Bank of Russia’s parachute shields the rouble

Published by Alba Di Rosa. .

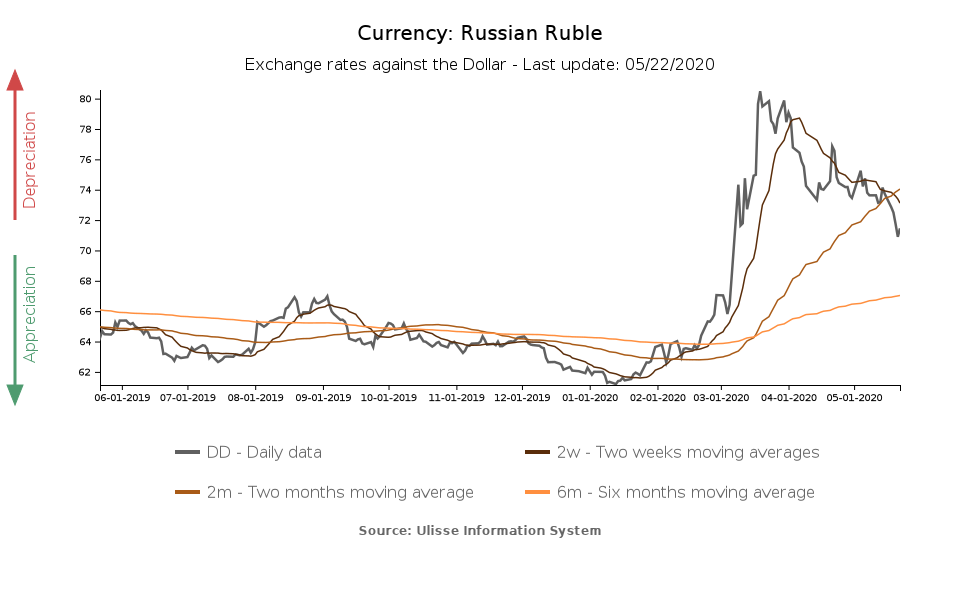

Exchange rate Emerging markets Russian rouble Exchange rate risk Oil Central banks Exchange ratesAmong EM currencies showing the most vigorous rebound after the Covid-19 shock on financial markets, we can find the Russian ruble. As can be seen from the chart below, the rouble experienced a sharp depreciation against the dollar during March, aggravated by the collapse in oil prices, and then gradually recovered from April. The recovery has accelerated in the last few days, bringing the rouble to its highest level in the last 2 months.

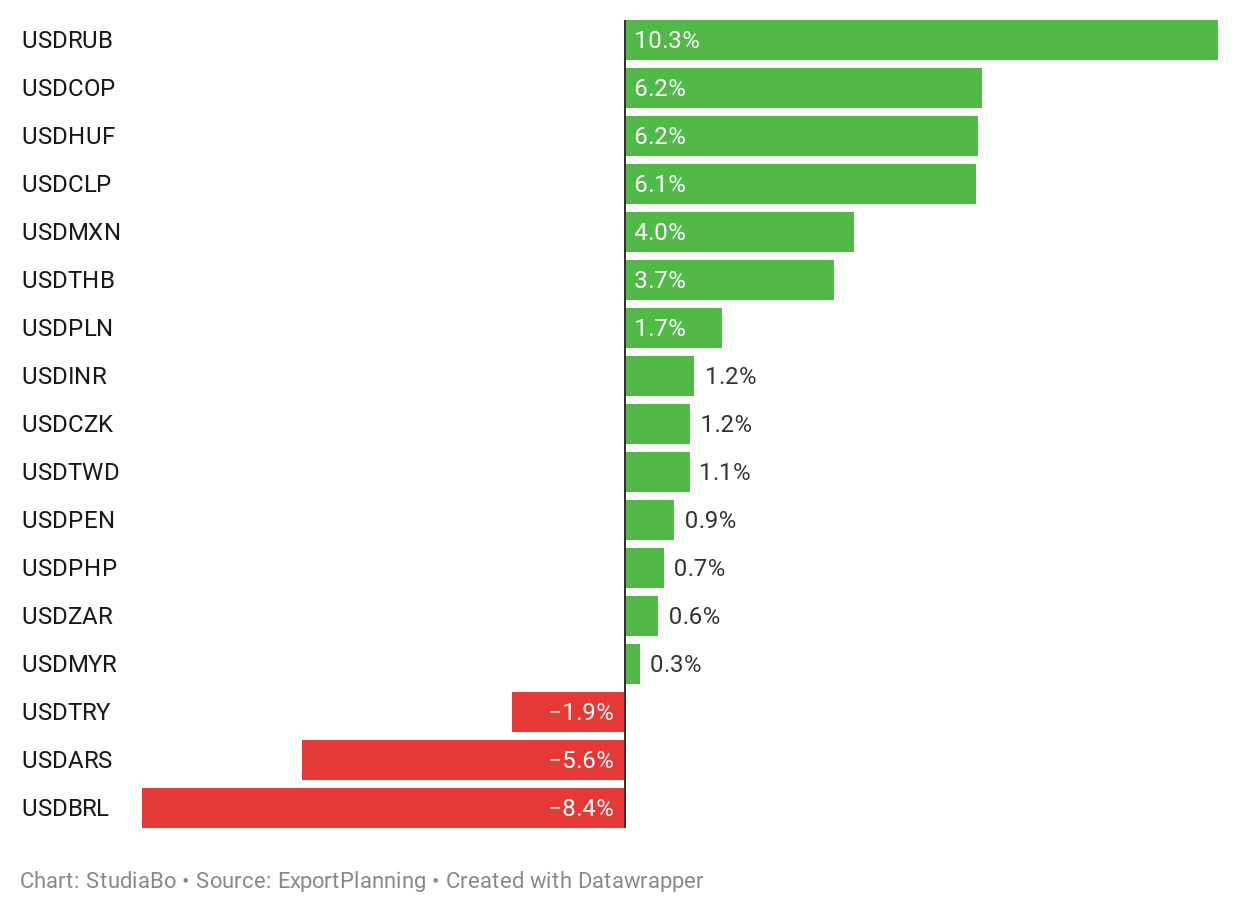

Comparing the dynamics of the Russian currency, from the beginning of April to date, with the rest of the floating EM currencies cluster, the outperformance of the rouble can be clearly identified, with its 10% recovery against the dollar. The Colombian peso, the Hungarian forint and the Chilean peso recorded a significant but lower 6% recovery, while the Thai baht and the Mexican peso stopped around 4%. For the rest of the group, we can see a stabilization on the levels reached at the beginning of April, rather than an effective recovery, or even a continuation of the depreciation trend in the cases of Turkish lira, Argentinean peso and Brazilian real, linked to the presence of domestic economic problems and weaknesses on top of the external symmetric shock.

Floating EM currencies: exchange rate % change against the dollar

(April 2020-present)

An additional element that puts the dynamics of the rouble in the spotlight is the prosecution of the phase of weakness of the price of oil: in spite of a recovery started the last month, the price of crude oil still remains significantly lower compared to the pre Covid crisis levels, a factor that, as is well known, should put pressure on exporting countries’ currencies.

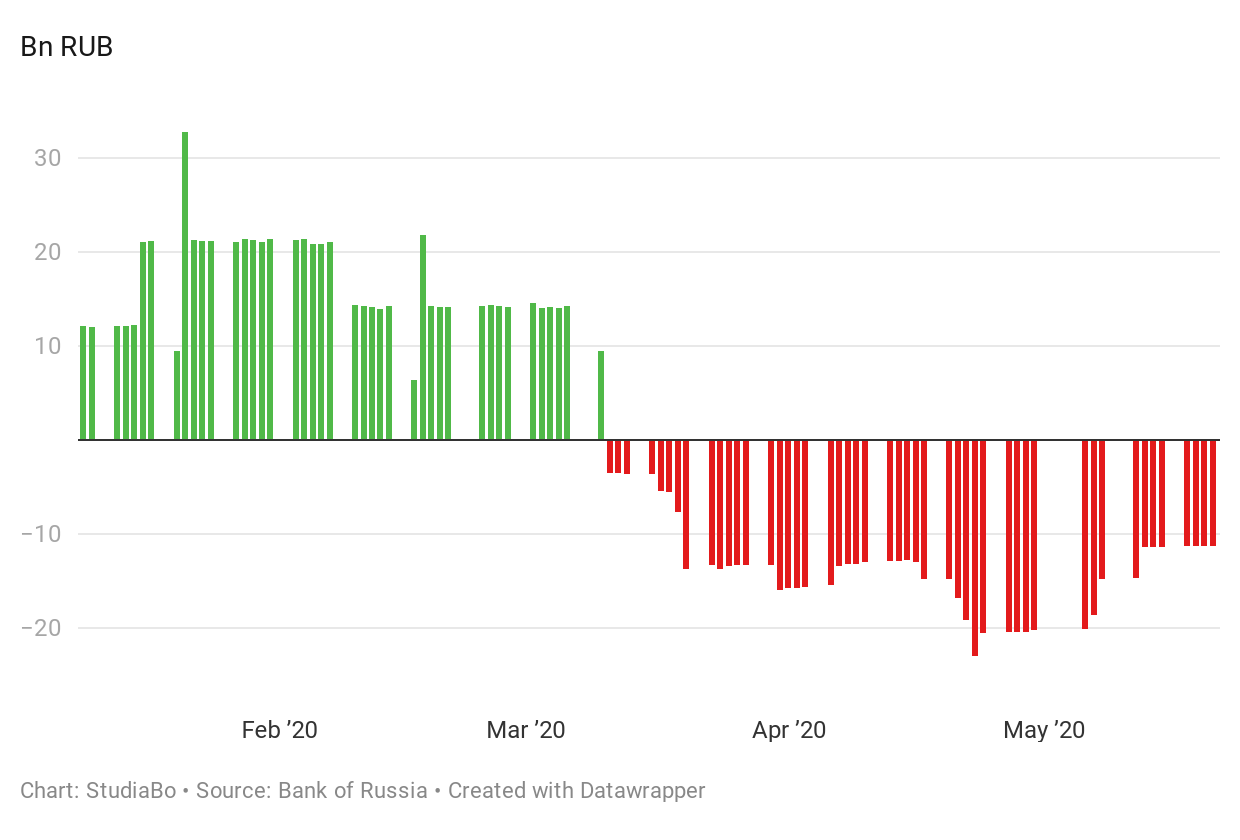

The link between the rouble exchange rate and the price of oil has always been strong over the years, as clearly shown in 2014, when the fall in crude oil prices had a heavy impact on the Russian currency and economy. The current scenario is more encouraging, at least for the moment, as the country is better equipped to deal with such events. In recent years, the impact of oil prices on the exchange rate has been reduced thanks to the so-called "budget rule", according to which the proceeds from oil sales exceeding $42.4 per barrel are allocated to the National Wealth Fund. In a case like the current one, however, with the price of oil falling well below the threshold since mid-March, the budget rule requires, on the other hand, accumulated foreign currency proceeds to be sold, so as to reduce exchange rate volatility.

In addition to the sale of foreign currency coming from oil revenues, the Bank of Russia (CBR) has recently obtained an additional source of income from the sale of its stake in Sberbank to the Russian Ministry of Finance: this amounts to more than $20 bn worth of foreign currency, which the CBR has started selling on FX markets since 19 March, when the price of oil falls below $25 a barrel.

The combined effect of the two measures is shown in the graph below.

CBR: Purchase/sale of foreign currency on domestic FX market

On top of the already mentioned supporting factors for the rouble, in April a recovery in portfolio flows to the OFZ market has taken place as well. The demand for OFZ, Russian government bonds denominated in rubles, has been confirmed in May auctions, too. While this trend clearly signals the perceived attractiveness of Russian assets, according to analysts this could also potentially communicate a general improvement in investor sentiment, thanks to the situation on the Covid front which shows, in many countries of the world, the first attempts to return to normal.

You may be interested in:

IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsPer il 2026 il Fondo ha rivisto lievemente al ribasso le stime di crescita del PIL mondiale, ora previsto al +3% [ Read all ]

January 2026: the latest data on global trade in goods

Published by Marzia Moccia. .

Slowdown Exchange rate Conjuncture Dollar Euro Foreign markets Uncertainty Global economic trendsThe availability in the ExportPlanning Information System of global trade data for January makes it possible to update the short-term outlook on the most recent dynamics of world trade in goods, wit}... [ Read all ]

B-READY 2025: the World Bank’s new compass for economic development

Published by Veronica Campostrini. .

Macroeconomic analysis Foreign markets Economic policy Central banks Foreign market analysisWith the publication of the Business Ready 2025 report, the World Bank introduces the new B-READY (Business Ready) index, intended to permanently replace the previous Doing Business, which was suspend}... [ Read all ]