IMF WEO Update July 2026: a (precarious) balance between war and technology

Published by Alba Di Rosa. .

Macroeconomic analysis Asia Emerging markets United States of America Uncertainty IMF Eurozone Global economic trendsOn July 8, the International Monetary Fund released its World Economic Outlook Update. In both July and January, the Fund publishes an update of the key variables included in its macroeconomic scenario, which is released in spring and autumn and is available on the ExportPlanning platform.

The key findings of the analysis are summarised below.

Global growth figures

Let us begin with world GDP. Following stable growth of 3.5% in both 2024 and 2025, the Fund revised its forecast for the current year downwards by 0.1 percentage points compared with last April. As a result, world GDP is expected to grow by 3% in 2026, half a percentage point below the average recorded over the previous two years.

By contrast, the growth forecast for 2027 was revised moderately upwards, from 3.2% to 3.4%. On a cumulative basis, the scenario therefore remains broadly unchanged compared with the forecasts included in last April’s World Economic Outlook.

World GDP and GDP by macro-region: historical data and forecasts (%)

| Historical data | Forecasts | Difference from the April 2026 forecasts | ||||

|---|---|---|---|---|---|---|

| 2024 | 2025 | 2026 | 2027 | 2026 | 2027 | |

| World | 3.5 | 3.5 | 3 | 3.4 | -0.1 | 0.2 |

| Advanced economies | 1.9 | 1.9 | 1.7 | 1.8 | -0.1 | 0.1 |

| Emerging market and developing economies | 4.5 | 4.5 | 3.8 | 4.5 | -0.1 | 0.3 |

Source: StudiaBo elaborations on IMF data (World Economic Outlook Update, July 2026)

At present, the Fund has identified two main factors driving these modest revisions. On the one hand, there are the effects of the war in the Middle East, which are weighing on the global growth outlook. On the other hand, there is the positive impact of the accelerating global technology cycle, primarily driven by advances in and the spread of Artificial Intelligence.

The impact of these factors at country level varies according to each country’s exposure. The performance of energy exporters not directly involved in the conflict differs from that of economies participating in the intense development of new technologies. The countries currently facing the greatest disadvantages are those that import energy and have limited participation in the technology value chain, including many low-income countries.

Would you like to receive a selection of the week's most relevant international trade news? Subscribe free to the World Business Newsletter!

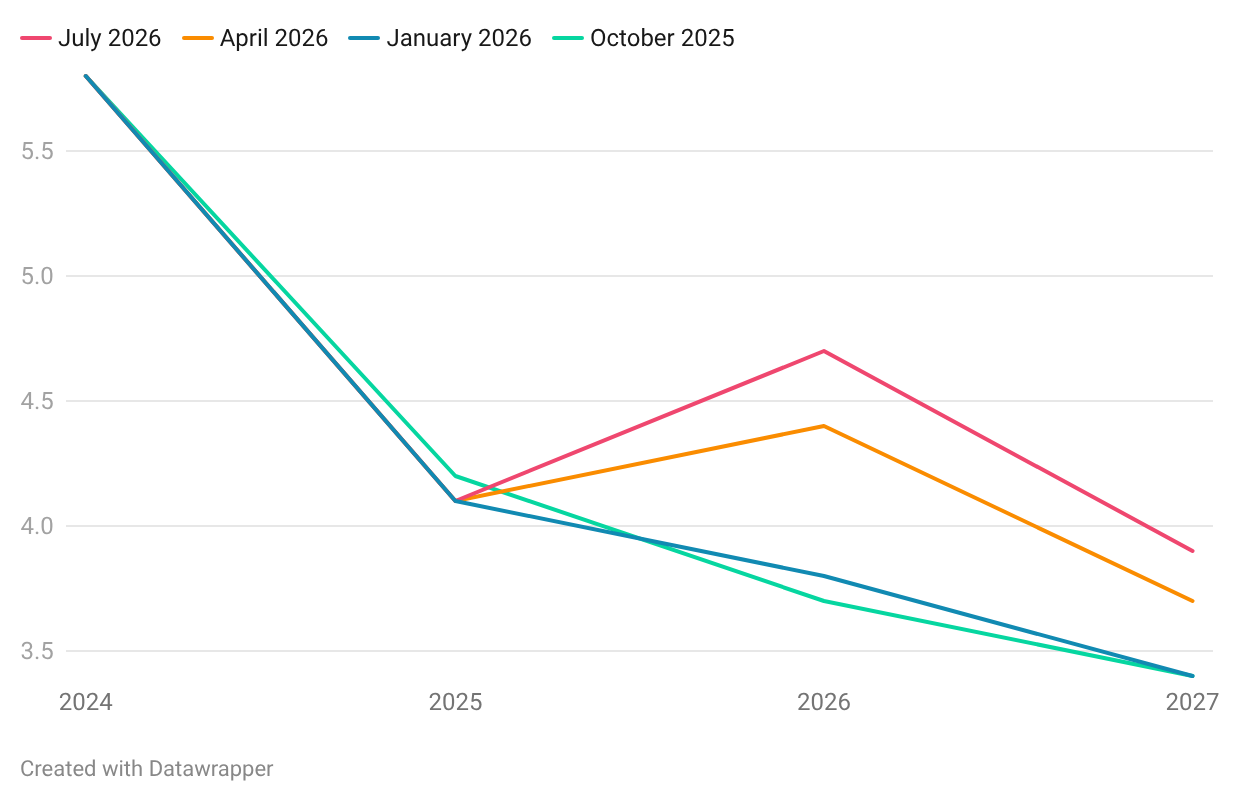

Inflation dynamics revised upwards

On the price front, the Fund expects inflationary pressures to accelerate. The global inflation rate is forecast to rise from 4.1% in 2025 to 4.7% in 2026, mainly due to higher energy and food prices. Global inflation is expected to fall below 4% only in 2027.

As shown in the chart below, the inflation projections published in July were revised slightly upwards compared with the April edition, indicating that the disinflationary trend underway since 2024 has currently come to a halt.

Global inflation in the latest WEO editions (%)

Source: StudiaBo elaborations on IMF data

An initial assessment

In drawing some initial conclusions about the impact of the shock caused by the US-Israel war with Iran on the global economy, the Fund highlighted a performance showing greater resilience than initially expected. The repercussions on the main transmission channels have been relatively limited, particularly regarding commodity prices, inflation expectations and financial conditions, which have remained relatively accommodative by historical standards.

The Fund also reported that quarter-on-quarter world GDP growth in the first quarter of 2026 was higher than expected in April. This appears to be partly attributable to the gradual increase in the share of renewable energy in global energy production, which is making many economies less energy-intensive than they were a few years ago and therefore more resilient to increases in energy prices.

Country focus

Let us now examine the macroeconomic forecasts for a number of individual countries.

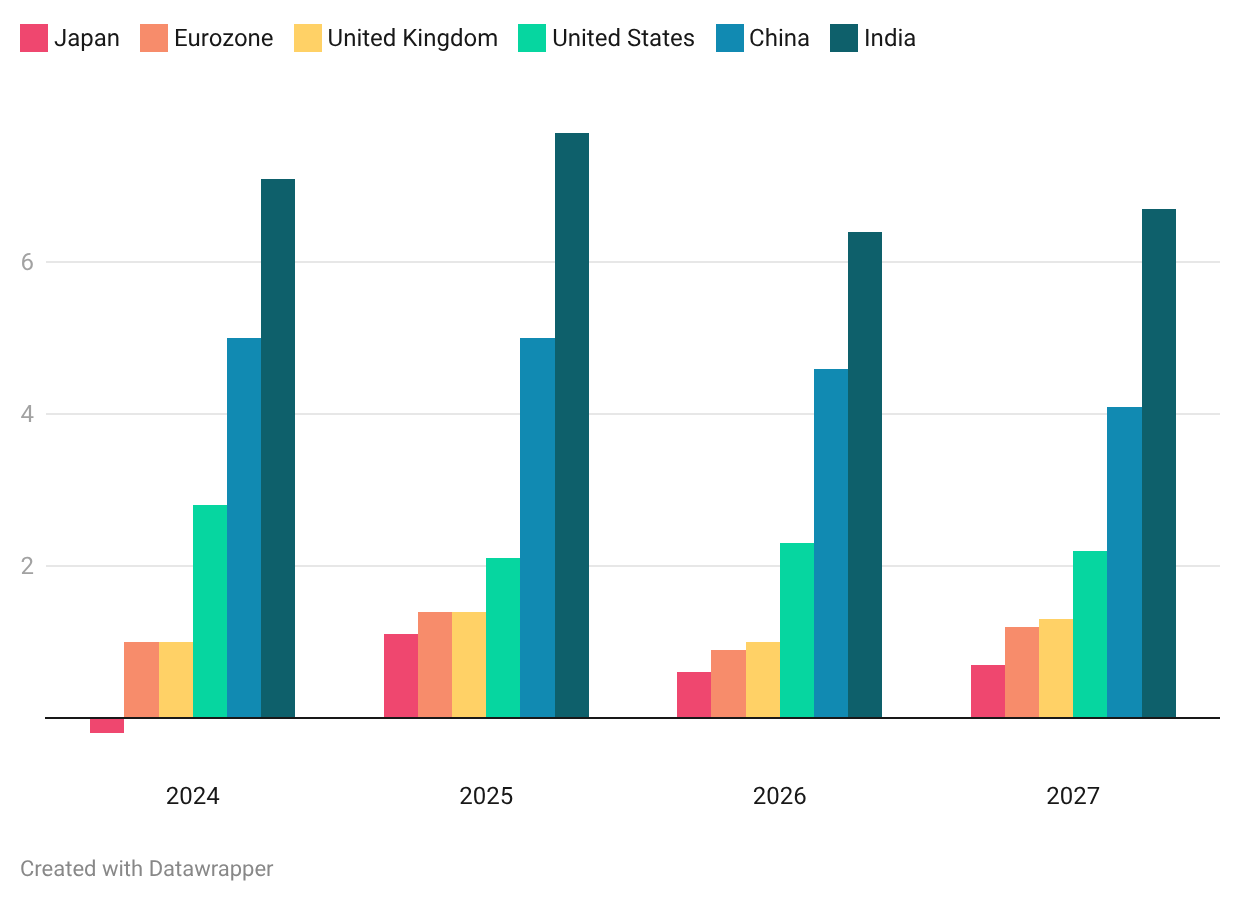

Starting with the United States, although US economic growth remains below the levels recorded in 2024 – the last year before the beginning of the trade war – the GDP forecasts published in July remained broadly unchanged compared with April: +2.3% in 2026, +2.2% in 2027.

US economic activity continues to be supported by fiscal policy, accommodative financial conditions and continued business investment in the technology sector. The ongoing war has had a limited impact, given the country’s status as a net energy exporter.

The economic outlook is significantly weaker for the euro area, which is expected to grow by 0.9% in 2026 and 1.2% in 2027. In this case, the 2026 GDP forecast was revised downwards by 0.2 percentage points compared with the April WEO, reflecting a significant negative carry-over effect from the first quarter. This was largely driven by Ireland, although it also points to weak momentum elsewhere. Growth is being restrained by higher energy prices and limited consumer confidence.

The outlook is also relatively subdued for the UK economy, where GDP growth is expected to stand at 1% in 2026, compared with 1.4% in 2025, before partially recovering to 1.3% in 2027 as the energy shock gradually eases.

GDP of the world’s largest economies: historical data and forecasts (%)

Source: StudiaBo elaborations on IMF data (World Economic Outlook Update, July 2026)

Among emerging economies, the case of China is particularly noteworthy. GDP growth for the Asian giant is expected to slow to 4.6% in 2026, compared with 5% in both 2024 and 2025, weighed down by higher oil prices, prolonged uncertainty and structural challenges.

By contrast, India continues to stand out for its dynamism and remains one of the world’s fastest-growing economies, supported by strong private consumption and activity in the services sector. Elsewhere in Asia, Malaysia, with a GDP growth of 4.7% in 2026, Thailand (+1.9%), Vietnam (+7.5%) and South Korea (+2.6%), are benefiting from the current strength of technology-related economic activity.

Conclusions

The complex international environment, currently affected primarily by the shock of the conflict, is confronting policymakers with difficult trade-offs. The balance lies between containing inflation, supporting economic activity and protecting households. At the same time, the strong momentum generated by Artificial Intelligence is supporting economic activity, while exposing the financial system to a greater risk of instability.

In this context, the task facing the authorities is not only to manage the immediate impact of current shocks, but also to strengthen resilience to future shocks. This requires country-specific policy responses, together with efforts to promote renewed international cooperation.

You may be interested in:

Export 2026-2029: ExportPlanning updates its forecast scenario

Published by Marzia Moccia. .

Conjuncture Export markets Uncertainty IMF Global economic trendsFor exporting companies, the ability to promptly interpret the evolution of international markets is now a key competitive factor. In a global context characterized by rapid changes and growing unce}... [ Read all ]

US Trade Deficit Put to the Test by Tariffs: Evidence from First-Half 2026 Data

Published by Marzia Moccia. .

Slowdown Conjuncture United States of America Uncertainty Trade war Foreign market analysisAmid uncertainty that has now become the new normal, international geopolitical tensions, and the reshaping of the rules governing global trade, the United States undoubtedly remains a key focus of }... [ Read all ]

Global Economic Outlook: International Trade Results for April 2026

Published by Marzia Moccia. .

Conjuncture Industries Uncertainty Global economic trendsThe data for April 2026 document the continuation of an expansionary phase in international trade, albeit with significant differences at the product level. [ Read all ]