The global trade of woodworking machinery: Italy’s position between quality excellence and global challenges

Published by Mauro Badanelli. .

Premium price Internationalisation Industrial equipment Foreign markets International marketingDespite an international scenario marked by a slowdown in global trade that began in 2023, Italy continues to hold a prominent position in the global woodworking technology1 industry, competing for leadership with the world’s main global players.

As already highlighted in a recent article, the three leading suppliers of woodworking technology are China, Germany, and Italy. In 2025 Chinese exports reached a value of 2,486 million euros (equal to 24.3% of global exports). Germany, meanwhile, exported machinery worth 2,262 million euros, accounting for a 22.1% market share.

Italy ranks as the third-largest technology supplier in the sector, with exports amounting to 1,374 million euros, corresponding to 13.4% of global exports. Over the years the growth of Chinese foreign sales has resulted in a contraction of market share for both Italy and Germany (Italy’s share stood at 20.5% in 2000). During the same period China’s market share rose from 1.6% to 24.3%.

An analysis of the 2015–2025 period shows a decline in the export share of EU countries (Germany and Italy, together with the significant contribution of Austrian exports), which fell from 57.0% to 53.4% of the global total. China was the sole beneficiary of Europe’s loss of competitiveness, as illustrated in Table 1.

Table 1 – Woodworking machinery – Exports by geographical area

(% share)

| AREA | 2015 | 2025 |

|---|---|---|

| EU Europe | 57.0 | 53.4 |

| China | 16.9 | 24.3 |

| Asia (excluding China) | 14.8 | 10.0 |

| NAFTA | 6.5 | 5.8 |

| Non-EU Europe | 3.8 | 3.7 |

| Other areas | 1.0 | 2.7 |

| TOTAL | 100.0 | 100.0 |

Source: ExportPlanning elaborations

On the other side China’s share increased by more than 7 percentage points, absorbing the loss of competitiveness of European suppliers. However, the consolidation of Chinese leadership does not appear to correspond to a technological upgrading of Chinese supply.

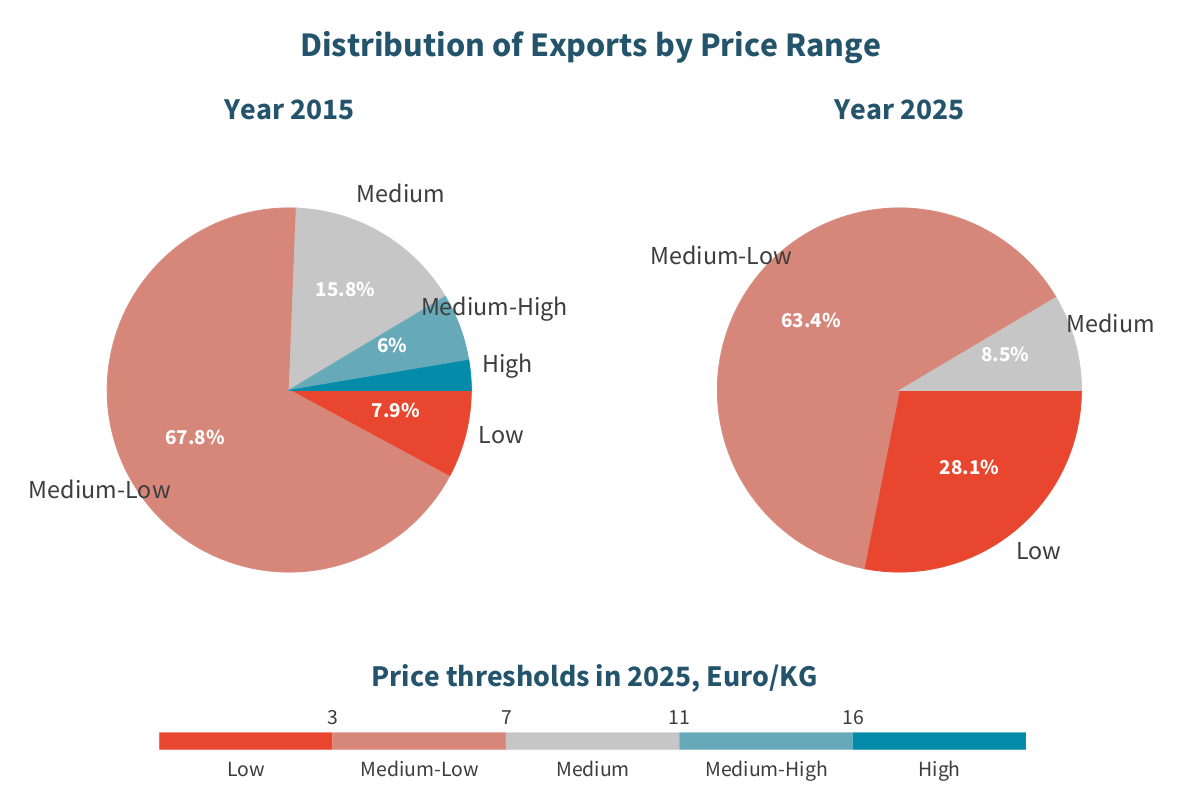

As illustrated in Fig. 1, the comparison between 2015 and 2025 in the distribution of Chinese exports by price range highlights how low-end and lower-mid-range exports increased their share of total exports, rising from 75.7% to 91.5%.

Fig.1 – CHINA - Distribution of woodworking machinery exports by price range

Source: ExportPlanning elaborations

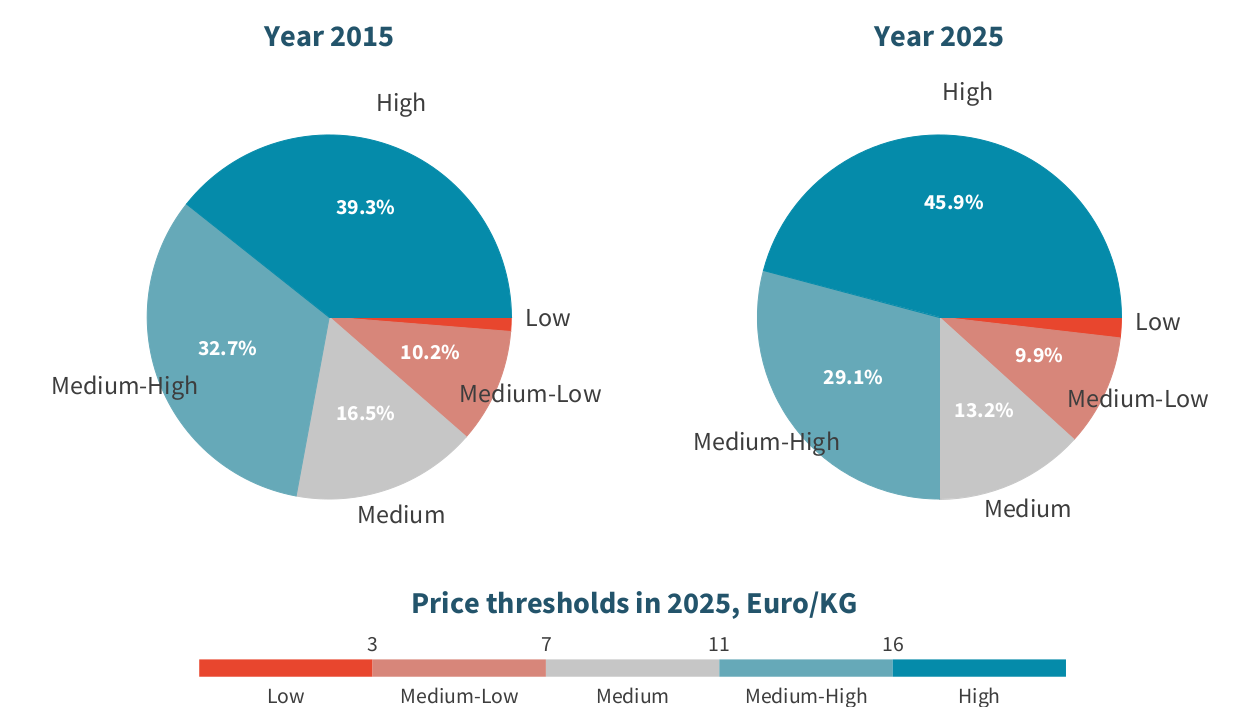

In a global environment that has witnessed the expansion of lower price ranges driven by the growth of Chinese supply, Italy has instead strengthened its position in the premium segment. The Italian industry has focused on secondary wood processing (panel processing and finishing), where precision and automation are essential and justify the recognition of a premium price by end users. Fig. 2 highlights the increase of more than 9 percentage points in the share of high-end and upper-mid-range Italian exports.

Fig.2 – ITALY - Distribution of woodworking machinery exports by price range

Source: ExportPlanning elaborations

Are you interested in receiving a selection of the most relevant foreign trade news of the week? Subscribe free to the World Business Newsletter!

Positioning by product segment

The product-level comparison based on the main HS codes for China, Germany, and Italy highlights specific specializations reflecting their positioning in the global market.

Machining centres (HS 846520)

This is the only segment in which Italy holds the undisputed global leadership, outperforming Germany with a 38.5% market share in 2025. Germany accounts for 31.4% of the market, sharing with Italy a leadership position in high-value-added technology. Although China ranks third, its share is much smaller (7.4%) and competition is mainly based on lower-price strategies compared to European suppliers.

Other machine tools and auxiliary machinery (HS 846599)

In this segment, which includes conditioning machinery and auxiliary equipment, China dominates due to its price competitiveness, with a 41.3% market share. Italy follows with 20.6%, while Germany’s share in this specific segment is limited to 3.9%.

Panel presses (HS 847930)

Germany leads the segment by volume, holding a 38.7% market share. China ranks second (23.0%), having doubled its share since 2008 through volume-based strategies. Italy is the world’s third-largest player with a 16.4% share. The Italian strategy is focused on qualitative differentiation in the manufacturing of particleboard and MDF panels.

Multi-purpose machines (HS 846510)

In this segment, Germany maintains an almost monopolistic position in high technology. The Country accounts for 53.1% of the global market share. Italy is the second-largest exporter with a 13.9% share, classified as a “leader competitor,” though with lower volumes and prices than Germany. China has only a marginal presence in this specific segment, with a 2.5% share.

Table 2 – Woodworking machinery – Global trade by product segment

(2025)

| Product code | Product name | Global trade (EUR million) |

Italy share % |

China share % |

Germany share % |

|---|---|---|---|---|---|

| HS846520 | Machining centres | 613 | 38.5 | 31.4 | 7.4 |

| HS846599 | Other machine tools and auxiliary machinery | 1 421 | 20.6 | 41.3 | 3.9 |

| HS847930 | Presses | 566 | 16.4 | 23.0 | 38.7 |

| HS846510 | Multi-purpose machines | 896 | 13.9 | 2.5 | 53.1 |

| HS846692 | Parts and accessories for machine tools | 1 641 | 12.3 | 13.8 | 15.8 |

| HS846593 | Grinding, sanding and polishing machines | 406 | 11.6 | 26.2 | 23.7 |

| HS846594 | Bending or assembling machines | 408 | 11.0 | 21.5 | 19.8 |

| HS846592 | Planing, milling or moulding -by cutting- machines | 688 | 7.1 | 29.4 | 16.8 |

| HS846591 | Sawing machines | 1 882 | 6.9 | 27.2 | 15.1 |

| HS846595 | Boring or mortising machines | 548 | 5.5 | 32.4 | 39.0 |

| HS846596 | Splitting, slicing or paring machines | 458 | 3.9 | 51.2 | 12.7 |

| TOTAL | Woodworking machinery | 9 528 | 13.4 | 24.3 | 22.1 |

Source: ExportPlanning elaborations

Forecast scenario through 2029

The ExportPlanning information system also makes it possible to formulate a forecast scenario through 2029 for global sector trade and, in particular, Italian exports.

The end of the post-pandemic boom, geopolitical and trade uncertainty, and increasingly intense price competition in international markets are factors negatively affecting the sector outlook. Data for the first quarter of 2026 discussed in a previous article confirm the persistence of a contraction phase in global demand (with a year-on-year change of -10.7% in euro) and a significant decline in Italian exports (-8.8%).

For global trade, the average annual growth rate for the 2026–2029 period is forecast at +1%, assuming a recovery in international trade starting from 2027. Forecasts for Italian exports remain negative (CAGR: -1%) due to the continuous erosion of market share by China. For the Asian Country, the forecast scenario points to progressive growth, which is expected to strengthen further starting next year.

Conclusions

Over the last decade, Italy’s positioning in the global woodworking machinery market has increasingly shifted toward the premium segment, characterized by high technological content, flexibility, and manufacturing quality. While competitors such as China focus on volume-based strategies at lower prices, the Italian industry has consolidated a leadership position based on added value and the ability to meet complex production requirements.

However, the technological leadership shared with Germany is not sufficient to ensure the consolidation of the market shares held by Italian manufacturers. Exporting companies must constantly monitor external market data. Particular attention should be paid to the dynamics of the competitive landscape, where price competition risks causing further losses in competitiveness for Italian companies, especially in certain product segments.

1. The Harmonized System (HS) codes considered for the analysis were the following: HS846510, HS846520, HS846591, HS846592, HS846593, HS846594, HS846595, HS846596, HS846599, HS846692, HS847930. ```

You may be interested in:

Hollow glass manufacturing machinery: Italy strengthens its position in global markets

Published by Mauro Badanelli. .

Internationalisation Industrial equipment Foreign markets International marketingIn a competitive landscape marked by increasing pressure from Asian manufacturers and the strong technological specialization of the world's leading exporters, the Italian hollow glass manufacturing m}... [ Read all ]

The Global Market for Hollow Glass Manufacturing Machinery: Trade Trends and Italy’s Competitive Position

Published by Mauro Badanelli. .

Internationalisation Industrial equipment International marketingFrom everyday food and beverage bottles to high-performance pharmaceutical containers, hollow glass products have undergone a remarkable technological transformation over the past decades. Growing r}... [ Read all ]

The most dynamic markets for Italian woodworking machinery

Published by Mauro Badanelli. .

Industrial equipment International marketingAs already discussed in a previous article, Italy is a reference player in the woodworking machinery sector for the breadth and quality of its technological offering. In particular, for the followi}... [ Read all ]