Denim: how global trade is changing amid new materials and competitive pressure

Published by Mauro Badanelli. .

Fashion Internationalisation Export International marketingThe evolution of denim in fashion

Denim is one of the most iconic and versatile fabrics in the history of apparel. Its origins date back to the 17th century and are linked both to the Italian city of Genoa, renowned for producing a durable cotton fabric used for workwear, and to the French city of Nîmes, where the famous serge de Nîmes fabric was developed, giving rise to the term "denim." Over time, this material has evolved far beyond its original function, becoming a distinctive element of contemporary culture.

Originally developed as a hard-wearing fabric, denim has gradually become a symbol of style, cultural identity, and innovation. Its worldwide success is the result of its unique combination of durability, comfort, and versatility, enabling it to adapt continuously to changing consumer preferences, fashion trends, and market requirements. Today, denim remains at the heart of the global apparel industry, combining tradition, technological innovation, and an increasing commitment to the sustainability of manufacturing processes.

Global denim trade

From a customs classification perspective, denim fabrics are primarily identified under HS 520942 and HS 521142. These codes mainly refer to denim fabrics used in the production of blue jeans. HS code 520942 covers traditional denim containing more than 85% cotton, while HS code 521142 includes blended denim fabrics made of cotton combined with man-made or synthetic fibres.

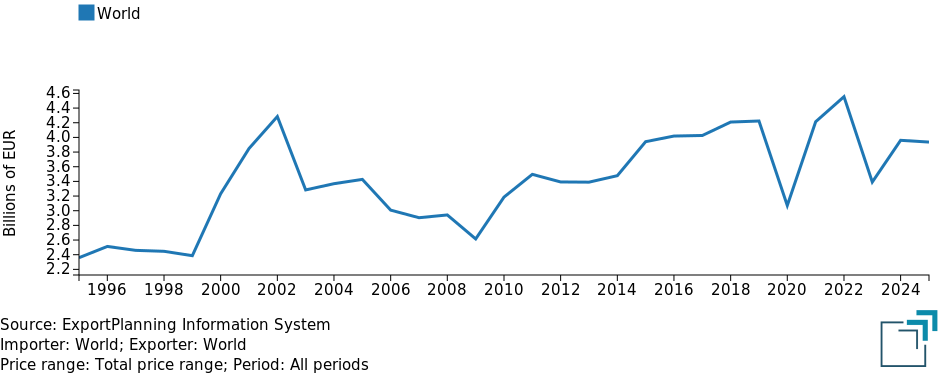

The analysis of international trade over the past three decades highlights how the global denim market has undergone several distinct phases of development. Following strong expansion during the early 2000s, driven by the worldwide popularity of blue jeans, international trade declined between 2002 and the Great Recession of 2008–2009. In the years that followed, global trade gradually recovered before entering a phase of relative stability over the last decade. Between 2015 and 2025, the value of international denim trade remained close to €4 billion, despite cyclical fluctuations such as the demand contraction caused by the COVID-19 pandemic and the slowdown experienced by the textile industry beginning in 2023.

This apparent stability, however, conceals a significant structural shift: the gradual decline in trade of predominantly cotton denim fabrics (HS 520942), contrasted by the rapid expansion of blended denim fabrics containing man-made or synthetic fibres (HS 521142). Between 2009 and 2025, the latter recorded a compound annual growth rate (CAGR) of 8.8%, compared with -0.3% for denim made primarily of cotton.

Fig. 1 – Denim fabrics: global trade

(current prices)

Key market players

An analysis of the leading players in the global denim fabric market (worth approximately €3.9 billion in international trade in 2025) reveals two distinct profiles: on one hand, the high-volume manufacturing giants dominated by Asia; on the other, integrated industrial hubs engaged in two-way trade flows.

The table below ranks the world's largest net exporters of denim fabrics by their 2025 net export value.

The top ten exporters are ranked according to their 2025 trade balance, combining total export value with the Normalized Trade Balance (NTB), an indicator measuring a country's degree of specialization, where a value of 1 identifies a pure exporter and 0 represents perfectly balanced two-way trade.1

Table 1 – Denim fabrics: Leading global market players (2025 data)

| Exports | Trade Balance | |||

| # | Country | € million | € million | Norm. (-1/+1) |

| 1 | China | 1 750 | 1 679 | 0.92 |

|---|---|---|---|---|

| 2 | Pakistan | 533 | 521 | 0.96 |

| 3 | India | 374 | 352 | 0.89 |

| 4 | Turkey | 298 | 217 | 0.57 |

| 5 | Japan | 59 | 56 | 0.91 |

| 6 | Brazil | 41 | 39 | 0.91 |

| 7 | Thailand | 50 | 37 | 0.59 |

| 8 | United States | 70 | 29 | 0.26 |

| 9 | Italy | 68 | 8 | 0.07 |

| 10 | Hong Kong | 43 | 7 | 0.09 |

Source: ExportPlanning – Data Hub – Annual Trade Data, Datamart Ulisse

China not only leads the global ranking, accounting for 43.2% of worldwide denim exports, but also records an exceptionally high NTB (0.92). This indicates that the country acts almost exclusively as a supplier of denim fabrics to the rest of the world, with imports remaining limited (around €71 million) compared with its enormous export capacity.

Pakistan and India follow China among the world's leading net exporters. Pakistan represents the most specialized case, with an NTB of 0.96. It exports denim worth €533 million while importing only around €12 million, confirming its role as a highly export-oriented manufacturing hub for this textile intermediate product. India follows a similar pattern, posting a trade surplus of €352 million and an NTB of 0.89.

Turkey displays a different profile (NTB 0.57). While remaining a major exporter (€298 million), it also imports significant volumes of denim fabric (around €81 million), acting as both a manufacturing and distribution hub for the Euro-Mediterranean region. Thailand shares a similar intermediate-trade profile, with an NTB of 0.59.

Among the leading players, Italy, the United States, and Hong Kong (which mainly serves as a logistics hub) record the lowest normalized trade balances. Italy, with an NTB of just 0.07, exports high-value denim products (€68 million) while importing almost the same amount (approximately €59 million). This reflects a highly developed industrial structure that imports raw or semi-finished denim fabrics before re-exporting premium, high-value-added finished products, a typical feature of the luxury fashion industry. The United States follows a similar pattern (NTB 0.26), with relatively balanced import and export flows.

Would you like to receive a selection of the week's most relevant international trade news? Subscribe free to the World Business Newsletter!

Global leaders' performance and developments during the first four months of 2026

The analysis of the 2022–2025 period reveals a structurally negative trend for almost all of the leading players in the global denim market, confirming that the industry has experienced a contraction over the past three years. The world's three largest net exporters — China, Pakistan, and India — all recorded negative compound annual growth rates (CAGR) in export values, highlighting a decline in the value of their international sales compared with 2022.

India recorded the weakest performance among the major Asian producers, with a CAGR of -7.5%. China followed with an annual decline of -4.9%, while Pakistan posted a more moderate contraction of -3.8%.

Among the world's leading manufacturing hubs, Turkey stands out for its greater resilience. Its CAGR of just -0.5% indicates that export values have remained broadly stable compared with 2022, confirming the country's position as the strongest competitor within the Euro-Mediterranean region.

Advanced economies, typically specialized in premium and high-value-added products, recorded the sharpest declines. Italy experienced the largest structural contraction, with a CAGR of -15.4%, while Japan posted -7.2% and the United States recorded -7.1%.

During the first four months of 2026, all the world's leading net exporters experienced a decline in exports compared with the same period of the previous year, reflecting a widespread slowdown in global demand. The three largest exporters — China, Pakistan, and India — all reported export declines of around 9%.

More pronounced signs of weakness emerged among premium producers such as Italy and Japan, whose exports fell by 12.0% and 20.6%, respectively. The decline recorded by the United States was comparatively more limited.

In sharp contrast with its Asian competitors, Turkey was the only major exporter to record robust growth during the first four months of 2026, with exports increasing by 9.6%. This performance may indicate a gradual shift in sourcing strategies—particularly among European buyers—towards geographically closer suppliers, or an improvement in the competitiveness of Turkish denim during the current market cycle.

Furthermore, as shown in Table 2, comparing trade volumes (kilograms) with export values (million euros) reveals a clear divergence, pointing to growing pressure on average unit prices worldwide. The compound growth rates show that, among the major Asian producers, export volumes increased while export values declined.

This trend became even more pronounced during the first four months of 2026, when the gap between quantity and value widened further.

A different pattern emerged among advanced economies (Italy, Japan, and the United States), where export values and volumes declined at similar rates, suggesting greater stability—or rigidity—in average export prices.

Table 2 – Denim fabrics: Global trade dynamics of the leading net exporting countries

| # | Country | CAGR 2025/2022 | YoY change Jan–Apr 2026 | ||

|---|---|---|---|---|---|

| Value (€) | Quantity (kg) | Value (€) | Quantity (kg) | ||

| 1 | China | -4.9% | +4.6% | -9.2% | +5.0% |

| 2 | Pakistan | -3.8% | +6.4% | -9.8% | +3.8% |

| 3 | India | -7.5% | +6.8% | -9.0% | +3.0% |

| 4 | Turkey | -0.5% | +8.2% | +9.6% | +14.5% |

| 5 | Japan | -7.2% | -10.2% | -20.6% | -17.3% |

| 6 | Brazil | -12.1% | -2.3% | -21.6% | -5.9% |

| 7 | Thailand | -8.6% | -5.4% | -20.7% | -31.4% |

| 8 | United States | -7.1% | -8.8% | -2.3% | +0.3% |

| 9 | Italy | -15.4% | -12.7% | -12.0% | -11.1% |

| 10 | Hong Kong | -29.9% | -27.4% | -46.6% | -43.2% |

Source: ExportPlanning analysis

Conclusions

The analysis of international denim trade shows that the industry is undergoing a profound transformation rather than merely experiencing a cyclical slowdown. While the overall value of global denim trade has remained broadly stable over the past decade, this apparent stability conceals significant structural changes. On the one hand, blended denim fabrics are steadily gaining market share, driven by growing demand for lighter, more elastic, and higher-performance materials. On the other hand, the slowdown observed between 2022 and the first months of 2026 has affected nearly all of the world's leading exporters, pointing to a more selective market characterized by weaker international demand and increasing competitive pressure.

In such a rapidly evolving environment, access to timely and up-to-date international trade data has become a strategic asset. Monitoring changes in global demand, identifying emerging competitive dynamics and anticipating technological trends enables companies to make better-informed investment decisions and strengthen their competitive position in the global denim industry.

1) The conventional trade balance (Exports − Imports) is heavily influenced by the size of a country's market. The Normalized Trade Balance (NTB), on the other hand, provides a more meaningful basis for comparison across countries, industries of different sizes and time periods. It is calculated as (Exports − Imports) / (Exports + Imports) and is one of the most widely used indicators in international competitiveness and trade specialization analyses. An NTB value close to +1 identifies a country that acts almost exclusively as an exporter, while values close to 0 indicate balanced two-way trade flows.

You may be interested in:

World Trade Trends: International Trade Results in Q2 2026 (Preliminary Estimates)

Published by Marcello Antonioni. .

Home items Fashion Food&Beverage Metal industry Intermediate goods Electronics Chemicals Industrial equipment Conjuncture Automotive Global demand Industries Global economic trendsStrengthening dynamics, driven by AI applications, and the green and digital transitions [ Read all ]

Blue jeans, shifting geographies: the challenge faced by new manufacturing Countries to China and Bangladesh

Published by Mauro Badanelli. .

Fashion Export Foreign markets International marketingBlue jeans: an iconic fashion product Blue jeans are one of the iconic products of the apparel industry, with a well-established presence in markets around the world and demand spanning generat}... [ Read all ]

Dyeing machinery: innovation and sustainability at the heart of a changing supply chain

Published by Mauro Badanelli. .

Industrial equipment Export Foreign markets International marketingDenim is one of the cornerstones of the global apparel industry. Every year, billions of garments are produced and sold worldwide, fueling demand from fast fashion brands, premium manufacturers, and}... [ Read all ]