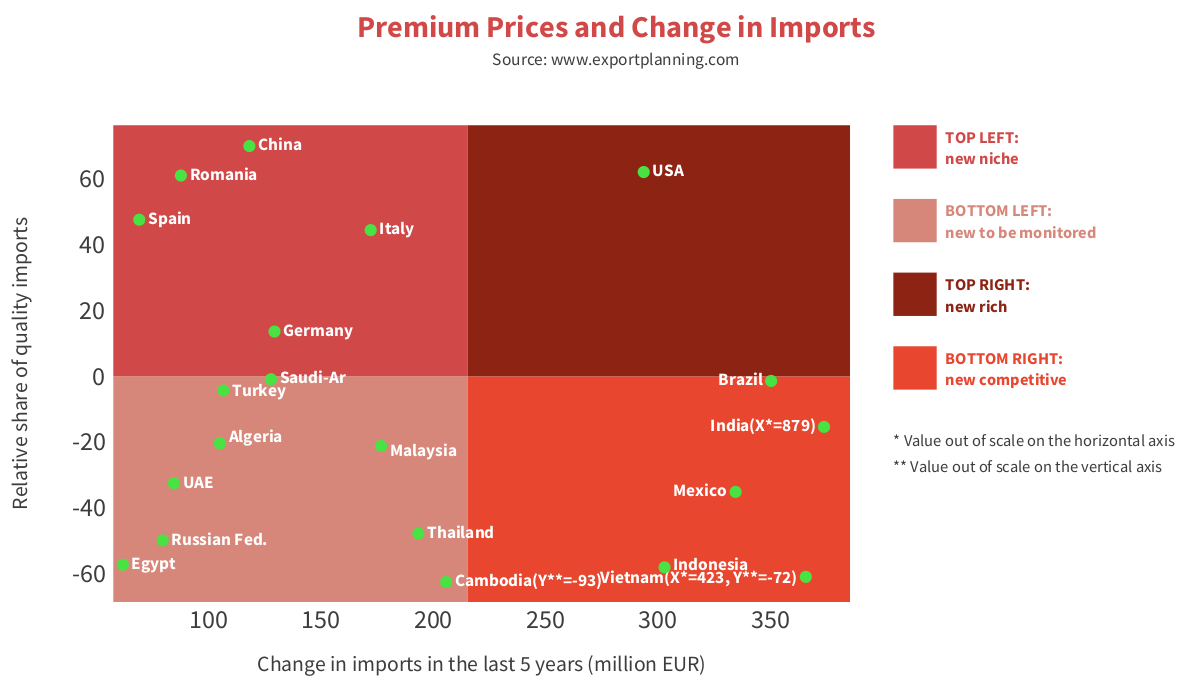

The world's leading destination markets for plastic processing machinery are China, the United States and India. In 2025, China imported machinery worth 2 059 mln €, accounting for a 10.5% share of global imports. Between 2009 and 2025, Chinese imports recorded a compound annual growth rate (CAGR) of +1.2% at current prices. Compared with the other major markets, China experienced a significant reduction in imports, increasingly replacing foreign machinery with domestically manufactured equipment. As shown in Figure 2, however, the Chinese market continues to absorb primarily high-quality machinery.

The United States imported plastic processing machinery worth 1 815 mln € in 2025, representing 9.2% of international trade. Over the 2009–2025 period, imports recorded a CAGR of +5.9%. India, meanwhile, posted an average annual growth rate of +8.5%, with imports reaching 1 484 mln € in 2025.

Together with Brazil, Vietnam, Indonesia and Mexico, India is among the markets that have significantly increased their imports of plastic processing machinery over the past five years. However, as illustrated by the premium price analysis in Figure 2, this growth has mainly involved lower-priced machinery. The United States, by contrast, stands out as a high-value market characterized by strong demand growth for medium-high and premium-quality machinery.

Fig. 2 – Plastic processing machinery: premium price analysis in the most dynamic markets

(2020–2025)

Source: ExportPlanning analysis – Reporting Tool

Competitive landscape

China dominates the global competitive landscape for plastic processing machinery exports. In 2025, it was the world's leading exporter, accounting for a 30.4% market share with exports valued at 6 229 mln €. It was followed by the European economies of Germany, Italy and Austria, while Japan ranked next. Only Germany recorded a market share exceeding 20% in 2025, whereas all the other major exporting countries accounted for less than 10% of global exports.

Between 2009 and 2025, China experienced remarkable export growth, posting a compound annual growth rate (CAGR) of +11%. The main foreign markets for Chinese manufacturers include Vietnam, India, Indonesia, Thailand and Russia. Chinese exports continue to be characterized by a strong concentration in the low- and medium-low-price segments.

Germany exported plastic processing machinery worth 4 194 mln € in 2025, a value 2.8% lower than the previous year. Over the 2009–2025 period, German exports recorded a CAGR of +1.9% at current prices.

For Italy, exports amounted to 1 813 mln € in 2025, representing a 5.5% decline compared with the previous year. Nevertheless, over the 2009–2025 period, Italian exports achieved an average annual growth rate (CAGR) of +1.9%.

Conclusions

The analysis highlights how the international market for plastic processing machinery is evolving according to increasingly differentiated competitive dynamics. On the one hand, several markets continue to compete primarily on price; on the other, a growing number of countries are rewarding solutions with higher technological content, greater energy efficiency, advanced automation and enhanced sustainability.

In such an environment, the ability to promptly interpret changes in global demand, monitor the most dynamic markets and assess competitors' positioning becomes a strategic asset. These capabilities enable companies to identify the most promising growth opportunities and to develop more effective internationalisation strategies.

1. The Harmonized System (HS) codes considered for this analysis are: HS847710, HS847720, HS847730, HS847740, HS847759 and HS847780.

You may be interested in:

Footwear: how are the manufacturing Countries performing in the first half of 2026?

Published by Mauro Badanelli. .

Conjuncture Industries Foreign markets International marketingAfter analyzing the dynamics of global trade in footwear machinery in a previous article, attention now shifts to the finished product, in order to examine the most recent performance of the main foot}... [ Read all ]

Export 2026-2029: ExportPlanning updates its forecast scenario

Published by Marzia Moccia. .

Conjuncture Export markets Uncertainty IMF Global economic trendsFor exporting companies, the ability to promptly interpret the evolution of international markets is now a key competitive factor. In a global context characterized by rapid changes and growing unce}... [ Read all ]

Footwear Machinery: the map of Growing and Slowing markets in Q2 2026

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Foreign markets International marketingFor exporting companies, the international context is changing increasingly rapidly. Relying on consolidated year-end data often means arriving too late. Having indicators updated to the second quarte}... [ Read all ]