Economic signals from world trade in capital goods

An analysis by geographic area

Published by Simone Zambelli. .

NAFTA Asia Conjuncture Foreign markets Eurozone Foreign market analysisThere has been increasing talk in recent months about the slowdown in the world economy, caused by the high level of uncertainty on the international scene, a direct consequence of several critical issues that threaten world growth in the next two years, primarily the Russia-Ukraine war and soaring inflation.

In a context of significant uncertainty, such as the current one, monitoring information on the investment policies of firms around the world are crucial in order to assess the sentiment of economic agents regarding the challenges facing the near future, such as the possible reconfiguration of global value chains, and related production location decisions, as well as the rising cost of credit, linked to more restrictive policies by central banks.

This analysis focuses on the dynamics that have characterized global imports of equipment, machinery and plant goods, segmented by trade areas, in order to provide an initial reading of the demand for the corresponding goods as a first proxy for related investment policies.

As documented in a previous article (World export of Investment Goods for industry holding in 4th quarter 2022), a first element of interest is the relative resilience that is characterizing the demand for capital goods, such as ICT Tools and Equipment, Transport Equipment, Industrial Process Machinery and Equipment, Industrial Tools and Equipment, and Industrial Plant.

After fully recovering in 2021 from the pre-pandemic levels of 2019, capital goods were, in fact, also on the rise in the last quarter of last year, testifying to a relative resilience and marking a 6 percent annual growth in quantity at pre-2022.

To what is this resilience attributable? And what are the geographic areas that are sustaining this dynamic?

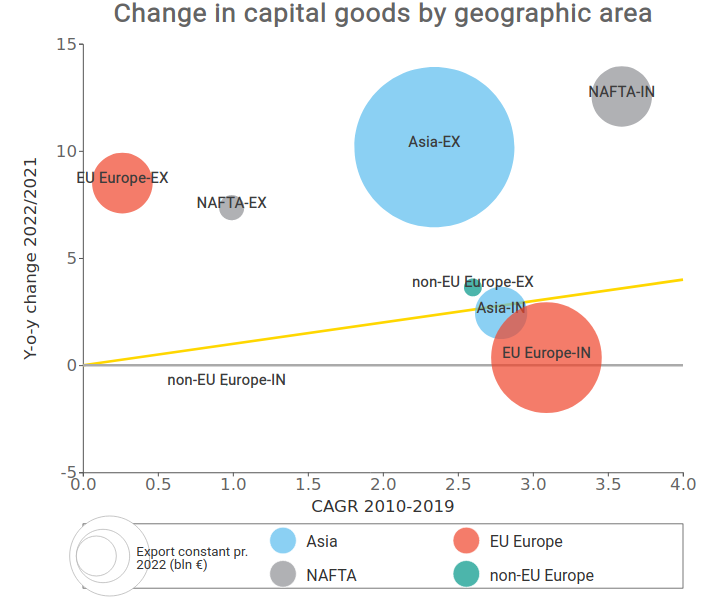

First, it is useful to look at the phenomenon from a geographical perspective, with a focus on the dynamics of interregional trade. The following graph shows the growth in demand for capital goods, dividing the flows between demand for goods within the home area (suffix -IN) and demand outside the home area (suffix -EX).

On the y-axis we find the annual trend change recorded last year, while on the x-axis we find the long-term growth that characterized the pre-pandemic decade (2010-2019 period).

The comparison between the two was introduced in order to capture any acceleration phenomena with respect to a longer time horizon; the ball magnitude is proportional to the value of exports at constant prices in 2022.

Source: ExportPlanning.

Taking into account the pace of development that has characterized the different areas over the past decade, it is particularly significant to highlight how it is mainly Asian demand, satisfied by out-of-area partners, and U.S. demand, in this case attributable to intra-area partners, that most sustained the resilience of demand for capital goods in quantity over the past year, marking a 10 percent and 17 percent growth over 2021 in quantity, respectively.

Compared to the two areas just mentioned, the growth in quantity of demand for investment goods from the EU is relatively less intense, especially in intra-EU trade in investment goods.

North America: significant tightness in electronics and commercial vehicle trade

Supporting the results of intra-regional North American trade has been mainly the Electronics and Freight Vehicle segments.

Both sectors appear to be growing at double-digit rates in 2022, consolidating at levels well above pre-crisis levels and accelerating over the medium term.

Asia: growing investment demand from Vietnam, Taiwan and Malaysia

Asia has emerged as a leading area for global demand for capital goods for many years now, with the Dragon Country playing a dominant role. It is interesting to point out that, however, among the Asian countries that are supporting the demand for capital goods, in the most recent months we find especially the economies of Vietnam, Taiwan and Malaysia.

Also for the Asian continent, the dominant sectors in 2022 are computer electronics and telecommunications equipment, along with earthmoving machinery. However, as anticipated, compared to what has been observed in the North American case, this is still trade between Asia and out-of-area partners, denoting the dependence of local geographies on Western technology.

Conclusions

Based on early evidence, the resilience of global demand for capital goods appears to be strongly supported by overseas countries, with the electronics segment playing an absolute leading role. Indeed, the segment is now increasingly central within the rocess of digitalization and technological transformation of the world economy. In addition, monitoring information on world trade in intermediate goods within different areas during the most recent months will be a significant piece in understanding whether the changes we are witnessing can be ascribed within a process of reconfiguration of world production.

You may be interested in:

Global trade in footwear machinery: China dominates, Italy leads the way in premium technology

Published by Mauro Badanelli. .

Industrial equipment Conjuncture Foreign markets International marketingThe footwear machinery industry represents one of the pillars of manufacturing innovation in the fashion sector. In an increasingly competitive environment, characterized by global markets, growing }... [ Read all ]

World Trade Trends: International Trade Results in Q2 2026 (Preliminary Estimates)

Published by Marcello Antonioni. .

Home items Fashion Food&Beverage Metal industry Intermediate goods Electronics Chemicals Industrial equipment Conjuncture Automotive Global demand Industries Global economic trendsStrengthening dynamics, driven by AI applications, and the green and digital transitions [ Read all ]

Blue jeans, shifting geographies: the challenge faced by new manufacturing Countries to China and Bangladesh

Published by Mauro Badanelli. .

Fashion Export Foreign markets International marketingBlue jeans: an iconic fashion product Blue jeans are one of the iconic products of the apparel industry, with a well-established presence in markets around the world and demand spanning generat}... [ Read all ]