Space Economy: the new space race

Published by Marzia Moccia. .

High-tech International marketing

The space economy is playing an increasingly important role in the global economic and technological landscape. The growing diffusion of space-related products and services now influences not only the activities of public institutions but also the daily lives of citizens, making the sector a strategic element for economic and social development.

More and more aspects of life on Earth rely on satellite signals and data, stimulating new public and increasingly private investments.

Space has been considered strategic since the Cold War. After nearly sixty years, the centrality of the space sector has increased significantly: space has proven to be a technological and scientific driver across a wide range of application areas.

Technologies developed for space activities have significant spillover effects in sectors such as precision agriculture and weather forecasting, infrastructure monitoring and maintenance, Earth observation, and climate change analysis, enabling a more accurate understanding of environmental phenomena and their impacts.

Satellite platforms in Earth orbit also play a crucial role in emergency management and civil protection activities, providing essential data and services for coordinating rescue operations following natural disasters and for implementing risk prevention and mitigation strategies. Earth observation satellite constellations also contribute to monitoring migration flows, border surveillance, cultural heritage protection and the management of air and maritime transport systems, enhancing the efficiency and security of infrastructure and services.

Looking ahead, the development of new satellite networks could foster the expansion of high-capacity global connectivity services, reducing dependence on traditional terrestrial infrastructure and broadening access to digital technologies even in remote areas.

It is no coincidence that interest in and the strategic vision for space activities are expanding globally, with a record number of countries and commercial actors now investing in space programs. While in 1960 only two countries were essentially investing in space, today the space economy attracts widespread geographical interest, with satellites in orbit registered in more than 80 nations.

The growing expansion of the space economy has been driven by increasing accessibility to the space sector. The dramatic reduction in launch costs, made possible primarily by reusable launch vehicles, has been combined with the miniaturization of components and satellites. This transformation has enabled a shift from extremely costly systems to more affordable, flexible, and easily replaceable solutions, lowering barriers to entry for new public and, above all, private players. In the United States, for example, the growing influence of the private sector within the American space economy ecosystem is clearly evident.

The international competitive landscape

Given the increasingly central role of space applications in the global economy, the space economy is expected to consolidate its position as one of the main arenas of technological, industrial, and geopolitical competition, with significant implications for international economic and strategic balances. In this context, it is worthwhile to analyze the competitive positioning of the key players operating in the sector by examining their role in international trade.

In this regard, defining the space economy precisely is essential for measuring its value and comparing its evolution internationally. According to the OECD definition, it encompasses all activities, resources, products, and services that generate value through the exploration and utilization of space. It is therefore not limited to the space sector in the strict sense but also includes all economic and social effects generated by space technologies and data, which are increasingly integrated into everyday activities and across various sectors of the economy, including the services ecosystem.

For the purposes of this article, however, two representative and indicative products of the sector have been identified and used as indicators to analyze its dynamics and degree of integration into international value chains:

- HS880260 - Spacecraft, including satellites, and their launch vehicles and suborbital payload launch vehicles;

- HS880790 - Parts of spacecraft and launch vehicles.

International trade and major players

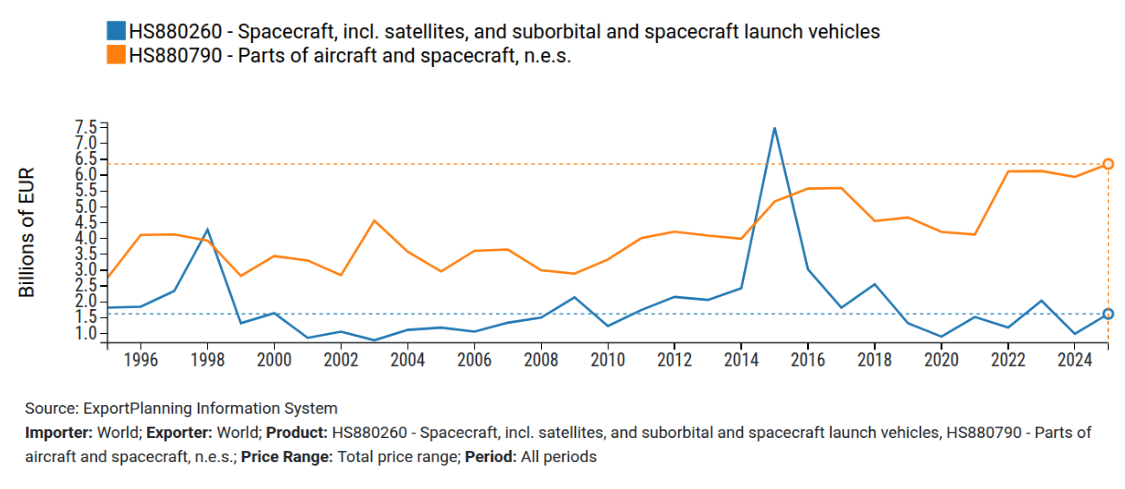

In 2025, global trade in spacecraft, satellites, and related components reached an estimated value of approximately €8 billion. International trade flows show a progressive decline in the relative weight of complete spacecraft, alongside a growing share of components, subsystems and spare parts. This trend reflects the increasing modularization of space architectures, the spread of reusable launch vehicles, and the resulting transformation of global value chains, which are fostering increasingly sophisticated demand for intermediate technologies and specialized components.

Fig.1 – Global Trade in Spacecraft, Satellites and Parts

Source: ExportPlanning

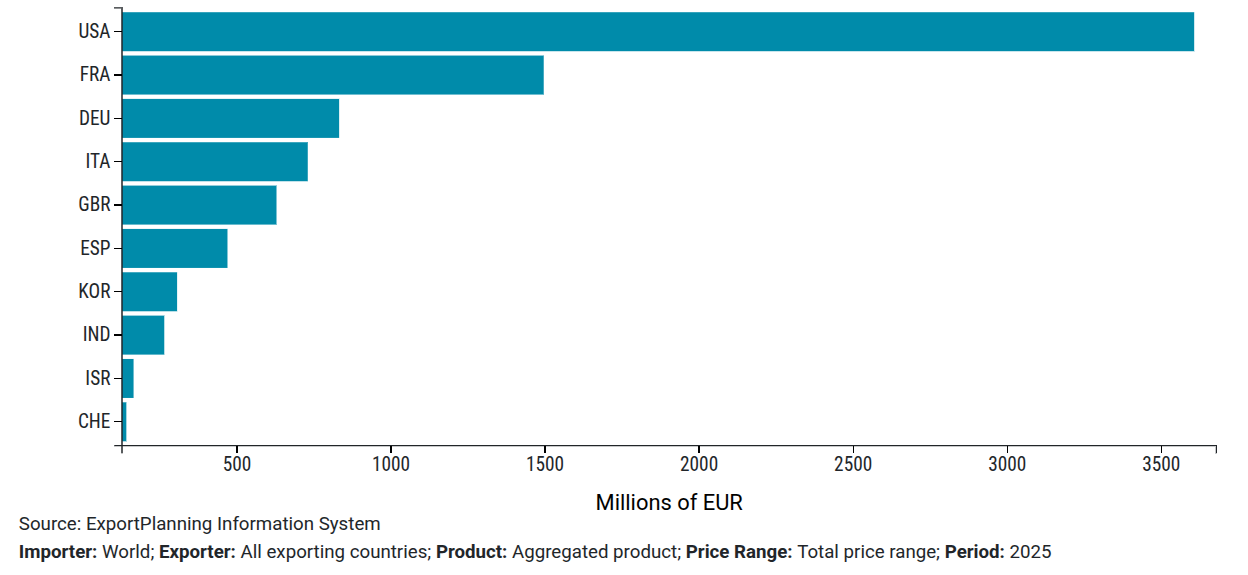

The pace of the "space race" is being set by the United States, the world's leading exporter in the sector in 2025, followed by major European economies and emerging players in Asia.

On the international stage, the United States demonstrates a strong productive specialization in the space economy, with a trade surplus of €975 million and a normalized trade balance (NTB1) of +0.21.

Europe also maintains a prominent position thanks to several highly specialized economies: Italy records a trade surplus of €391 million (NTB +0.28), while Spain shows an even higher degree of specialization, with €280 million and an NTB of +0.46, supported by the development of its satellite supply chain, space operators, and an emerging private launch segment.

In Asia, meanwhile, heterogeneous but rapidly evolving dynamics are emerging: South Korea has developed a complete industrial ecosystem that includes satellites, components, and launch systems, supported by increasing technology transfer to the private sector, resulting in a trade surplus of €215 million and an NTB of +0.50.

Fig.2 – Leading Exporters of Spacecraft, Satellites and Parts

Source: ExportPlanning

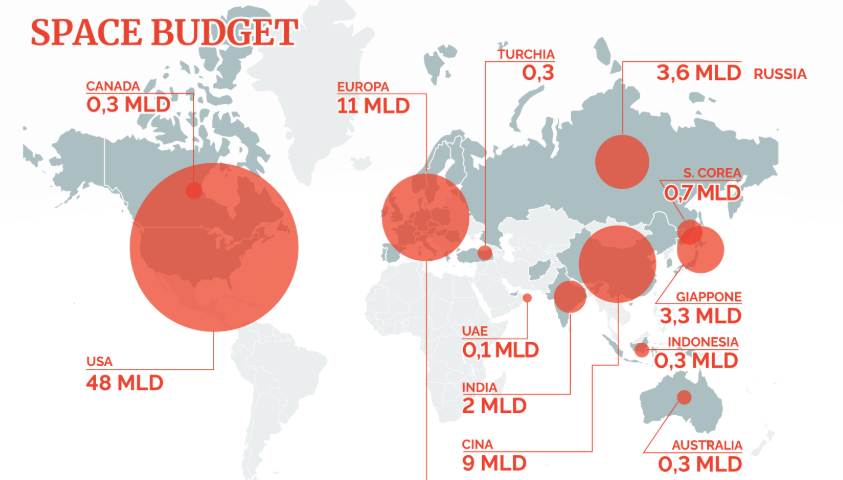

It is also useful to complement this trade information with data on public and private investments in space programs, which largely reflect a country's ability to sustain long-term industrial and technological policies in the sector.

Fig.3 – Public and Private Investments in the Space Economy

Source: ISPI based on Euroconsult data

The map of public and private investments in space programs confirms the centrality of the American and European regions, which continue to represent the main hubs for financing and developing the global space economy. At the same time, it highlights the growing participation of emerging economies, particularly India, which is significantly strengthening its involvement in space programs through increasing institutional and industrial commitments.

Comparing investment intensity with positioning in international trade flows also highlights the particular case of China: its strong public investment is not fully reflected in its position as an exporter of space-related goods. Several OECD and CSIS studies emphasize that the country has developed a largely "state-led" space ecosystem focused on domestic demand. In this sense, China represents a typical example of an “investment-heavy but export-limited space economy,” where sector growth is driven more by industrial and national security policies than by the full internationalization of its production value chains.

Conclusions

The analysis of the space economy highlights a rapidly expanding sector that is set to play an increasingly central role in global economic, industrial, and geopolitical dynamics. The combination of growing public and private investments, technological innovation, and the strategic relevance of space applications—from global connectivity and Earth observation to navigation and security systems—reinforces its structural importance as a long-term growth driver.

Europe continues to play a leading role as a major international player in the sector, while also retaining significant untapped growth potential. Its established industrial expertise, structured space programs, and advanced technological base position Europe among the main hubs of the global space economy. However, the strong growth dynamics of other international players make it crucial to strengthen investment capacity, industrial coordination, and innovation.

In a scenario where space is increasingly becoming a field of economic, technological, and geopolitical competition, stronger investment and European cooperation will be essential to consolidate the continent’s role as a key player in the space economy of the 21st century.

1. The “simple” trade balance (Exports - Imports) is heavily influenced by market size. The normalized version, however, enables more meaningful comparisons:

- between different countries;

- between sectors of different sizes;

- over time.

The NTB can assume values ranging from -1 to +1:

- +1 → exports only, no imports (maximum surplus);

- 0 → exports equal imports;

- -1 → imports only, no exports (maximum deficit).

- positive NTB values (and increasing over time) indicate strong specialization in a given sector or product;

- negative NTB values (and decreasing over time) indicate dependence on imports and a lack of specialization;

- NTB values close to zero indicate a balanced situation.

You may be interested in:

Advanced Technology Products: Overview and Dynamics of Global Technological Leadership

Published by Marcello Antonioni. .

Global demand Competitor analysis High-tech International marketingChina and the United States are competing for global technological leadership; Europe is catching up, showing some interesting areas of specialization [ Read all ]

High-tech sectors are driving global trade in the first nine months of 2025.

Published by Marzia Moccia. .

Conjuncture Global demand Industries Uncertainty High-tech Global economic trendsThe availability of ExportPlanning’s foreign trade data updated to Q3 2025 makes it possible to highlight how, in the cumulative total for the first nine months of 2025, the US market represented a su}... [ Read all ]

World trade in capital goods: Q2-2025 confirmed overall positive trends

Published by Marcello Antonioni. .

Metal industry Industrial equipment Conjuncture Automotive Industries Uncertainty High-tech Global economic trendsThe measurement at constant prices confirms the (albeit moderate) signs of strengthening of the industry outlook, but with significant differences at the sectoral level [ Read all ]